Repercussions (or lack) - regarding Greece were said responsible for the market's out-of-the-box run (following Europe and futures) early Wednesday. Interestingly, this became a flip-of-the-rumor (coin) bet during the session; as Germany came forth and said they were unaware of any improved prospects for a 'deal'.

The story rolled through several hours; which does suggest credit and equity markets 'do' care about what happens with Greece (mostly due to peripheral risk in other countries perhaps); contrary to the spin that's it's not important at this point. What can be said is the longer a 'deal' isn't cut as deadlines near; it could be considered odds favor failure. But back-channel deals are just that; of course not leaked to the press if possible before negotiations conclude. (It's also not the primary or sole market concern, as we've outlined.)

So trading based on Greece is a 'roulette' game (as it keeps spinning daily; sometimes landing on red or black repeatedly during a day); while increasing focus (remainder, please understand, reserved for our subscribing members).

The U.S. today said it is 'not' contemplating extending Iran talks beyond June if a deal isn't made; China is hinting at further margin restrictions; a story about hydrogen risk at Fukushima is not confirmed; and techs got hyped a bit more due to the ReCode 'con', gathered in California; and Broadcom.

Ironically, it was the youthful CEO of SnapChat, who spurned FaceBook's 3 billion offer (even when Mohammed came to the Mountain essentially); who appeared and while indicating they'll eventually do an IPO; looked brilliant by comparison to reporters looking puzzled when he said 'everybody knows' the market is heading toward a correction; and that money-printing is the culprit. (If 'everyone knows', why are they exposed to the max? Ahh.. we know why.)

Well of course we applaud that, and it simply makes the case. It's especially interesting in that so many pundits spend hours rationalizing upside; ignoring the fails (not just Michael Kors); and pretending the Fed's policy's unchanged even when the Fed begs markets to listen; so as to dampen downside risk.

In sum- for the moment the market isn't listening; as the usual rhetoric went from the litany of real issues we've warned of (after the fact as Tuesday's hit rattled them), to the pundits chortling how you had to 'buy the dip' and so on; 'as if' there's nothing wrong at all. (They just go with emotion; or 'promotion'.)

To us this is more than 'pockets of excess valuation'; and 'pockets of stocks undervalued' (most of those are down for reasons); this is a broad advance so long in the tooth that it becomes somewhat fractured; so (reserved).

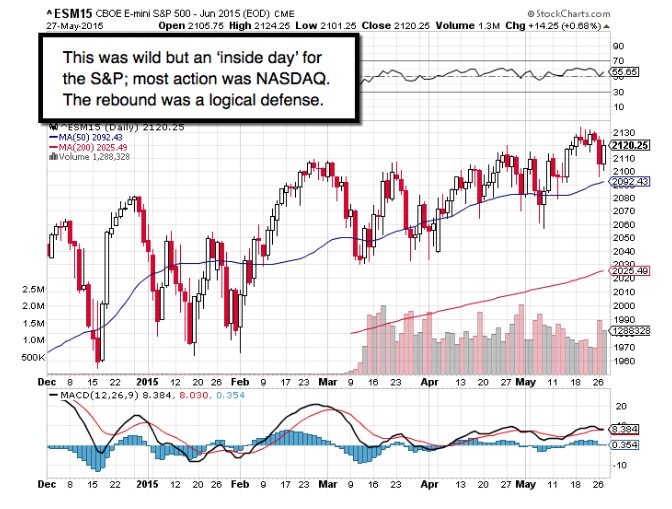

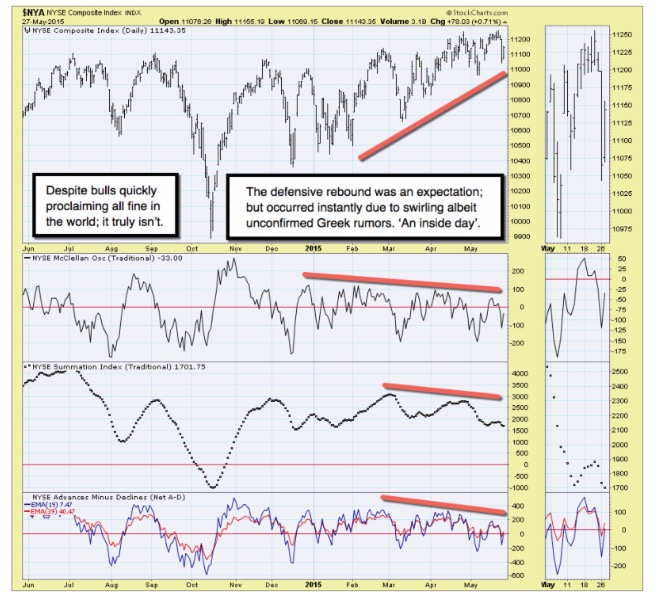

The kind of alternating volatility is a sign of weakness not strength. Dangers lurk in many ways; all of which (including Greece, China, Japan, Europe and the Middle East) are capable individually or collectively of being cited more or less as 'causal factors', along with the changing Fed policy, for the decline. If anyone says what decline; look at the market internals, the inside day hyped by the Grecian formula rumors; and the structure really isn't changed. They'll freak if (as I suspect) this runs into a brick-wall of resistance early Thursday.

Daily action - we knew they'd try the upside on Wednesday; but this insanity (manipulated) Greek deal rumors (Berlin came forth to say they heard nothing about it, which was interesting since media hardly took a moment to note that there was nothing behind the rebound but more circulating rumors).

(And of course as the videos outlined, we know the technical perspective was requiring them to mount a comeback after Tuesday; but also suspected that it would falter Thursday, in which incidentally we bought the first hour right near the trading low; took a near 'home-run upside' 'gain -yes- long); intending the next trade a move back to the 'short' side of this key technical session.)

Sure that was enough to run-in the shorts and shoot this market back up; still as an 'inside day', which itself is typical after a decline like Tuesday's; albeit not so crazy. Technically it's more than a rebound to the breakdown point; but not a lot, and is right back up to the top of the more or less 2080-2120 S&P range. Bulls will expect follow-through and be stunned when they don't get it.

Yes, a number of folks see this as proof the dips have to be bought; and we'll say it's a logical rebound that has to be sold into. If and as yesterday's lows come-out in future sessions; that will be (most of the rest of the report and all videos reserving for subscribing members; we work diligently at this, and will appreciate your joining; especially during crucial market times like this).

Prior highlights follow:

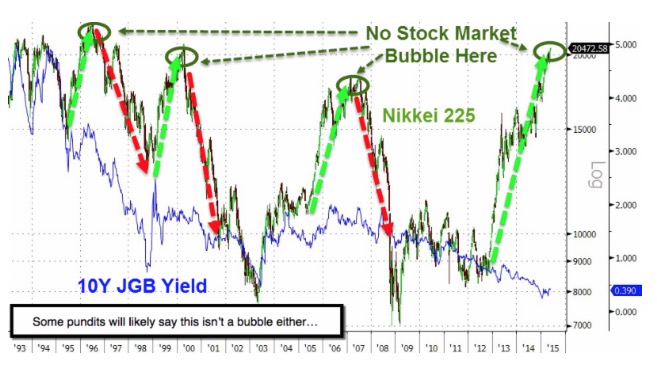

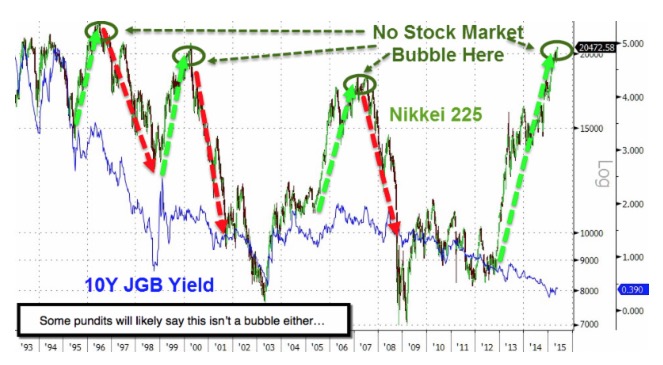

In a grand excessive market pricing cycle- the final refuge of speculation is not necessarily waiting for the cherished 'retail speculation' to commence, but be the 'new era' abandonment of historically reliable measures pretty much in a wholesale dismissal way; resting faith instead on the advent of central bank control so advanced (they think) that a 'money printing' era in which the old rules simply don't apply; and all that matters is 'cash flow'. (More redacted.)

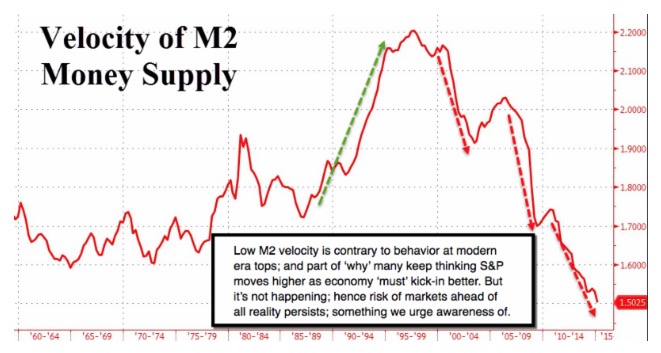

Reduced 'capital formation' - is about the last thing the Federal Reserve of course expected after their repeated rounds of stimulus; but is what they got. They often dismiss policy criticism based on 'it would have been worse if we'd not done the emergency stimulus', and we agree; but dispute benefits of any continuation beyond that point. A simple gander at the M2 'Velocity' of money proves the lack of dynamism after all their effort.

There is a seriously dangerous aspect to this; because aside the Fed painted into a corner given firming rates (recently easing a tad); (details redacted).

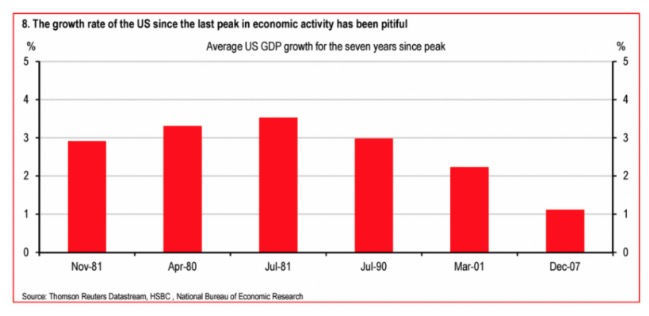

My point is Washington has been borrowing from Peter to pay Paul as we all at this point know. And they won't get out of it by more stimulus. That means, if we're right, that growing our way to levels justifying current S&P multiples is a tall task; and one that leaves that 'open jaw' between (balance redacted).

That lack of M2 'velocity' suggests (reserved for members). Factors holding S&P up are esoteric; (detailed; as well as why and how they'll falter).

Bottom-line: despite the S&P achieving new highs again; the internal top's been behind for weeks; not a new technical development. Rallies (blow-off at this point?) appear to be efforts to forestall technical breakdown (more).

Treacherous times. The process evolves.

Enjoy the day, and join us at this potentially pivotal time;

Gene

Gene Inger

www.ingerletter.com