There's an old Wall Street adage that says: "What's important is the return of your money, not the return on your money." This is one of those times.

With the major indexes making new highs and the market's breadth gauges following close behind, it's hard to argue with the current upward momentum in stocks. Yet, the outcome of the Federal Reserve's first meeting of 2024, scheduled for January 30-31, will likely set the stage for what happens in the stock market for the rest of the first quarter.

While the Fed is expected to keep interest rates unchanged, the market will be hoping for hints that rate cuts may come sooner rather than later. The Fed has been forecasting rate cuts in Q3, while the market has been hoping for rate cuts in March.

Part of the uncertainty has to do with persistently above-average consumer spending in the wake of the ongoing issues in the Red Sea, the rerouting of cargo ships, and the potential for supply chain disruptions bleeding into consumer prices, which combined would likely restoke inflation.

Bonds Remain in Bear Trend

The bond market has been in a bearish yield retracement since late December, when the U.S. Ten Year Note yield (TNX) fell to 3.8%. Currently, TNX retains a bearish tone, given its recent move above its 200-day moving average and the 4.1% area. Recent inflation data suggests that the rise in inflationary pressures has slowed, but the threat of higher prices remains.

Moreover, its rise has bled into the mortgage market, and the recent drop in mortgage rates has likely bottomed out.

As I noted in this post, the homebuilder stocks, which had been in a lofty bull market since October 2023, and which recently seemed poised to benefit from a potential increase in mergers and acquisitions, are suddenly starting to show some wear and tear. This was highlighted in the earnings miss posted by the largest homebuilder in the U.S., D.R. Horton (DHI), whose shares tumbled in response.

I detailed the report in a Flash Alert to subscribers, as well as in the post referenced above. Suffice it to say that it's now day to day with the homebuilders.

As a result of the confluence of these events, risk management is the prime directive for investors. That means that portfolios should be prepared for both a rise or a fall in stocks. Keep these factors in mind:

- The FOMC meeting could push bond yields higher. Stocks will likely fall in response;

- Sentiment remains too bullish. The CNN Fear/Greed Index closed at 76 on 1/26/24, remaining well in the GREED zone. This type of reading means the market is very vulnerable to bad news;

- The CBOE Put/Call Ratio closed at 0.94 after its recent high of 1.25 – the bears are losing their grip; and

- The CBOE Volatility Index (VIX) failed to rise above 15.

Here's how to manage the potential risk:

- Stick with what's working; if a position is holding up – keep it (see section on homebuilders below);

- Raise cash by reducing position size while maintaining exposure to strong stocks;

- Consider short-term hedges, such as put options and inverse ETFs. These could soften the blow if the Fed spooks the markets;

- To reduce risk of loss, consider trading options instead of stocks;

- Look for value in out-of-favor areas of the market that are showing signs of life, but build positions slowly; and

- Protect your gains with sell stops and keep raising them as prices of your holdings rise.

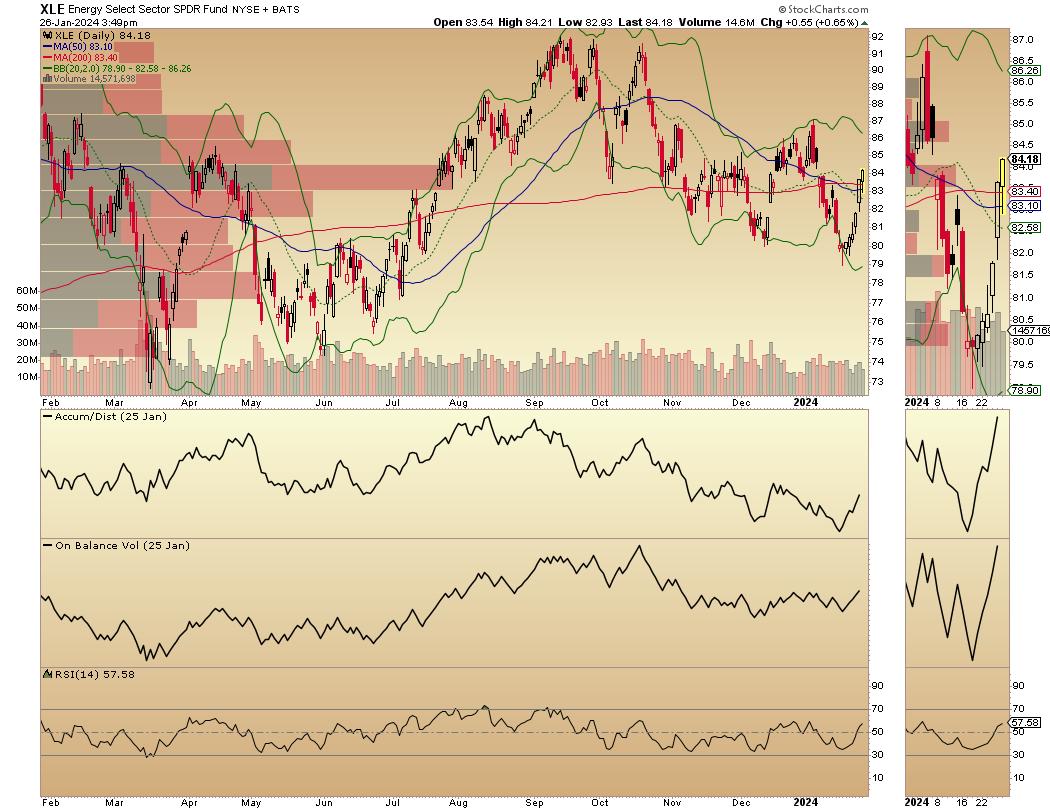

Value Sector: Energy Stocks Show Signs of Life

The energy sector is strengthening and is an example of an area of the market where value is emerging. The reasons cited for the recent improvement in the sector include better-than-expected U.S. GDP and, of course, the uncertainty surrounding the Red Sea, as potential price boosters for crude oil.

The Energy Select Sector SPDR ETF (XLE) has crossed back above its 200-day moving average with Accumulation/Distribution (ADI) and On Balance Volume (OBV) both rising. That means that short sellers are moving out (ADI) and buyers are moving back in (OBV).

Given the potential for daily gyrations in the oil market, this bullish change gives investors an opportunity to consider trading options in the sector, which is what we've been doing in my service over the last few weeks.

My latest video offers details on the successful use of put options in real time. Check it out here. For details on my latest option trades and on which areas of the market make sense currently consider a FREE Trial to Joe Duarte in the Money Options.com.

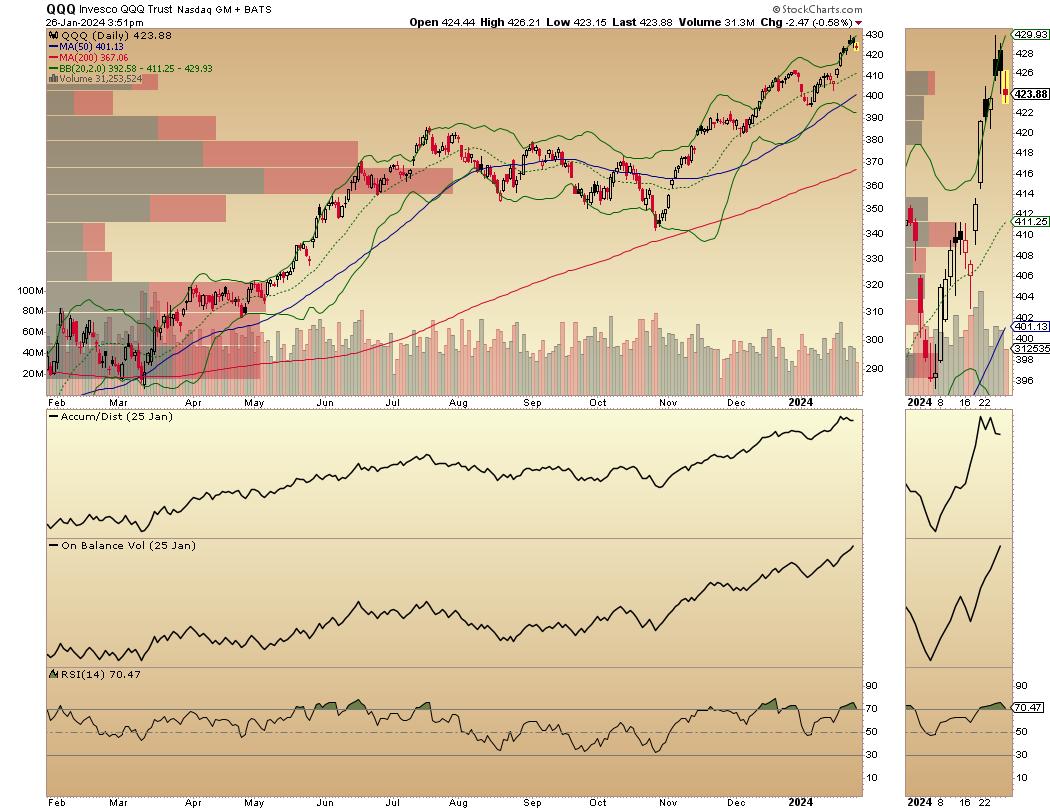

QQQ Takes a Break as Shipping Stocks Consolidate

The Invesco QQQ Trust (QQQ) finally slowed its recent ascent after its breakout, which was boosted by the earnings beat in Taiwan Semiconductor (TSM), a stock I recommended before the news was released. This action confirmed my expectations for a short squeeze in QQQ, which I described here over the last couple of weeks.

Both the price charts for QQQ and TSM continue to suggest that another short squeeze could be brewing. Note that ADI is falling and OBV is rising in both charts. Much may depend on what happens with the Fed.

Meanwhile, our weekly look at SonicShares Global Shipping ETF (BOAT) suggests that a consolidation is ongoing in the shipping stocks. On the other hand, some shipping stocks remain in uptrends.

If you saw this post, you would have been prepared for the rally in the shipping stocks. For my latest recommendations on technology, energy, homebuilder and shipping stocks and options grab a FREE two-week trial to my service by clicking here.

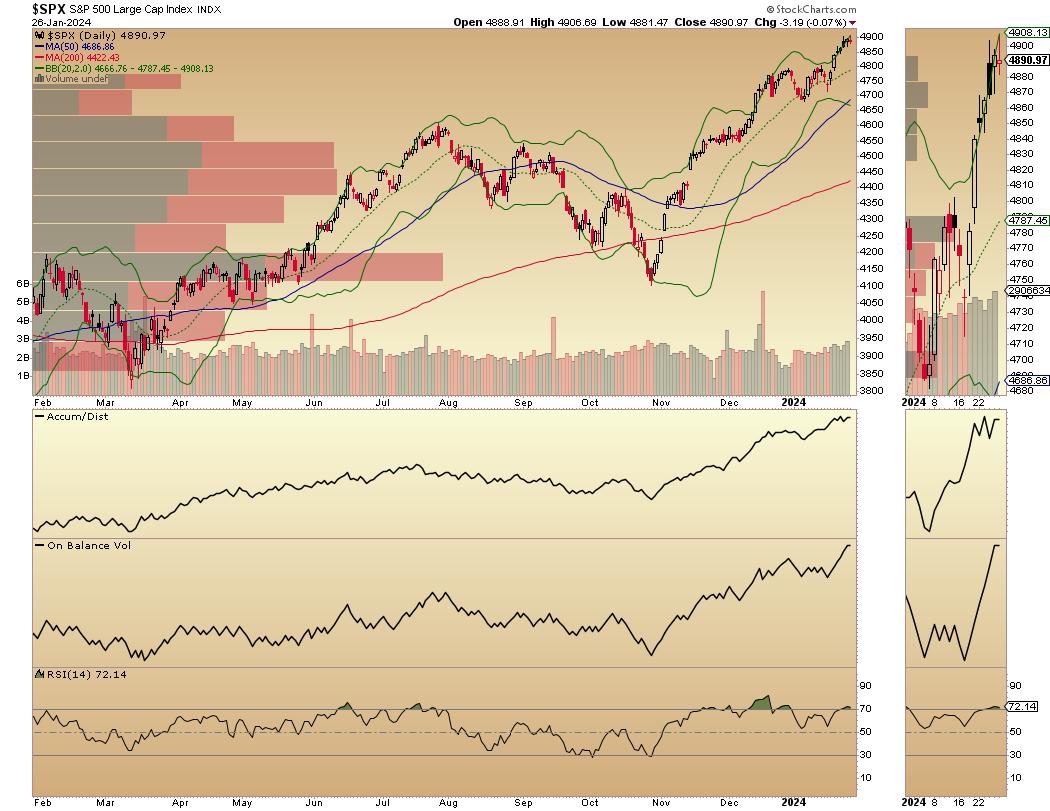

Market Breadth Rallies, NDX Rises Further Above 17,000, SPX Outperforms

The NYSE Advance Decline line (NYAD) rallied after finding support at its lower Bollinger Band after breaking below its 20-day moving average in the prior week. It closed just below a new high. This remains a positive for the market.

The Nasdaq 100 Index (NDX) remained above the 17,000 area, as the short squeeze I predicted here two weeks ago developed further. Note the rise in ADI (short sellers covering) was joined by OBV as buyers moved in.

The S&P 500 (SPX) moved ahead of NDX, closing above 4900. 4800 is now support.

VIX Remains Below 15

The CBOE Volatility Index (VIX) ran into resistance at 15. This, for now, remains a bullish factor for stocks. If VIX remains subdued, more upside is possible.

To get the latest information on options trading, check out Options Trading for Dummies, now in its 4th Edition—Get Your Copy Now! Now also available in Audible audiobook format!

#1 New Release on Options Trading!

#1 New Release on Options Trading!

Good news! I've made my NYAD-Complexity - Chaos chart (featured on my YD5 videos) and a few other favorites public. You can find them here.

Joe Duarte

In The Money Options

Joe Duarte is a former money manager, an active trader, and a widely recognized independent stock market analyst since 1987. He is author of eight investment books, including the best-selling Trading Options for Dummies, rated a TOP Options Book for 2018 by Benzinga.com and now in its third edition, plus The Everything Investing in Your 20s and 30s Book and six other trading books.

The Everything Investing in Your 20s and 30s Book is available at Amazon and Barnes and Noble. It has also been recommended as a Washington Post Color of Money Book of the Month.

To receive Joe's exclusive stock, option and ETF recommendations, in your mailbox every week visit https://joeduarteinthemoneyoptions.com/secure/order_email.asp.