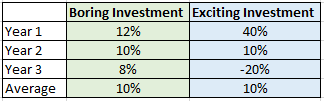

This is part of a client letter I wrote when running MurphyMorris Money Management about 20 years ago. The message is the same today. Market volatility has an emotional cost. It causes investors to make irrational decisions that are usually based on either fear or greed. Volatility also carries a steeper financial cost than most realize. Consider the two investments in Table A below. The one on the left (Boring Investment) is a dull, boring, plodding investment. It never hits a home run, but never strikes out either. The investment on the right (Exciting Investment) has lots of sizzle and excitement. It takes your breath away in both directions.

This is part of a client letter I wrote when running MurphyMorris Money Management about 20 years ago. The message is the same today. Market volatility has an emotional cost. It causes investors to make irrational decisions that are usually based on either fear or greed. Volatility also carries a steeper financial cost than most realize. Consider the two investments in Table A below. The one on the left (Boring Investment) is a dull, boring, plodding investment. It never hits a home run, but never strikes out either. The investment on the right (Exciting Investment) has lots of sizzle and excitement. It takes your breath away in both directions.

Table A

Notice how the numbers for both investments work out to a simple annual return of 10%, but here is the real kicker: Even though the investor taking the volatile ride was able to brag about a 40% up year, at the end of the three-year period, the other investor has more money! How can that be? Look at the compounded returns in Table B.

Table B

Table B

It is so much fun to have big up years that most investors spend all their energy chasing returns without ever giving a thought to what will happen to their portfolio when the bad year(s) comes along. It is important to realize how tough it is to resist the urge to chase returns. Consider the first two years for the Boring Investment. All the investor heard about everyday was the spectacular returns they were missing out on. It can be tough to rein in the short-term emotions and stick to the long-term plan when you feel like everyone else in the world has found the key to Fort Knox. Greed is a very powerful emotion to overcome. Yet it is that blind pursuit of the “big year” that can destroy a retirement portfolio. The next time you feel tempted to chase returns, ask yourself this question: What is more important, bragging about short-term returns to your friends, or creating long-term wealth so that you can live a comfortable and decent retirement?

Dance with the Trend,

Greg Morris