Many funds/strategies are tied to a benchmark. In fact, I think most are tied to a benchmark. The goal of these managers is to try to beat the benchmark. Some do and most don’t; yet when the number beating or failing to beat the benchmark is usually not worthy of comment, especially over time. I like to say that benchmarking is what you try to do when you have no idea what to do. The World of Finance is wrapped up in relative performance and comparison. Relative performance is a widely used investment tool, but often causes horrible investment decisions. If a client is told his or her account is up 15 percent, they are happy; until you tell them the market was up 20 percent. This often causes a client to search for a new fund or advisor who claims to beat the market. We all know that no one can legally make that promise but carefully worded marketing material can easily give the reader a subliminal message that makes them believe it can be done.

Many funds/strategies are tied to a benchmark. In fact, I think most are tied to a benchmark. The goal of these managers is to try to beat the benchmark. Some do and most don’t; yet when the number beating or failing to beat the benchmark is usually not worthy of comment, especially over time. I like to say that benchmarking is what you try to do when you have no idea what to do. The World of Finance is wrapped up in relative performance and comparison. Relative performance is a widely used investment tool, but often causes horrible investment decisions. If a client is told his or her account is up 15 percent, they are happy; until you tell them the market was up 20 percent. This often causes a client to search for a new fund or advisor who claims to beat the market. We all know that no one can legally make that promise but carefully worded marketing material can easily give the reader a subliminal message that makes them believe it can be done.

The cycle of performance chasing is the beginning of a vicious process of moving money from what is perceived to be a better performing fund or strategy. Sadly, these moves usually happen at a point in time when they should add to their current account instead of sell it. In the case of tactical unconstrained management, trying to select a benchmark to measure performance is losing sight of the strategy’s goals and the client’s investment horizon. The only benchmark that should matter is the strategy return required to meet your goals. Most will find that in their later years a strategy that meanders to the upside with minimal downside action will be their most comfortable ride. Benchmarking in the investing world is common, often used in sales and marketing, rarely of any true value to an investor who is not interested in a strategy that does not attempt to beat a benchmark. It is, however, human nature to try to measure and compare things; sadly, that trait can cause poor results. In brief, benchmarking leads to chasing performance that generally leads to poorer performance.

The following is attributed to Tom Dorsey, yet upon asking Tom if he wrote it, he said no. In any case it covers a different reason why benchmarking is so commonplace. “Comparison in the financial arena is the main reason clients have trouble patiently sitting on their hands, letting whatever process they are comfortable with work for them. They get waylaid by some comparison along the way and lose their focus. If you tell a client that they made 12% on their account, they are very pleased. If you subsequently inform them that 'everyone else' made 14%, you have made them upset. The whole financial services industry, as it is constructed now, is predicated on making people upset so they will move their money around in a frenzy. Money in motion creates fees and commissions. The creation of more and more benchmarks and style boxes is nothing more than the creation of more things to compare to, allowing clients to stay in a perpetual state of outrage.”

If you are trying to decide upon which mutual fund to buy and are looking at objectives, such as growth, conservative, or small cap, you need to know this. Most of them hug a benchmark and performance is based upon how they perform relative to that benchmark. If they beat the benchmark they call it alpha, and if they don’t, they call it tracking error. Because most mutual fund managers are tied to a benchmark, expenses can become the only discernible difference among them. Plus, on top of all that, a defensive strategy like I used to manage and treats cash as an asset class has no benchmark. I have never seen a benchmark that uses cash. Why? Because Wall Street and Modern Finance want you to stay investing at all times and rebalance often.

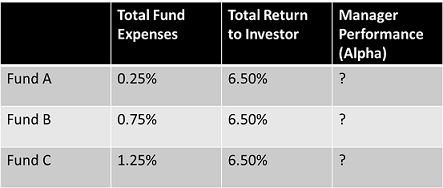

You need to understand mutual fund expenses since so many times decisions on which fund to buy boils down to this factor. Expenses can cause you to forget the goal, which is to select the fund that will give you the total return you need. Below is a table showing three mutual funds, their total expenses, and total returns. Which mutual fund is delivering the most alpha?

Fund C clearly delivered the most alpha. If Fund C generated the same total return as the other two with a higher expense, then Fund C manager produces the most alpha of the three funds. If you are momentum buyer like me, the above does not come into play.

Turnover and taxes are also often used to compare similar funds. Turnover refers to the percentage of an investment vehicle's holdings that have been "turned over" or replaced with other holdings in a given year. Most unconstrained tactical models generally yield a high turnover.

The turnover is based totally upon market action.

Low volatility trends will not have high turnover.

Short whipsaw-like moves will have high turnover.

Rarely are there any long term gains or losses.

Predominately there are short term gains and losses.

A good model will not compromise its investment process with tax considerations. Plus, there is no risk of getting a long term gain that you did not participate in. This is a phenomenon most never realize can happen until it happens and then it is too late. Most mutual funds that follow an objective will hold issues for really long periods of time, upwards of many years. If you purchase shares of an open end mutual fund, and shortly thereafter the fund manager decides to sell one of their long-term holdings, you will realize the full long-term capital gains tax, and you never participated in the actual gains.

Remember: Taxes are the consequence of successful investing.

Trade with understanding,

Greg Morris