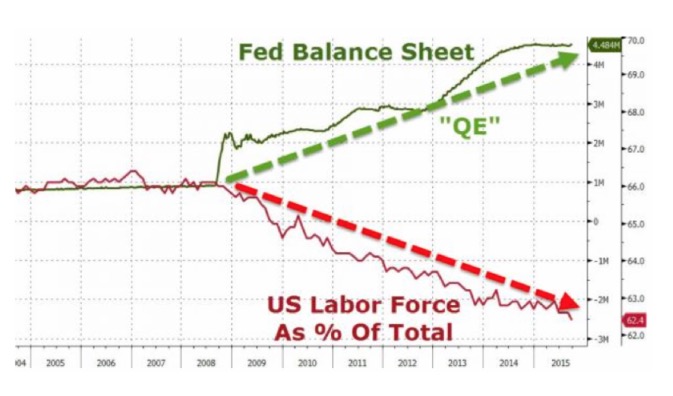

The transition driving markets - continues reflecting schools of thought that reflect competing analytical views of 'what drives the stamina'. One obviously is the idea of dependency on central banks; which has been waning, but hope remains alive in that segment, as they desire soft economics to keep stimulus alive and dismiss concerns about the bloated central bank balance sheets (in our view a dangerous approach that even the Fed belatedly acknowledges).

(Our clear daily trading view as of mid-day Friday is short Dec. S&P at 2011.)

Another is liquidity, which I've contended really is a major factor, in-part clearly strained (not just because of seasonality); and is responsible for rapid shifts of direction in markets, often repeatedly in a single day. That's the basis for fairly wild volatility, with the dynamics pulling bear and bull into alternating swings.

Liquidity drives market valuations in other markets too. Banks have tended to respond to fixed-income assets trading at very low-to-zero returns for a quite long period of time; thus contributing to eventual boom-and-bust outcomes. It's a sketchy time when such low rates allow overheating of markets (not just the stock market; consider housing as well). As central banks provide this liquidity and then banks intermediate this liquidity to areas believed to need it. Now, if people want to unwind positions; it's hard to get past the vanishing liquidity (for unwinding); and that's a very difficult position which hedgers have discovered.

That might have been one of the lessons of both the expected August/Sept. hit but also the Fed's tendency to withdraw into its shell and becoming muted and a bit petrified about taking moves. The US is 'in theory' (rest is for members).

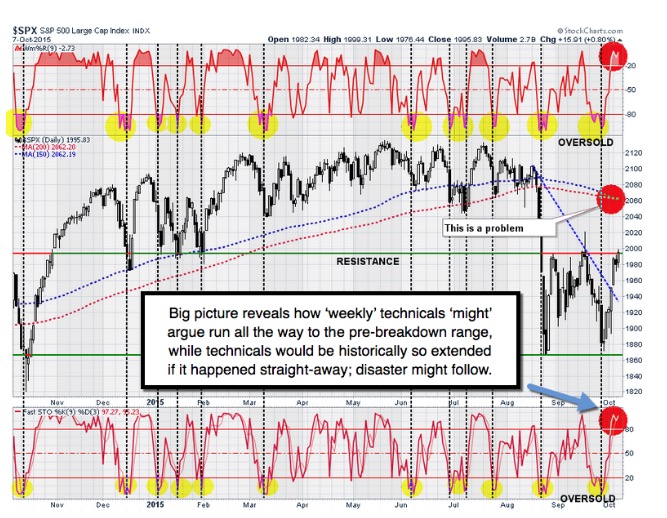

Bottom-line: this market remains the 'most' overbought it has been on a daily basis (stochastic work; not others) since just before the August breakdown; but that came after several weeks of 'erosion' that sapped market prior to the 'flash crash'. On a weekly basis (rest for regular ingerletter.com subscribers only).

Incidentally this weekend, we'll offer you the chance to 'discover' our analysis on a nightly basis, with a Columbus Day 'special'. Available to new members only; we'll rebate $26 on Daily Briefing subscription, and $50 on MarketCast subscriptions. This offer will expire at the close of business Monday. We'll be on-guard for trading and investing moves as this crucial October evolves.

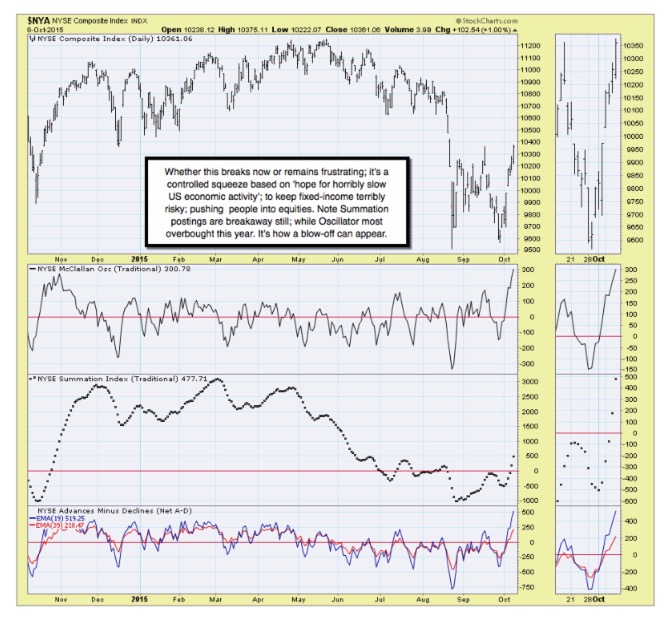

Aside that, they desperately want to survive October, in hopes of being past at least the majority of 'fiscal year-ends' for most funds, and closer to a traditional seasonal reinvestment (retirement funds) period. The problem (more); missed lowered bars for earnings and revenue (no longer masked by buybacks). This week, Bears would rather head 'to' other bars; but I caution enthusiasm can wane quickly in a kind of a blow-off squeeze in such low liquidity times.

Daily action - was pretty wild; somewhat complicated by political news as well as economic data (generally negative) from Japan, China, and Europe. Then a out-of-the-blue withdrawal by Congressman McCarthy for House Speaker, hit the market a bit; (rest just for our subscribing members; please join us).

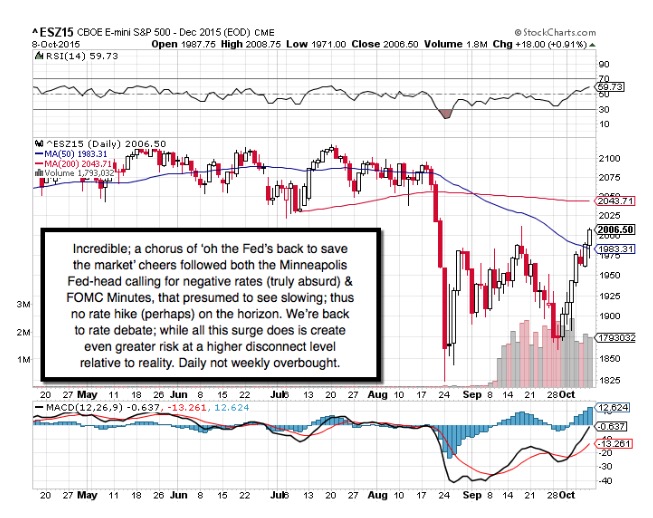

Amid all this the Minnesota Fed-head came forth to call for 'negative rates' and more stimulus (insanity to press financial engineering's pedal to the metal); so what does the stock market do? (Redacted as to reaction and what's coming.)

This chaos, on-top of which you had the sad news of an American Hero; USAF Airman Spencer Stone as the victim of a serious stabbing last night near or in a Sacramento bar. Maybe it's just a bar fight; but one doesn't know until one knows; hence one might ask for no leap to judgement; including not denying the enemy wants to go after our good guys. Meanwhile we'll say a prayer for Airman Stone's full and complete recovery.

(We noted) targeting S&P 2000 has been the Bulls' objective; stretching it to that level Thursday (more details). (Editor: as of mid-morning Friday, our daily trading guidelines moved to the short-side of Dec. S&P at 2011, just for now.)

'To be or not to be' - a 'virtuous' cycle, as contrasted to an overly aggressive rebound, is the question. Whether or not thou shall see a vicious cycle appear shortly, is a subjective question that even Shakespeare could only speculate a bit on, at this point.

We're overbought on a daily basis; though not particularly on a weekly basis. It is a reason why there's such ongoing debate as to whether this continues. For a trader that might be moot; as catching moves is the goal, and the next phase should be exhaustion (ideally near-at-hand) of a short-term upside scramble.

The Middle East saw Russia putting those Forces to work as suspected; while the U.S. is looking fairly impotent, and this Administration refuses to endorse the Russian action; falling-back on the argument about attacking anti-Assad elements. Without opining on that as such; we'll question 'why' Washington's lack of singling-out the strikes on ISIS as very laudable and of mutual interest.

Bottom-line: the Middle East is trying to emerge from a vicious cycle with one of the few ways it ever has; brute force by an outside power. We don't endorse that per se; but given the threats to the world, and many lives lost to extreme Islam, we would think most normal people (Muslims included) would link-up to a campaign to rid the world of ISIS, and somehow politically replace Assad but not destroy the basic governing entity that runs daily life in it (or any) country.

The stock market is near the end of what can be a rebound within a rotational vicious cycle, that followed a prolonged virtuous cycle levitated by stimulus or central bank financial engineering. Unwinding (rest for subscribers).

The 'Party Gods' on Wall Street - remain convinced that nothing matters but easy money, low rates, and a Fed totally cowering in a corner, frozen into sort of fear of inaction, and fear of acting; hence the beat can go onward & upward.

Not so quick: even today's action in a couple companies experiencing potholes on earnings (some of which should not be surprising) should serve to remind a chorus of 'new market order' Bulls of something shocking: earnings matter.

With limited news from Beijing or Shanghai during Golden Week, it was a good spot for Bulls to try to jam this market, and they did. But we suspect it swoons before week's end (trading tactics detailed).

Besides that tinderbox, we suspect Russia (and even Iran) are pressing OPEC members to isolate Saudi Arabia and the Gulf states, in a way that allows a bit firmer 'floor' on oil prices; such as I suggested in the mid-40's. I've expressed suspicions on Russia's motives related to stabilizing oil prices; and surprised nobody has gleaned onto this sooner as one of Putin's key goals. It remains far more important to Russia than to the US to have oil prices higher; a factor.

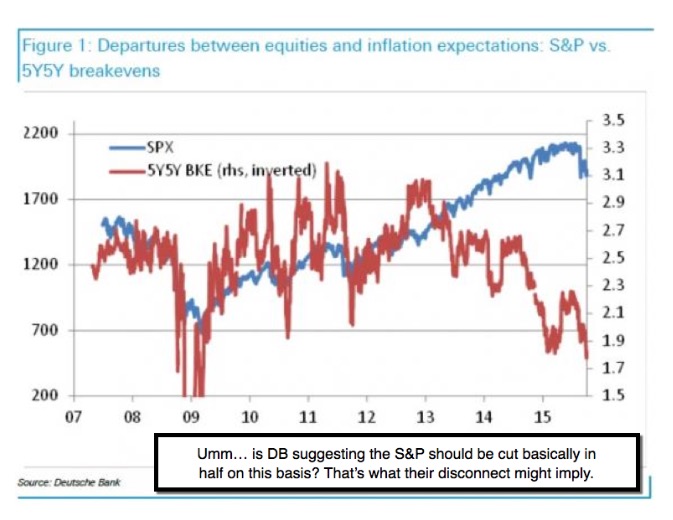

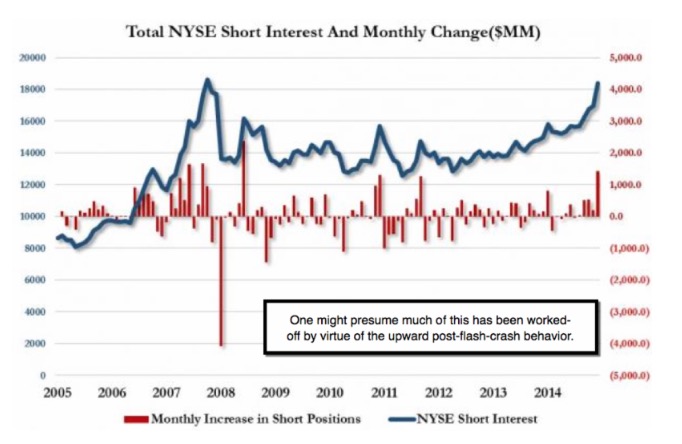

In sum: everything continues as outlined. Record high short-interest helped contribute to the rocket-ride upward with the down-up reversal. (Is) that now largely eradicated (we opine). Stay tuned.

Treacherous times. The process evolves. Likely akin to 'surfing' as it nears what's sometimes called 'point break'. (In this case the rebound rolling over.)

Enjoy the evening;

Gene

Gene Inger

www.ingerletter.com