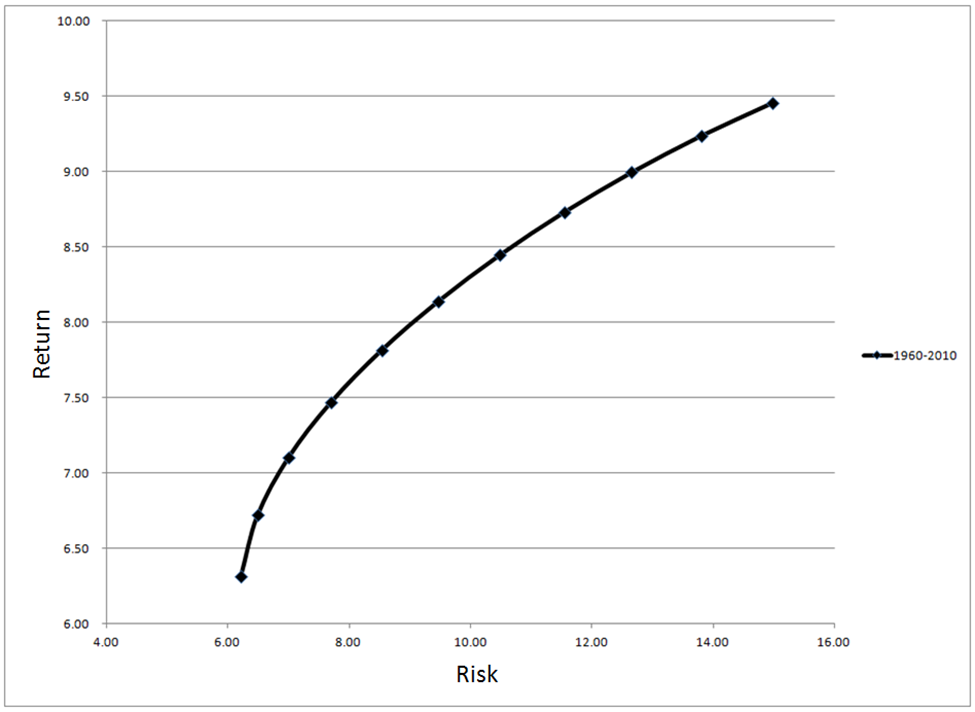

It is almost impossible to see any performance comparisons that not only show a benchmark, but also show a mix of 60% equity and 40% fixed income, known as 60/40 in the fund industry. The Efficient Frontier is one of those terms that came from a theory developed decades ago on risk management. Modern finance looks at a plot of returns versus risk, and of course by risk, they mean standard deviation. This is the first mistake made with this concept. As I have written about many times before using standard deviation as a measure of risk is flawed from so many angles it takes and entire article to describe. See article Risk is More than a Four Letter Word and What is It with Modern Finance? Then they plot a variety of different asset classes on the same plot and derive the efficient frontier which shows you the level of risk you take for the asset classes you want to invest in. Chart A shows that efficient frontier curve from 1960 to 2010 (an intermediate bond component was used). Next, if you draw a line that is tangent with the curve and have it cross the vertical return axis at the level for an assumed risk free investment, then the point of tangential is the proper mix of equity and bonds. I did not attempt to do this here as the determination of the risk free rate to use over a 50 year periods presents too much subjectivity. Guess I just found another problem with this process. From 1960 to 2010, that mix of stocks and bonds is about 60 / 40.

It is almost impossible to see any performance comparisons that not only show a benchmark, but also show a mix of 60% equity and 40% fixed income, known as 60/40 in the fund industry. The Efficient Frontier is one of those terms that came from a theory developed decades ago on risk management. Modern finance looks at a plot of returns versus risk, and of course by risk, they mean standard deviation. This is the first mistake made with this concept. As I have written about many times before using standard deviation as a measure of risk is flawed from so many angles it takes and entire article to describe. See article Risk is More than a Four Letter Word and What is It with Modern Finance? Then they plot a variety of different asset classes on the same plot and derive the efficient frontier which shows you the level of risk you take for the asset classes you want to invest in. Chart A shows that efficient frontier curve from 1960 to 2010 (an intermediate bond component was used). Next, if you draw a line that is tangent with the curve and have it cross the vertical return axis at the level for an assumed risk free investment, then the point of tangential is the proper mix of equity and bonds. I did not attempt to do this here as the determination of the risk free rate to use over a 50 year periods presents too much subjectivity. Guess I just found another problem with this process. From 1960 to 2010, that mix of stocks and bonds is about 60 / 40.

Chart A

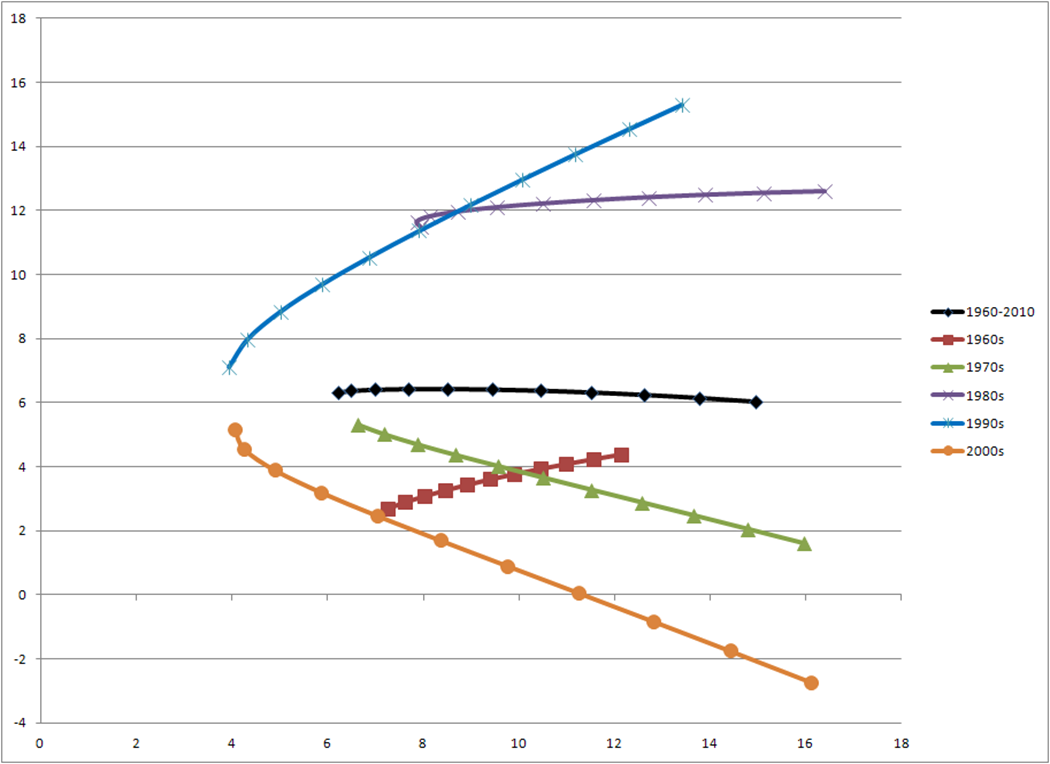

The ubiquitous 60/40 ratio of stocks to bonds which shows up in most performance comparisons gleans the message that for over 50 years of data nothing has changed? Does anyone actually believe that? Chart B is a chart showing the efficient frontier for each individual decade in the 1960 to 2010 period. Clearly each decade has its own efficient frontier and its proper mix of equity and bonds. Yet, the world of finance still sticks to the often wrong mix of 60/40. It may very well be a good mix of assets, but the data says it is dynamic and should be reviewed on a periodic basis. Notice that the decades of 1970 and 2000 showed similar downward curves meaning that stocks were not nearly as good as bonds. Conversely the decades of 1980, 1990, and 1960 were the opposite.

Chart B

In an interview with Jason Zweig on October 15, 2004, Peter Bernstein said that a rigid allocation policy like 60/40 is another way of passing the buck and avoiding decisions. Did you want to be 40% invested in bonds during the 1970s when interest rates soared? Did you want to only be invested 60% in equities in the period from 1982 – 2000 which was the greatest bull market in history? Of course not! Markets are dynamic and so should investment strategies. Finally, some analysis will show that a 60/40 portfolio is highly correlated to an all equity portfolio. The bottom line is that many of the portfolios taughted by the large wire houses are a heck of a lot more marketing than substance. They have been putting out marketing material for decades disguised as research. Nothing works all the time, except a dynamic rules-based model. And even then there are things like whipsaws and periods where you will question it’s value. Why? Because you are human.

It is odd and somewhat rewarding to begin seeing articles in the financial press being critical of the ubiquitous 60 / 40 portfolio. Some things, especially if they have been long term marketing vehicles, are hard to change.

Questions from Readers in 4th Quarter – 2015

There were not many reader questions last quarter, so will just put them at the end of this article. Recall, that I am delighted to respond to any questions and will do so at the end of each quarter. Fire away! Please!

Q - Hi Greg, How about more granular volume indicators like Laszlo Birinyi's money flow, or other indicators based on tick data such as bid/ask $ flow, uptick/down tick volume, where can one subscribe to such indicators and build breadth measures based of them? I do understand that acquiring such data requires resources and $, but I guess perhaps you could make a post on the basics such as acquiring data, cleaning it and storing it for analysis. Thanks D.

A - Dear D, I think StockCharts.com probably has the best and certainly the most robust database on tick data. I find myself looking at a tick chart when I am about to execute a trade, but have no particular feel for a process, I just know I need to execute. Plus, I believe I have mentioned in the past that I do no longer use any volume related indicators other than breadth’s up volume and down volume. Too many sources of volume these days and difficult to know what it really is. And to address the question about breadth from tick data, I think that would not be of any value since the tick is either up or down so you would only either an advance or a decline, but not both.

Q - Greg ...Awesome interview at Better System Trader...You mention Volume indicators do not work like they have in the past. I would like your opinion on parabolic volume that is seen on market bottoms and trend breaks. Secondly....I have looked at the Volume Profile indicator and I never see any repeatable evidence with respect to volume. I`m just trying to rule out another distraction in my analysis...Sometimes I feel like a fox chasing my tail...lol.

A - Dear lol, You came to the same conclusion as I did a few years ago. The volume just does not provide the information that it did decades ago. When I started managing money about 16 years go; my focus was mostly on price and price derivatives since price is the ultimate view of supply and demand. Volume profile, or market profile is certainly interesting, but again, I did not find it of any value in deciding when to buy and sell.

Q - Greg, Merry Christmas to you too. I enjoyed reading your articles and look forward to what you have to say in the new year. I would be interested in having you write more about portfolio management (if you are taking suggestions). Far too often we get caught up in the trade and not enough is talked about managing portfolios. I would like to hear your insights.

A - Your question is well timed. I am working on an outline of articles sprinkled throughout 2016 that does just that. Too often, investors and traders get so wrapped up in the indicators that they forget at some point they need to execute trades. This is a subject I will enjoy writing about since I did it for so long – with real money.

Trade Efficiently and Question Everything,

Greg Morris