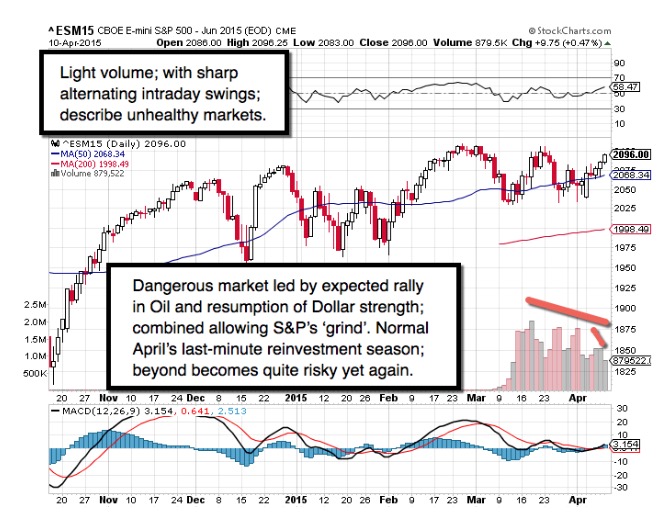

Beware the 'Ides of April' - might be pertinent for investors; as tax-time has not been a March, but April filing deadline for years (other than corporate). At the same time, seasonal reinvestment contributions should be waning, just about now; another factor contributing to exhausting 'fuel' for upside grinds.

In this case little has happened that could be market-moving; other than new threats between the Saudi's and the Iranians, as well as chatter about China's trying to upset the financial structure (not that it doesn't need reform; but that is presumed a long-term consideration). Big earnings parade starts this week.

We suspect the new week (especially with Yemen tension) will see Oil strong yet again; and the Euro soft, accompanied by Dollar stability or strength, as expected to resume, and did over the week just past. That the market resists this impediment to an advance is ignored; they won't ignore it once the S&P reverses again, and probably cite strong Oil & Dollar action as 'causation'.

Daily action - will become exciting anew; whereas last week's swings were incredible; if often tough for bull or bear alike to catch. This week should try the upside briefly; then risks being on the defensive (for outlined reasons).

(Most technical and Oscillator portions reserved for regular members.)

Prior highlights follow:

The financial world remains crazied - which in itself doesn't trigger decline; in fact it causes traders to be cognizant of risks; thus beside running shorts for sure (on the frequent shakeouts); you have the use of leverage and 'spin' to defend the illogical arguments as to why stocks should continue advancing.

This was a 'Dudley' market day; in which Bank of America came out with the comment that NY Fed President Dudley pretty much said this was controlled by the Federal Reserve. (Balance of Fed discussion just for regular readers.)

Bottom-line: evolving as outlined; S&P hangs on; bond markets as well as corporates become precarious.

The danger in 'hollow' low liquidity / low volume rallies is that when they break the downside tends to be amplified. (What we're expecting and when noted.)

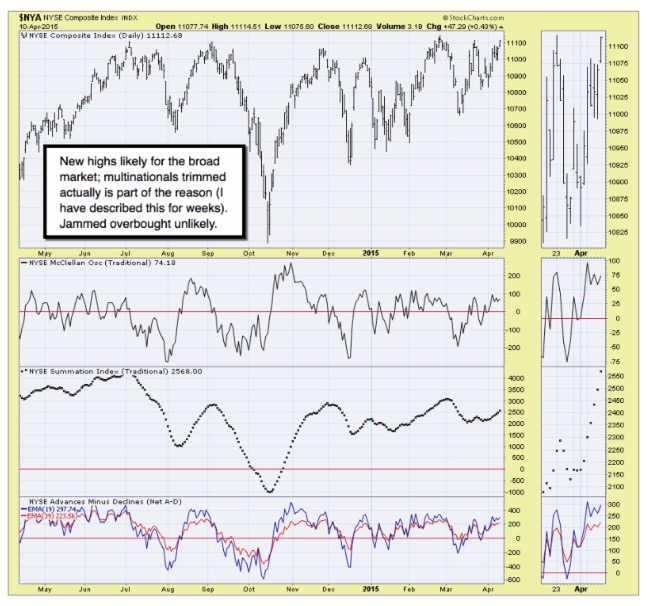

For investors, there is no change; distribution on rallies; faltering momentum; each rally has less 'punch'; and there is too much monetary policy emphasis, as even if the Fed 'never' hiked rates, the absence of QE and gradual taper, alone remove some props from under the market (ongoing for months now).

Just remember: the longer the distribution, the harder the potential fall.

Is a market correction probable - or are we heading toward a disaster? (It's a topic, like much of the last two weeks, that must be reserved for members.)

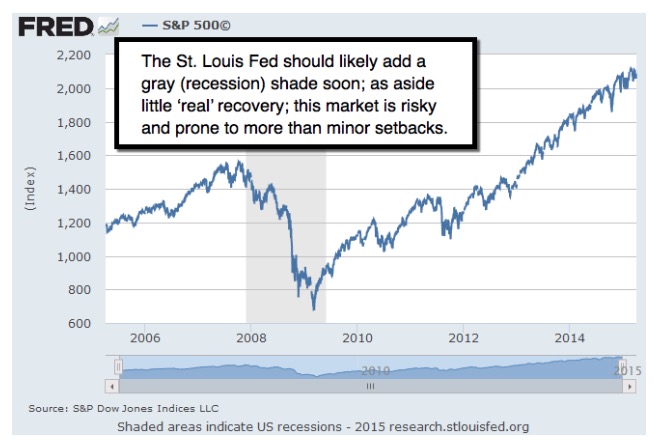

When you look at the long-term S&P, you see what actually is likely history's best-managed and 'controlled' (we won't say manipulated) market advance. It is normal that straight lines exist on road-maps, but not when actually driving.

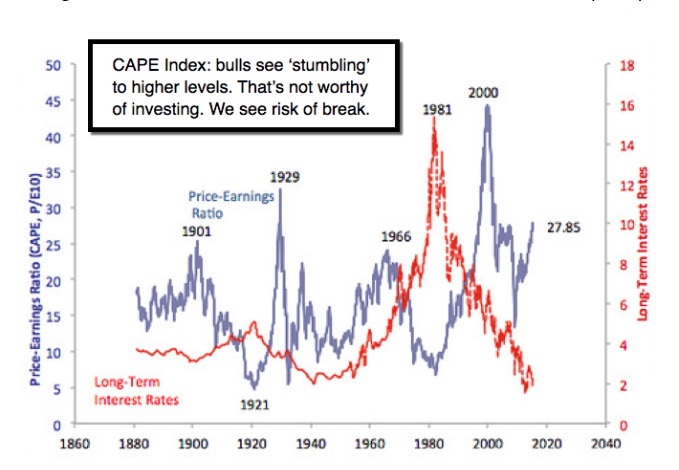

('Relational' multple P/E conditions and assessment provided.)

The 'ghost of 1937' comes to mind - as we look at economic data (more).

Saudi Arabia rejected Russia's amendments to a UN Security Council draft resolution which would see an all-inclusive arms embargo on all parties in the Yemeni conflict. (Discussion of this and other global issues.)

Bottom-line: stock markets recovered 'some' borrowed time; hence there is still a good bit of 'trading' cushion about the March lows. (However again we are at vulnerable levels, after an upside 'grind'. The 'cushion' simply means it will be a 'process' to challenge and then take-out March lows, and so on.)

Treacherous times. The process evolves.

Enjoy your evening;

Gene

Gene Inger

www.ingerletter.com