In light of tax season being near (albeit delayed) and that we find ourselves in the midst of a bear market, we thought it was a good time to discuss active management and taxes, which is something we are asked about regularly. We often get asked about the impact of taxes on how we invest, and if taxes erase the benefits of active management. Those are valid questions and our response is consistent – taxes are the consequence of being a successful investor.

There are a number of things to consider when trying to balance an investment approach or manager with the desire to be tax efficient. To be clear, we are not tax experts or CPAs and are not providing tax advice here, just some food for thought on the topic.

It is true that active management, and especially tactical approaches such as trend following, can create more trades and turnover in a portfolio, thus resulting in more short-term gains or losses than a passive/buy & hold approach. Those trades will have yearly tax consequences if done in a taxable account, while running an active/tactical strategy in a tax-deferred account, such as an IRA, will defer taxes and provide a better after-tax return over time. Does that mean that you shouldn't use an active strategy in a taxable brokerage account? Not necessarily.

Our trend following approach was not designed for tax efficiency per se, it was designed to provide a good return over time without suffering the devastating losses that come from bear markets. The desire of investors to always be tax efficient can even be counterproductive – if you never make any money investing, you don't have to pay any taxes – that would be pretty tax efficient, right? Taken to a logical extreme, the most tax-efficient investing approach is one that loses money consistently – allowing investors to offset other gains or income each year with their capital losses. This obviously misses the point of investing.

In 2020, short-term capital gains ("STCG") are taxed as ordinary income, with marginal tax rates ranging from 10% up to 37%. Many advisors and investors – the buy & hold crowd – think you should always hold appreciated securities for at least 12 months (if not indefinitely) in order to receive long-term capital gain tax treatment. Long-term capital gains ("LTCG") are taxed more favorably, at rates of 0%, 15%, or 20% (depending on taxable income and marriage status). We could agree with this view if the buy & hold approach also delivered the same or better performance than trend following, but we don't think it does. Sometimes it is much better to pay taxes on the gains you get to keep than to let a position with a gain unwind and turn into a loss. There are also some behavioral issues surrounding paying taxes and retirement that we'll address in our next article.

Some will argue that if you never sell your winners, thereby avoiding taxes on the gains, then there is more money left in the account to compound over time, leaving you better off in the long run. Perhaps, but there are no guarantees it will work out that way – and this sounds like something a buy & hold manager would say because they don't know how to do anything different. If you are a passive index investor, bear markets can ruin this approach. Or, if you have a portfolio of "quality stocks that never go down", you are kidding yourself. Just look at long-term charts of GE, Boeing, Kraft Heinz, Exxon Mobil, IBM, 3M, and countless other blue-chip companies that have given up 5, 10, or 15 years' worth of gains recently. People who owned these companies, and never sold because they didn't want to pay taxes on their gains, have just solved their tax problem – no more gains!

At the end of the day, what matters is the after-tax return to investors – so let's compare some after-tax results of an active approach (our Trend Plus) versus a passive approach (a typical 60/40 stock and bond portfolio).

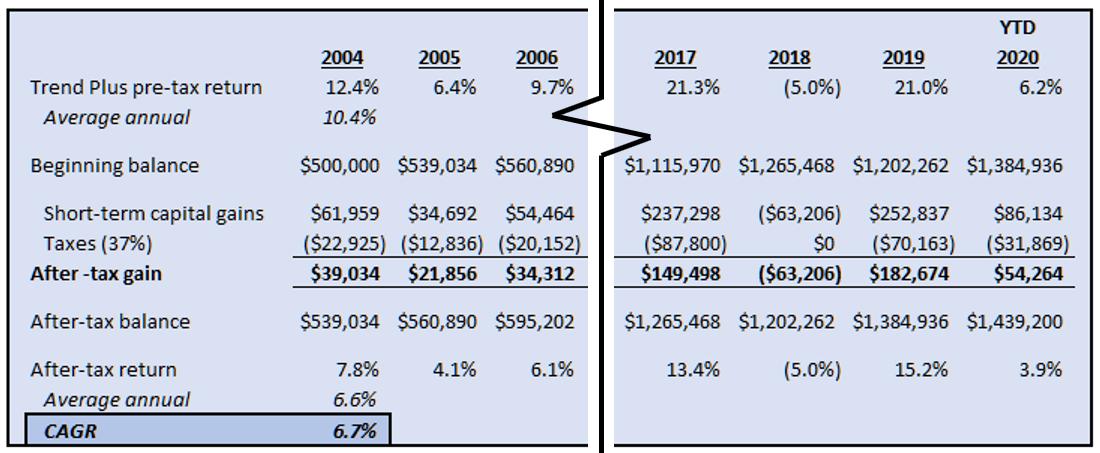

Table A is an excerpt from a schedule showing the modeled returns before and after taxes of the trend strategy (net of fees), from 2004 through yesterday's close (March 25, 2020). The years in the middle were hidden just for display purposes. Normal disclosure applies – we have not been running this exact strategy this long – the actual strategy results start in 2017.

Table A

2004 is the normal starting point we use to present our return data in marketing materials and this is more than 16 years of return data. Most investors have about 15 to 20 years of serious wealth accumulation and investing prior to retirement: you don't make much money when you are working and young; once you have a family, expenses are high and you are trying to keep up; then finally, when kids are out of the house and you're well established in a career, the serious savings and investing happens. Generally, this may start between ages 40 to 50 and end between ages 60 to 70, give or take years on either end. The 16-year history presented in Table A lines up with that timeframe. Also, the vast majority of these years were in strong bull markets, which should tilt this analysis in favor of the passive approach that we're arguing against.

For the after-tax returns, we have assumed that: (1) all gains are short-term in nature, (2) taxed at the highest current marginal income tax rate of 37%, and (3) the taxes are paid out of this account (again, all assumptions tilting the analysis in favor of a passive approach). This results in an after-tax compounded growth rate for Trend Plus of 6.7% over 16 years.

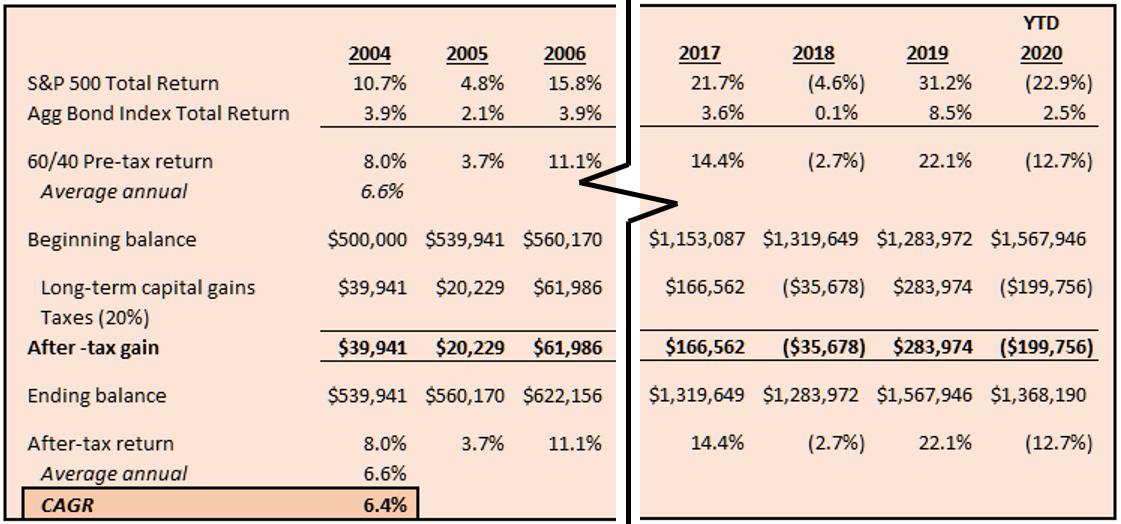

Table B shows the same timeframe with a passive (buy & hold) investment in a portfolio of SPY (S&P 500 ETF) and AGG (bond index ETF). Total returns including dividends are used for both ETFs and we assume an annual rebalance to the 60/40 weighting between the two holdings.

Table B

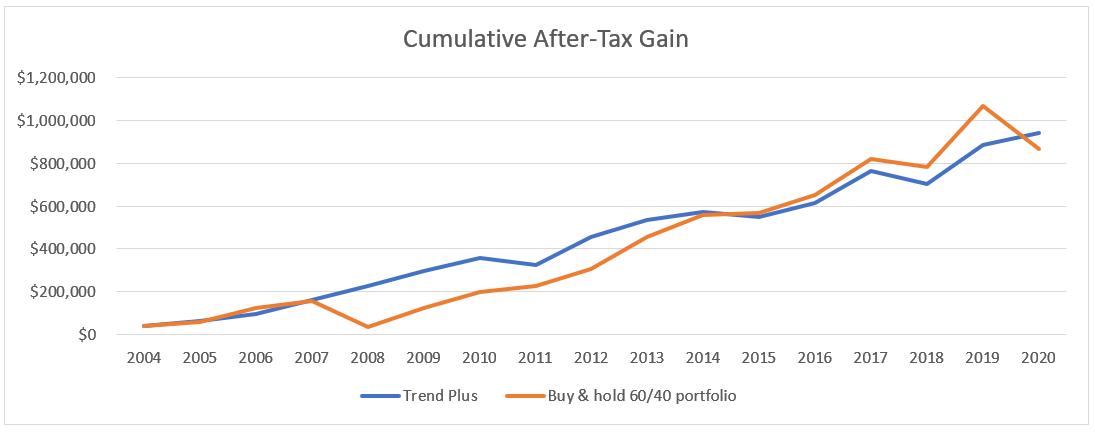

These buy & hold returns do not include any management fees paid to an advisor, and since we are assuming this is a passive investment and always deferring the taxes, we have not applied any taxes (again, tilting the analysis in favor of passive). In reality, long-term capital gains tax would apply at each annual rebalance and also whenever funds might need to be withdrawn for spending needs. Even without applying any taxes, the after-tax compounded return of this account is 6.4%, lower than the results from Trend Plus. Chart A below shows the cumulative after-tax gain of both approaches over time.

Chart A

After a historic 11-year bull market (2009-2019), deferring taxes by being a buy & hold investor did not come out ahead – further highlighting the benefit of avoiding the devastating losses of bear markets. Sure, if we stopped the analysis at the end of 2019, or picked any number of different dates, passive could have come out ahead, but look at the whole chart, not just the end point – it was very close or even behind trend for more years than it was ahead. No one knows what the frequency or severity of bear markets will be going forward – passive investing falling behind during this 16-year period is just one thing to consider.

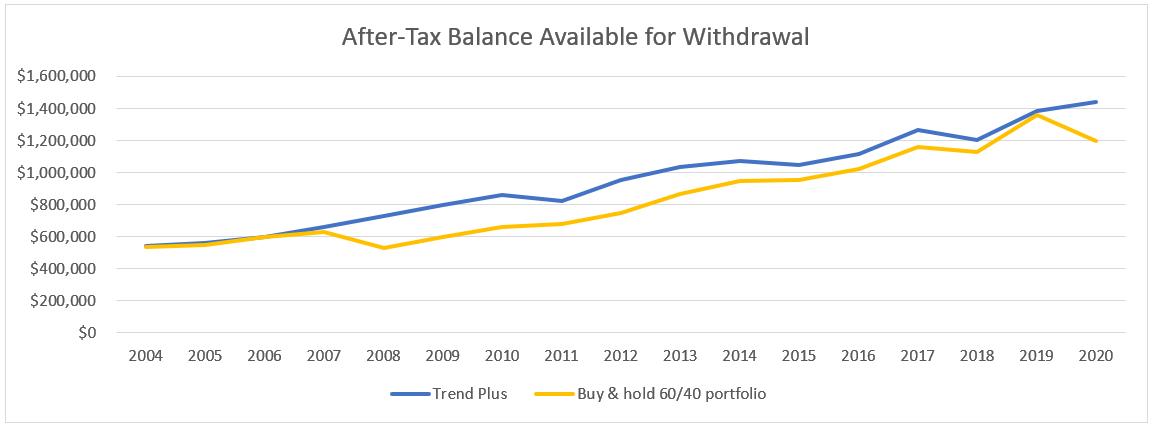

Another thing we like to look at is the after-tax balance that would be available to withdraw in any given year (not just at the end), since we don't know exactly when funds would be needed. This is a way to assess how liquid and flexible your investment account might be and to consider the fact that the tax on long-term gains will need to be paid at some point.

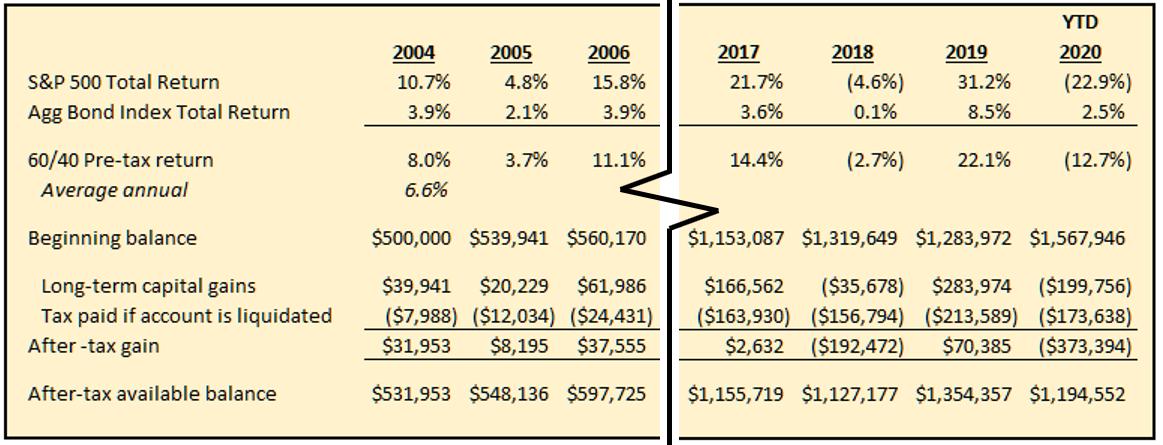

Table C shows the same pre-tax returns of the passive 60/40 portfolio, but this time, in each year we assume we need to withdraw the entire balance, and thus pay long-term capital gains of 20% when doing so.

Table C

This is not a schedule that tracks a balance through the years, rather each year is a separate calculation of what would happen in that year if all funds were withdrawn. For example, if nothing is withdrawn until the end of year 2017, you start 2017 with a balance of $1,153,087, add investment gains of $166,562 but then pay 20% taxes on the cumulative long-term gains made from 2004-2017, or $163,930, ending the year with an after-tax balance of $1,155,719. This after-tax balance available for withdrawal on the passive approach can be compared to the ending balance each year for Trend Plus in Table A .

Chart B shows this comparison of the after-tax available balances each year of both approaches. This after-tax balance is what you'd actually have available to spend on things you want in retirement in.

Chart B

Again, trend (with STCG) compares very well to the passive investment (with LTCG), matching or beating it in nearly every year, and pulling ahead of the passive approach when bear markets occur. We think this illustrates that trying to justify buy & hold strategies because of their tax efficiency is wrong.

Trend following seeks to avoid large drawdowns and bear markets, while passive investing accepts the randomness of bear markets (the frequency and severity of all future bear markets that are in your investing horizon). Trend Plus has outperformed the buy & hold approach in this timeframe because it avoided large drawdowns in 2008 and now in 2020, even after considering taxes.

Some other things to consider about this analysis and the tax implications of different investment approaches. Do you know what tax regime is going to persist while you are investing, and also during your retirement/withdrawal years? Will income tax rates be higher or lower? Will long-term capital gains always receive favorable tax treatment as compared to ordinary income? Do future changes to tax code make active or passive a better after-tax approach? Good luck guessing!

When it comes to trend following, it is true that there is high turnover because we only buy when the trend model indicates an uptrend is in place, and the holdings are always sold when our stop loss target is hit. Often, the short-term loses will offset much of the short-term gains, and the resulting tax consequence isn't much. It is certainly more tolerable than losing money. If your advisor or broker is concerned more about taxes than investment performance, you should find another advisor or broker.

If a client receives a large tax bill at the end of the year for capital gains, we sort of expect a "thank you!", because that means we made them a lot of money.

Dance with the Trend,

Greg Morris