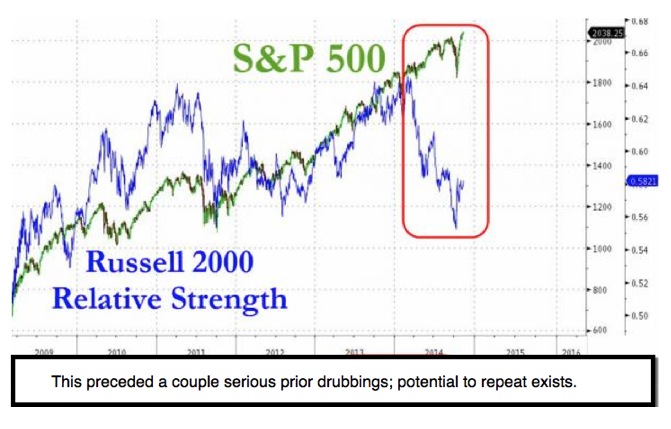

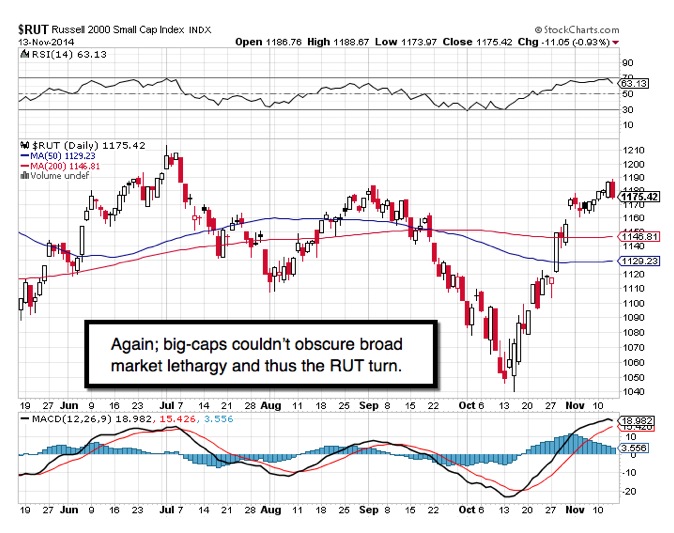

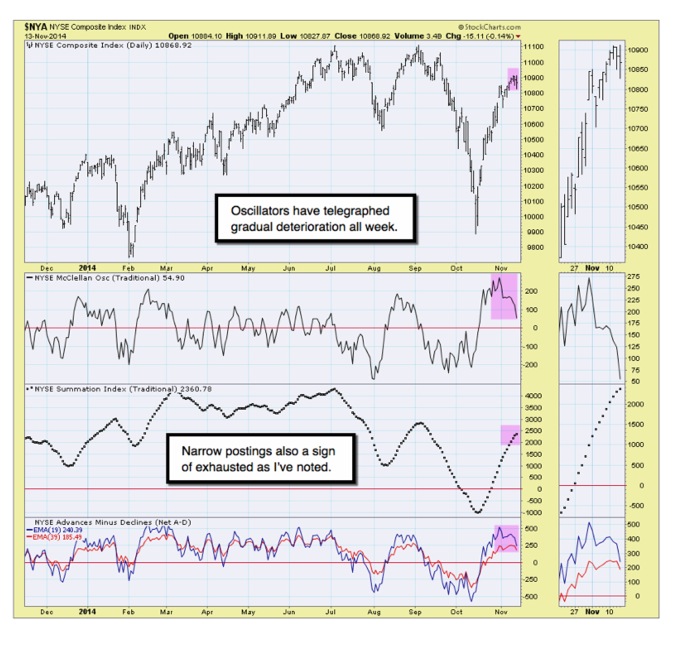

Current analytical 'narratives' - are mostly bereft of realistic perspectives. For their parts, Bulls (lacking a growth story or a truly-friendly Fed); point to a 'megaphone' technical pattern as their continuation logic (perhaps it says look out; as money managers seem bereft of justification for upside extensions).

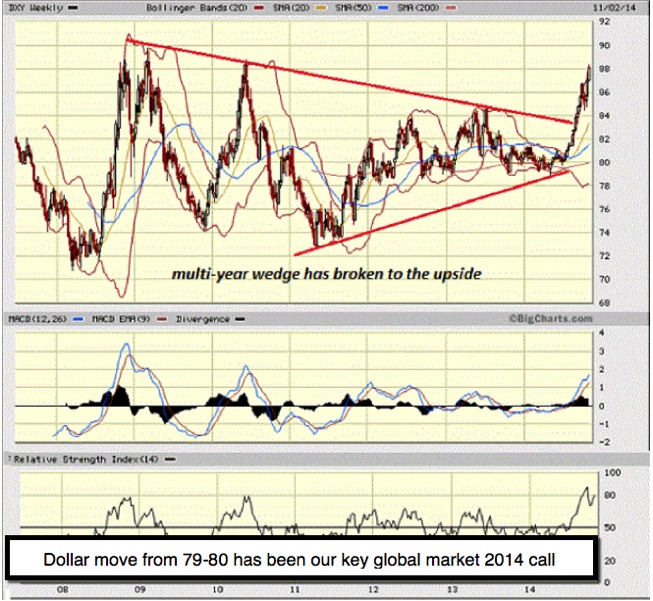

Conversely, bears argue risks of 'currency wars'; with the most radical bears (not merely gold bugs) blaming the U.S. for chaotic FX markets. Actually the U.S. is the more stable; our projected US Dollar advance (off 79 over recent months, along with a Euro decline anticipated from near 1.40) enhanced the ability of some countries (including Germany & Japan) to slightly grow exports to America because of currency advantages (thus slowing their decline).

The irony is that Bulls focus heavily on big-cap leadership; debate whether or not 'Net Neutrality' is a plus, a minus, or (as Mark Cuban put it) Ayn Rand in the modern era. This debate is a symptom of a struggle between 'populism' vs. innovative capitalism; (complexity analyzed and simplified for members).

But again; this is not the prime issue of the moment: global disintermediation of a sense is. Those blaming the Dollar are miss the main (detailed) threats.

Ramifications of a new Cold War, launched by Russia regardless if they had at a point some valid objections, (discussed). He wants to be Vladimir the Great.

Bottom-line: geopolitical issues are underplayed in market analysis chatter; so I mention it, including the 'melding' agreement reached between al Qaeda and ISIS today, which significantly increases the danger (further details noted).

Currency wars are a danger; and while colluding 'central banks' (discussed and not as it once was). Brisbane may affirm better unity; but Beijing and this weekend's Gold vote in Switzerland (are factors we've reflected upon).

Daily action - long-term economic warfare, is difficult to interpret as far as risk for markets. Obviously, the extent to which European countries and our own d 'gear-up' beyond the obvious 'cyber-warfare' concerns; are great (sure, certain companies will profit, others less; and nuances of Gov'ment work are always hard to depend on). What is notable is something else little reported: ponder if it really means much that Russia took advantage of soft Gold pricing recently.

I realize this seems like a premature discussion; but it might not be. When one has to deal with 'geopolitical ramifications', not just theoretical risks; one best be prepared to understand what's at-stake before anything is reported in the news. In this case, early causalities are (detailed in the full text for members).

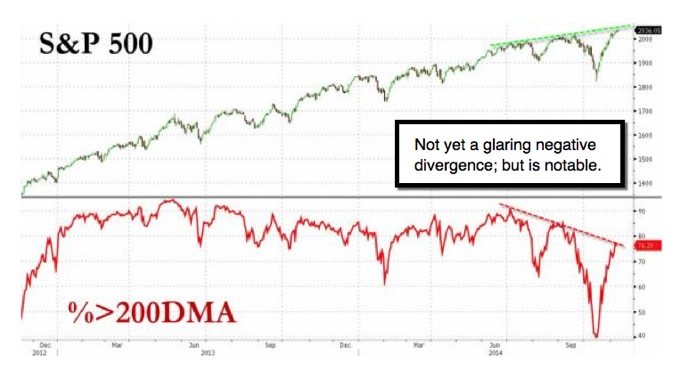

For now: we suggest either 'partial' profit-taking or overnight short-sale (some skin in the game) based on an E-mini/Dec. S&P 2042 short-sale guideline.

Prior highlights follow:

Bottom-line: (discusses whether downside risks are mispriced).

Lots of hard challenges progressively resolving in markets; but progress is a fleeting goal in global economics and geopolitics. Increasing awareness and sobriety has belatedly dawned on analysts. Investors grasped unsustainable financially-engineered moves; taking equity markets (to levels we identified).

Enjoy the evening;

Gene

Gene Inger

www.ingerletter.com