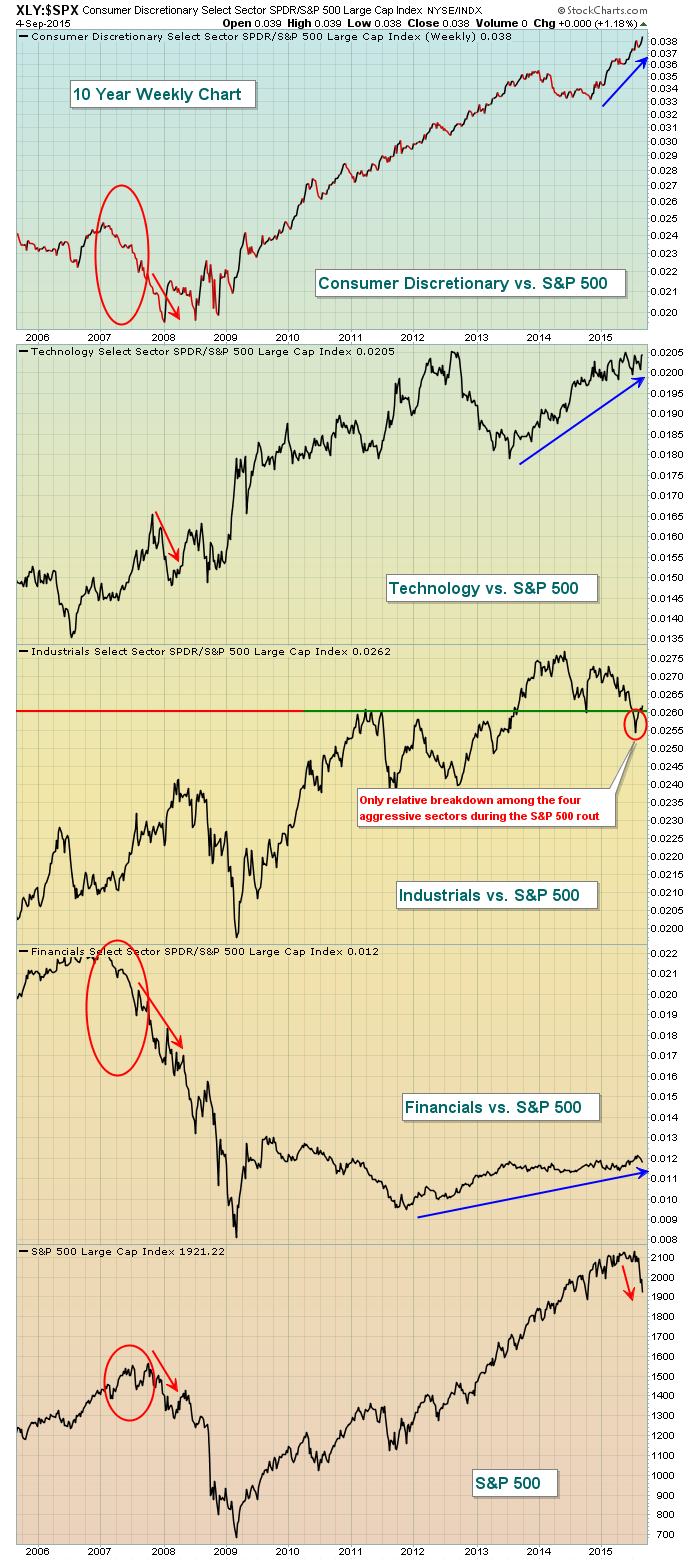

There are plenty of technical analysts calling for the beginning of a bear market after the past couple weeks of heavy volume selling. I'm certainly open to that possibility as I always respect price support breakdowns with accelerating volume. But the story behind the scenes isn't making a lot of sense and doesn't support that line of thinking. Typically, we see money flow away from aggressive sectors on a relative basis (vs. the benchmark S&P 500) before the plunge begins. The weakness recently, however, has been focused more on energy, materials and defensive groups, which is just plain odd. Bear markets can come in all shapes and sizes so I will definitely respect what's happened, but at the same time I will not be shocked if we magically resume the six year bull market once September is behind us. Compare how the aggressive sectors acted relative to the S&P 500 prior to the 2007 top to how they're acting now:

In 2007, both consumer discretionary and financials performed horribly BEFORE the S&P 500 topped. In other words, much of the smart money began rotating away from aggressive areas of the market prior to the recession that followed. And technology performed very poorly on a relative basis when the S&P 500 took its initial drop beginning in October 2007. Now fast forward to 2015 where we see consumer discretionary outperforming on a relative basis. The only true blemish with respect to the relative performance of aggressive sectors was a slight relative breakdown in industrials. A bear market generally tears apart aggressive areas of the market because those sectors are laden with high PE companies that typically free fall as PEs contract and GDP turns negative. The stock market always anticipates economic strength and/or weakness before it occurs.

But while the story behind the scenes doesn't make a lot of sense, I'm also watching our major indices and sectors struggle to clear rapidly-declining 20 day EMAs, a necessary first step to right this broken technical ship. Also, the Volatility Index (VIX) continues to print readings in the 20s and 30s two weeks after the initial selloff. During the brief V-bottom selling in October 2014, the VIX spiked above 30 but within just a few days retreated back to 15. On Friday, the VIX closed at 27.80 and reflects tremendous nervousness. Bears prey on fear and they've still got plenty to work with.

My conclusion is this. We COULD be in a transitional phase from bull market to bear market given the short-term high volume breakdowns. So until we begin to clear falling 20 day EMAs and the VIX settles back down below 20, I'll remain extremely cautious. I will be prepared, though, to become much more aggressive on the long side if the 6+ year bull market resumes.

Happy trading!

Tom