First of all, I need to apologize for the absence of writing a blog article (and publishing a Sector Spotlight Video). In the intro of today's episode of Sector Spotlight, I explain a bit about what happened. But to make a long story very short, on Wednesday evening, 11/17, I found my wife at the back of our property, wholly drenched in blood and confused, not remembering anything about what happened. She was rushed to the ER and stayed in the hospital for six days. She is now back home and, given the circumstances, she is doing relatively well.

As a result, priorities shifted to taking care of my wife and managing chaos here at home. At the moment, everything seems to have settled and is under control, so I can get back to work.

Looking at the market and sector rotation following last week's dent as a result of new COVID fears, I think the overall condition of the market is still pretty good.

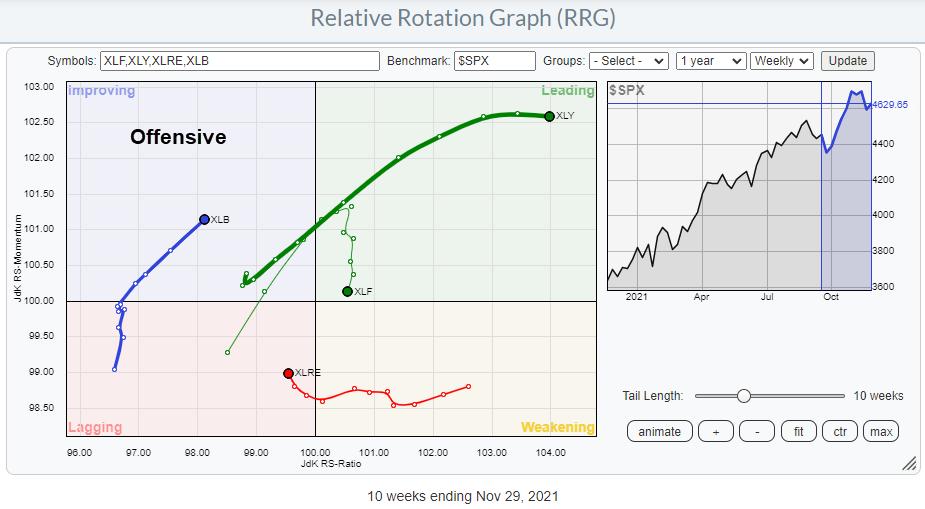

Offensive

The rotation for the offensive sectors is still overall pointing to strength for this segment of the market. Consumer Discretionary is obviously the strongest sector inside the leading quadrant on a very long (=strong) tail. The flattening/stabilization of the JdK RS-Momentum is nothing to worry about yet and to be expected after such a strong rotation.

Financials started losing relative momentum after entering the leading quadrant. However, the sector remains pretty stable on the JdK RS-Ratio axis, which means the relative uptrend is still intact. Materials are inside improving and have started to rapidly accelerate towards leading over the last few weeks, making it an interesting sector to keep an eye on going forward.

In this group of offensive sectors, the only sector inside the lagging quadrant on the Relative Rotation Graph is Real Estate. This rotation from weakening into lagging is happening after a long cycle through leading. The recent pick-up on the RS-Momentum scale suggests that improvement is underway for this sector.

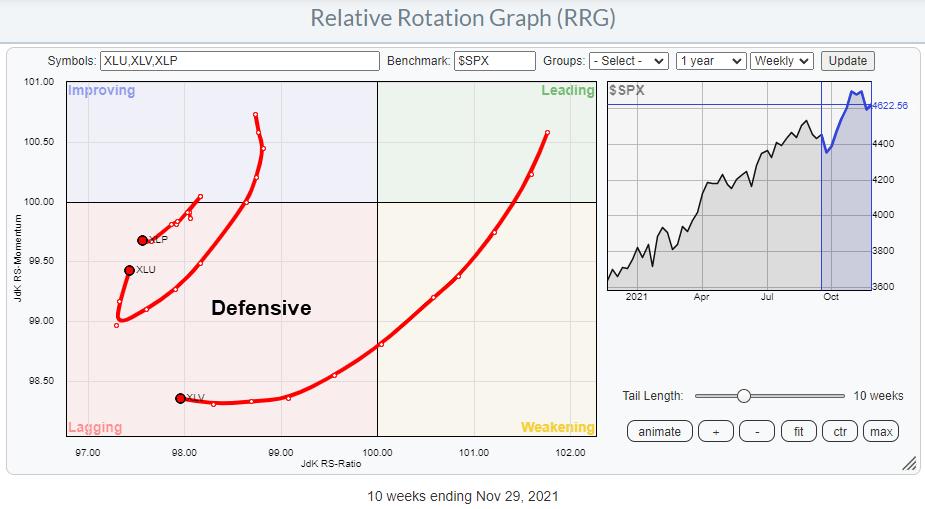

Defensive

IMHO, the group of defensive sectors is still sending the strongest signal. This group of sectors is expected to do well, outperforming SPY in times of general market weakness. This is not the case at the moment. All three sectors, Consumer Staples, Utilities and Healthcare, are well inside the lagging quadrant and pushing further into it. Only Utilities has picked up some relative momentum over the past few weeks, but it is still the lowest-ranked sector based on JdK RS-Ratio.

The entire group of defensive sectors in a relative downtrend against the S&P 500 is not a rotational characteristic of a bear market... On the contrary...

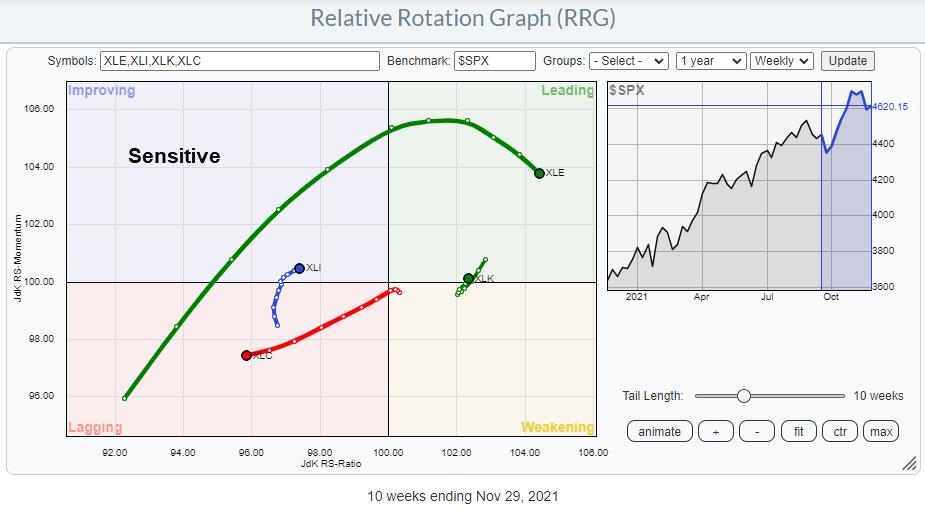

Sensitive

The group of sensitive sectors can help with providing additional confirmation on the direction of the general market and help tip the scale in either direction.

On this RRG, we see the Energy sector well inside the lagging quadrant, but rolling over for three weeks. Nevertheless, the relative uptrend is clearly intact. The Technology sector has just returned into the leading quadrant after a rotation through weakening and seems to be starting a new leg in its already existing uptrend.

The Industrials sector has moved out of lagging into improving. At the moment, its tail is at a positive RRG-Heading, but the tail length (short) indicates that there is not much power behind the move yet. So, for the time being, the rotation is positive. The only sector inside and heading further into the lagging quadrant is Communication services.

Three out of these four sectors are on a positive rotation, which tips the scale for the market (S&P 500) to positive.

S&P 500

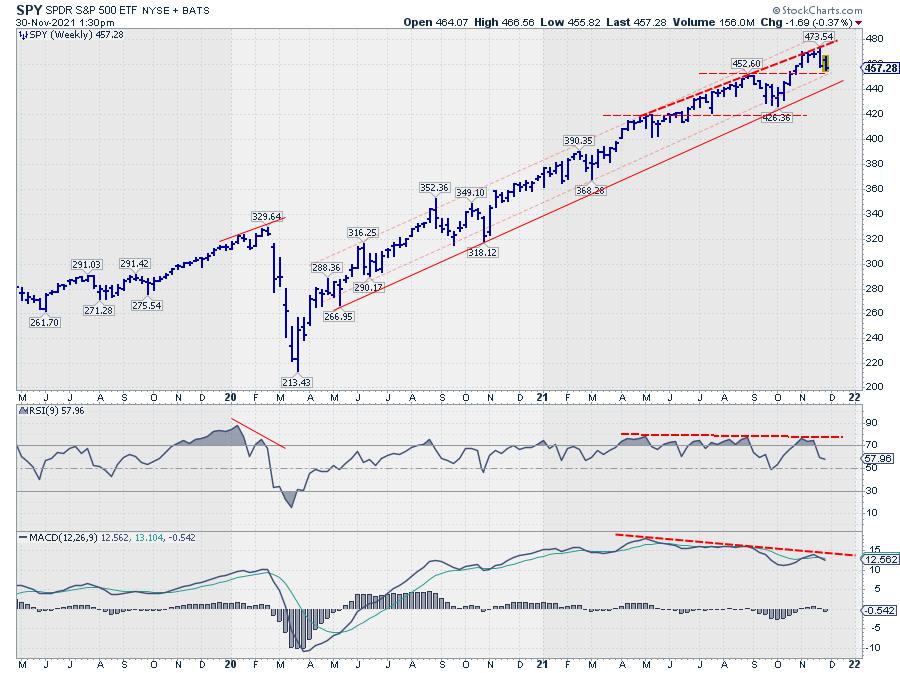

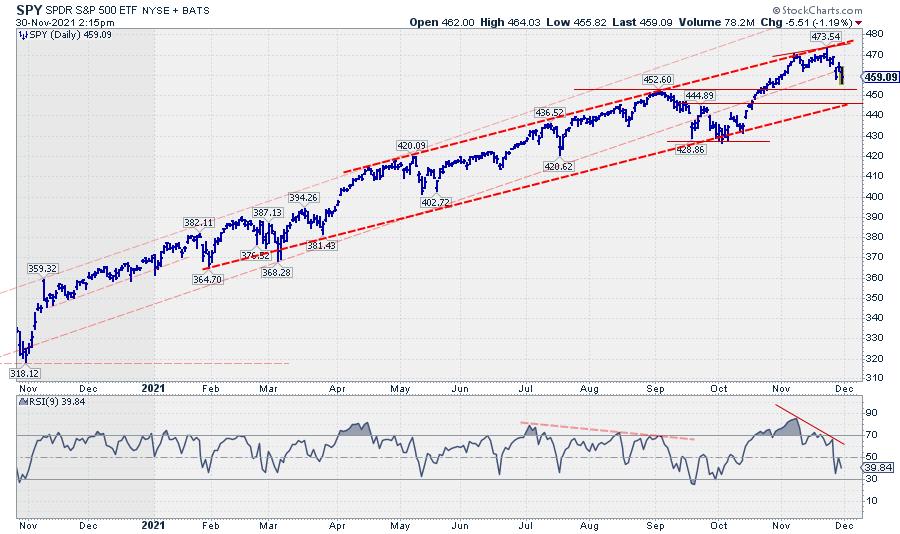

The only concern I have for the near term is that a negative divergence between RSI, MACD and price has built up again. We have seen this situation before the September drop towards the lower end of the channel, and it has now developed again.

On the weekly chart, the peaks in the RSI are all on the same level or slightly lower, while the price has peaked at higher levels during that same period. However, in the MACD, the divergence is more substantial, with lower highs vs. higher highs in price.

On the daily chart, the divergence between price and RSI is clearly visible.

Divergences are often a prelude to a pause in or a reversal of an existing trend. Given the observation that long-term uptrends for all sectors and the S&P 500 are still intact, as well as the observation that the rising trend channel on both the weekly and the daily S&P chart is still intact, I am judging this divergence as a warning signal for a possible renewed pause, leading to a sideways move inside the channel or a shorter decline towards the bottom of the channel.

The support levels are indicated on the charts above; they are coming in roughly between 445 - 452.5. As long as SPY can hold above these levels, preferably within the boundaries of the rising channel, the trend remains intact.

Julius de Kempenaer

Senior Technical Analyst, StockCharts.com

Creator, Relative Rotation Graphs

Founder, RRG Research

Host of: Sector Spotlight

Please find my handles for social media channels under the Bio below.

Feedback, comments or questions are welcome at Juliusdk@stockcharts.com. I cannot promise to respond to each and every message, but I will certainly read them and, where reasonably possible, use the feedback and comments or answer questions.

To discuss RRG with me on S.C.A.N., tag me using the handle Julius_RRG.

RRG, Relative Rotation Graphs, JdK RS-Ratio, and JdK RS-Momentum are registered trademarks of RRG Research.