The SEC finally gave approval to trade for eleven different spot Bitcoin ETFs, a long-anticipated action that many analysts and traders are expecting will increase demand for Bitcoins, now that ordinary investors can "own" Bitcoin in their brokerage accounts. But what the crowd believes will happen is often the opposite of what turns out.

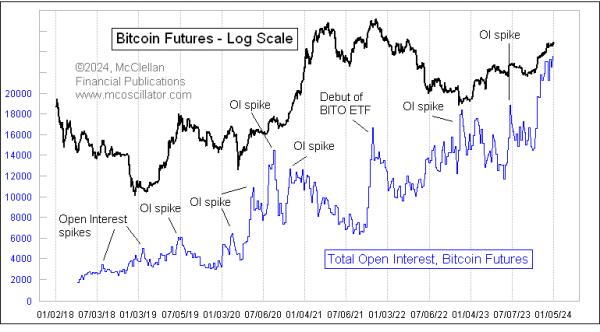

I noted here back on Nov. 4, 2023 that total open interest was spiking upward in Bitcoin futures, in anticipation of that supposed increase in demand. In that article, I featured the chart above, noting that big spikes in total open interest of Bitcoin futures usually serve as markers of important turning points. More often they are tops, but some have been bottoms.

Perhaps the most dramatic spike was when trading was approved for BITO, an ETF that owns Bitcoin futures. That debut helped to mark the all-time high (so far) for Bitcoin prices. BITO was great for investors who wanted to have Bitcoin exposure, but it had problems because of the pricing inefficiency of the futures contracts it owns. Because the Fed has short-term interest rates up above 5%, the farther-out expiring contracts of Bitcoin futures are priced higher than the near-month contracts. So, as those contracts expire every month, the fund sponsors of BITO have to "roll" into further out contracts at a higher price, which serves as a drag on BITO's performance. Spot Bitcoin ETFs will reportedly own actual Bitcoins, thus sidestepping that performance hit, although most of them will still have management fees.

This episode of BITO's debut marking an important price top is not unique. We have seen this story many times before. Back in November 2004, trading was approved in GLD, the first gold bullion ETF.

That moment of GLD's debut did not mark an exact top for gold prices, but an important top did arrive in gold prices two weeks later, and that price top was not exceeded for the next ten months.

It was a similar story for the debut of the silver bullion ETF, SLV, back in April 2006.

Once again, the day of SLV's approval did not mark the exact top, but it was part of a topping structure which endured as the high for several months afterward.

And both of these were echoes of a similar event that most modern investors won't remember. Back in 1975, Americans were finally allowed to own gold bullion again. President Franklin Roosevelt, back in 1933, had made it illegal for Americans to own gold bullion, and everyone had to sell their gold to the government as a way to push more dollars out into the economy and get everyone spending and investing again during the Great Depression. Roosevelt was kind enough to up the price from the $20.67 fix where it had stood for years to $32, so gold bullion holders at least made money on those investments (which of course got taxed as capital gains).

President Nixon finally took the U.S. off of the gold standard in 1971, mostly because it became indefensible. Running trade and budget deficits meant that the U.S. could no longer afford to exchange its gold for dollars, and Germany departed the Bretton Woods agreement in May 1971, refusing to exchange DMarks for dollars at the specified 4:1 exchange rate. By August 1971, economic pressures were so great that Nixon closed the gold exchange window, implemented wage and price controls, and imposed a 10% tariff on imported goods. Nixon's move on gold also set the stage for eventual restoration of Americans' rights to own gold, but not right away. That restoration was set to go into effect on Jan. 1, 1975.

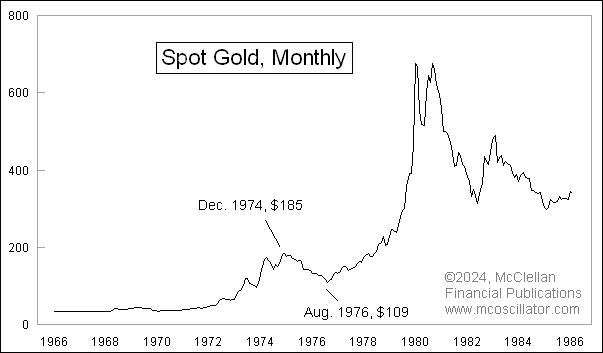

The rest of the world knew about that, and figured that all of this latent demand from Americans who would suddenly be able to own gold had to be a bullish factor. So they tried to front-run that demand, bidding up gold prices in a big way all during 1974. By December 1974, gold on a monthly closing basis was up to $185, a gain of 330% over where gold was trading when Nixon ended its convertibility.

But unfortunately for those front runners, the anticipated surge in demand for gold from American investors did not materialize as the rest of the world was hoping, and gold went into a big decline. It eventually lost 41% by the time of the August 1976 low, which led to one of the greatest bubbles of all time in gold prices during the late 1970s.

The point of all of these prior examples is that front-running a regulatory change, expecting a lot of demand to materialize, does not always work out very well for the front runners. This does not mean it has to work that way for the approval of these eleven new Bitcoin ETFs, but it is worth keeping in mind. And those prior examples in gold and silver prices did not bring permanent tops when trading was approved, but they were noteworthy tops.