Backfiring bearish bets - by rigidly negative money mangers (way different than a trader who uses a portion of assets in hit-and-run trading, realizing risks inherent in retaining broad short positions), are starting to become evident. Is it capitulation in its purest form? While we normally don't talk of individual managers, when they're larger than life and everybody knows who they are, or they tried to influence others because of their agenda, then besides fair game; it merits noticing any change in their stance, or in this case 'personnel'.

So, whether or not the departure of the CIO (Chief Investment Officer) of the personal George Soros 'family fund' (said to be about 25 Billion) is indicative of the view we've had (of too many big money managers too rigidly negative with incredibly heavy short large portfolios) is hard to say; but we suspect they're obviously feeling the heat now. (That's the biggest industry story many perhaps didn't even hear of this past week.)

Aside a few economic indicators (mostly reflected in charts we've share); (redacted). NASDAQ managed consecutive higher weekly closes; reflecting we suspect, a shift back into Oil a bit, as well as shuffles from multinational stocks that of course would suffer if the U.S. gets 'backbone' with respect to Trade policy (topic explored a bit).

Aside a few economic indicators (mostly reflected in charts we've share); (redacted). NASDAQ managed consecutive higher weekly closes; reflecting we suspect, a shift back into Oil a bit, as well as shuffles from multinational stocks that of course would suffer if the U.S. gets 'backbone' with respect to Trade policy (topic explored a bit).

Plus you have interesting geopolitical times. Russia is again beating-the-drums for a stand-off with Ukraine; moving missiles into Crimea, and cozying-up to Erdogan from Turkey, as the NATO relationship is more frayed than at any recent time. Two scores from the US Air Force (and Navy) this past week: one the announced elimination of a truly barbaric guy who ran ISIS in Afghanistan and Pakistan; and the other the strikes on ISIS in Eastern Libya, where the enclave they were ensconced in, was captured at last by Government (Tripoli-led) forces, supported by the U.S. We'll see how well this eliminates the threat in Libya, as I've said all Summer that ISIS on the Mediterranean is just not tolerable; both given proximity to Europe and radical groups within Africa.

What money managers that are 'not' short are doing, is now a form of 'musical chairs' associated with an effort to gradually shift exposure (details explored to members).

On top of everything (including the credit bubble); you have a property bubble that's of course most evident in cities like San Francisco (and surrounding environs), plus of course New York (which is in slight decline, and nobody wants to talk about that). I have pointed-out this risk for months, because (balance of topic follows to members).

On top of everything (including the credit bubble); you have a property bubble that's of course most evident in cities like San Francisco (and surrounding environs), plus of course New York (which is in slight decline, and nobody wants to talk about that). I have pointed-out this risk for months, because (balance of topic follows to members).

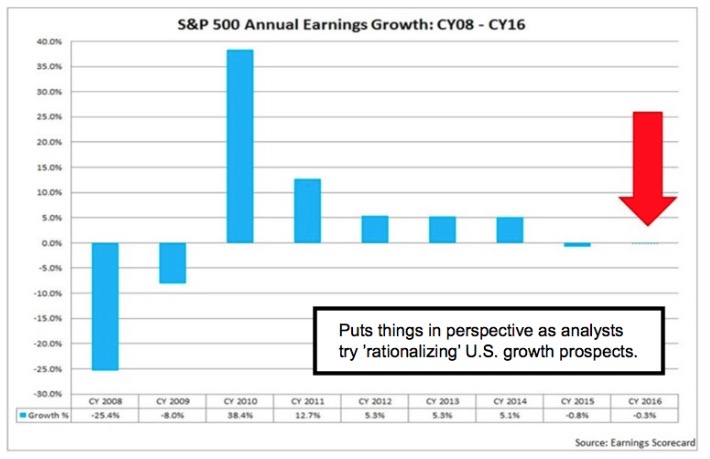

The same thing (in a sense) applies to stocks that are discounting earnings that likely aren't coming; and even if they do arrive; the irony will be if the shares (redacted).

The same thing (in a sense) applies to stocks that are discounting earnings that likely aren't coming; and even if they do arrive; the irony will be if the shares (redacted).

I think the huge money managers that didn't hedge, but leveraged bearish bets, may have the right idea about what's out there in terms of risk (we've agreed with much of it); but the wrong strategy, which for them requires a broad and prominent plunge. I'll be delighted if we (as occurred several times over the past year; most recently Brexit and of course earlier in the year) get a pattern that allows taking initial large gains on a break, and then (as discussed with our members; you're invited to join us).

I think the huge money managers that didn't hedge, but leveraged bearish bets, may have the right idea about what's out there in terms of risk (we've agreed with much of it); but the wrong strategy, which for them requires a broad and prominent plunge. I'll be delighted if we (as occurred several times over the past year; most recently Brexit and of course earlier in the year) get a pattern that allows taking initial large gains on a break, and then (as discussed with our members; you're invited to join us).

In-sum: big fund managers shorted too early this Summer in a massive way. We had a much more benign approach, which was selling rallies (primarily after the expected stability into mid-July), and then taking partial gains on those that worked (most), and using breakeven exits on the remaining portions of efforts.

Now we have managers jumping ship, as represented by the Soros CIO guy Friday. I see that as a sign of capitulation. Generally, barring 'black swans', they don't want to let this go until after the Elections one might presume. So in a sense (withheld).

But imagine these hedge or private fund guys (like Icahn too) who remain so heavily short..... and stay that way for weeks.... Many, as contrasted to our hit-and-run tactic of placing bets and then getting out (whether profitably or not; and mostly yes due to only fading strength, never weakness), are betting the ranch (or the 'back 40' as that term suggests) on catastrophic breakdowns.

(Redacted.) That's the idea as no market expectation by any of these esteemed big guys is quite as engraved in stone (they sometimes try making their own market; and they appear shocked when it doesn't work). It's why I mentioned earlier this Summer that I couldn't believe some of the rhetoric coming from these guys; especially Soros both before and after Brexit, when he was calling (in op-ed's in major papers) for the disaster that we said would NOT occur. I thought he was trading his 'book' as it's said and clearly it now looks like he (they) were. (Our view was for Brexit to vote 'leave' as well as the market to drop initially regardless, then rebound sharply to new highs for the FTSI especially, which the Dollar regained strength, which is what occurred.)

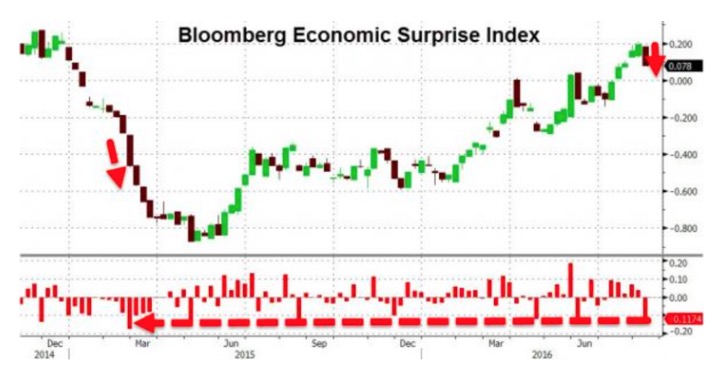

So perhaps as these huge managers work-off their shorts, we're seeing the fuel that's keeping this otherwise-indecisive trend holding together. It sure isn't economics, as is evidenced by many of the charts we've shared. And technicals remain locked in sort of an 'indecision pattern', in what is one of the dullest August ranges in ages.

So perhaps as these huge managers work-off their shorts, we're seeing the fuel that's keeping this otherwise-indecisive trend holding together. It sure isn't economics, as is evidenced by many of the charts we've shared. And technicals remain locked in sort of an 'indecision pattern', in what is one of the dullest August ranges in ages.

Daily action - well Friday we had a single-effort guideline short; really well-placed at the 2182 price level. Any retained through the end garnered just a slight gain (more if one played the intraday trend for the reversal into the 2 o'clock balloon of course); as we decided (without a stop hit but also without a sufficient cushion) to simply go flat.

Hence we enter August's 'nominal Expiration' week (reserved) flat S&P; with desires for short-sale guidelines at (reserved), as this market exhausts even the Bulls, while scrambling Bears. It amazed me (as was a main topic tonight) how persistent some major billionaires got with their bearish stance (nothing like ours, which at least is hit-and-run plus allowed the market's up moves both before and then in much of July as well as my return from England) to see seasoned veterans married to positions. I may seem married to bearish views; but it's not that simple. I've often mentioned not disturbing long-term holdings; just making sure one has liquidity for a potential better buying spot (for investors), or for those inclined, hit-and-run fading of upside spikes.

That approach has worked reasonably to those who understand it; while some will be groveling and (with hindsight being 20/20) adamant that one 'could' have been totally long all through this. Well we weren't and that is hindsight. And we did to fairly well as regards the periodic shorts. I doubt dip buyers trading from a bullish bias did better in the S&P; noting that rotation among sectors also defined a lot of the buy-and-hold crowd, because (more). Again it's tech and oil-led; as is fine by me (I was optimistic that Oil's break of 40 was a washout that would turn up; it did) but also is sensitive to how long the pattern (without improved demand) really holds. I give zero credence to stories from Saudi Arabia suggesting OPEC price accords.

We go into the new week realizing that the market's lethargy (up or down) reduces its volatility and probably lulls investors and traders into a sullen Summer complacency. I think that's fine (more). I caution however that the history of late August (reserved) is often 'anything other' than complacent even if investors (more).

It has become a 'Great Fool Theory' time. (More, including political impact, noted.)

Prior highlights follow: (includes a lot about credit markets; thus is reserved).

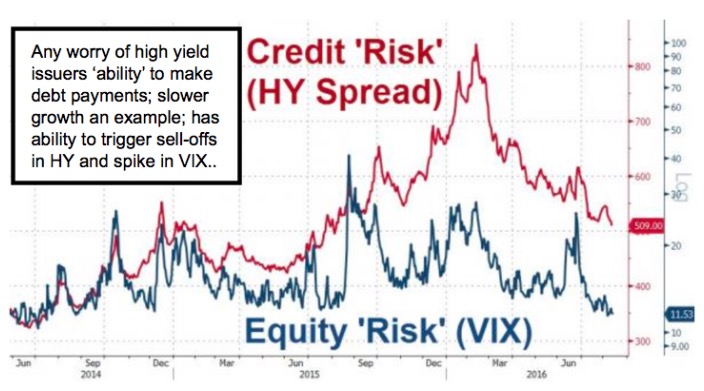

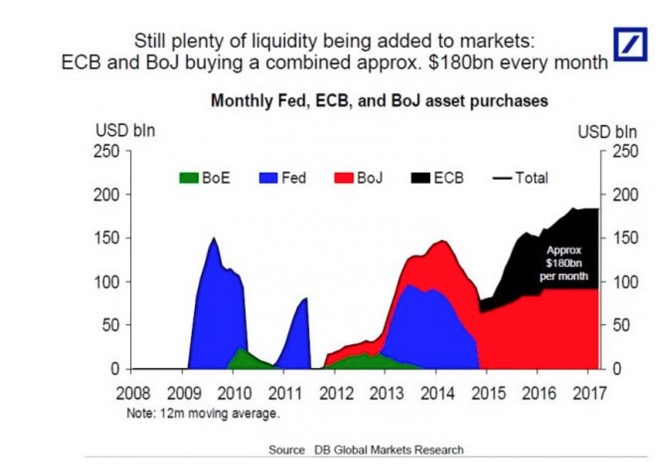

The distinction should be the 'bubble' that today's credit markets have formed; as well as the 'money-printing' binge that has shown no signs of stopping. Central banks so far have not been defeated, and we don't want to fight them; even as they are fighting the reality of the world. That reality suggests they are already behind the curve.

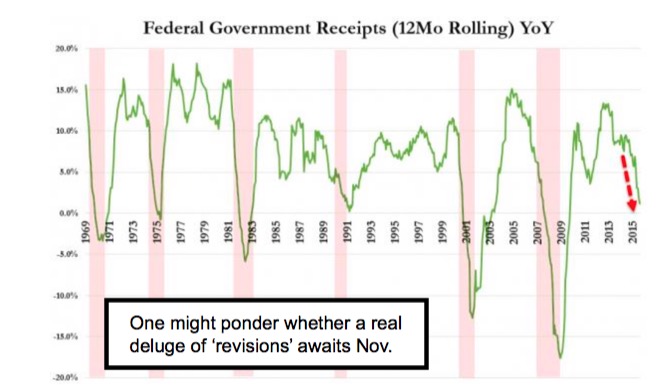

Just (last week) the Atlanta Fed Now showed a huge spike in economic activity. Isn't easy to detect (not based on Jobs, which were mostly so-called waiter or bartender service jobs), but if Atlanta is right (and they have been more on-track than the Fed itself) then you've got (redacted reality-check for members to contemplate).

Globally there are unreported tensions persisting. One is the Russian stance vis-a-vis the United States regarding not just Syria (where some cooperation exists at last so it is suggested); but Ukraine; plus the Ruble is showing some recovery signs too.

Bottom-line: the market remains extended, and the Bulls control isn't over until it's of course over. The disconnect between economic fiction, valuation and market levels is simply persisting; and changes in a decent way for the Nation if the Atlanta Fed's got it right; albeit not necessarily for the stock or credit markets.

The world remains on tenterhooks; the market is exploring rarefied air; and we'll not change (what we believe continues to be a correct approach).

Battlegrounds continue 'fluid', with multiple dynamics unfolding.

Enjoy the trading week ahead!

Gene

Gene Inger