In spite of all expectations, NIFTY remained volatile and did not make any directional call over the previous week, oscillating in a defined 230-point range throughout. However, on the weekly charts, the NIFTY has been able to keep its head above the 50-Week MA, which is 10757. Additionally, the market returned all of its gains from the prior week as it ended down 126.40 points (-1.16%).

The coming week is set to remain eventful, with the expiry of the current derivative series on Thursday, followed by the presentation of the Interim Budget on Friday. There are expectations that this interim budget is likely to be almost a full-fledged budget, even with general elections being just couple of months away. Given the events that the markets will face in the coming week, the presence of volatility will be obvious, which may keep the range for the markets wider than normal.

The Indian market has relatively under-performed its Asian and other global peers in the previous week. Since the NIFTY has kept its head above the critical support levels, with global markets stable and positive, we can once again expect a stable start to the week. The zones of 10900-10950 will continue to remain an important zone that the NIFTY will have to move past for any meaningful and sustainable up move.

With a stable start to the week expected, the levels of 10900 and 11130 are likely to post resistance on the upside. The downsides, if any, will find support at the 10700 and 10650 marks.

The weekly RSI is 49.9822; it remains neutral and shows no divergence against the price. The weekly MACD remains bullish as it trades above its signal line; PPO, too, remains positive. A small engulfing bearish candle has emerged. The size of the candle is much smaller than usual, but it may potentially set a base for a bullish reversal since it has emerged near the support area. However, this will need confirmation on the next bar.

Upon close examination of the weekly charts, it can be seen that the NIFTY has been consolidating around its 50-Week MA for over eight weeks, with higher-than-normal volumes. If this is noted along with the narrowed trading band on the daily chart, it becomes more than evident that the markets are now overdue for a directional move on either side. As the markets wait for a trigger, we suggest not chasing the upsides blindly, but look to see if a decisive move beyond the 10950 mark is made. Unless this happens, all up moves should be used to protect profits at higher levels. Purchases, if any, should be kept strictly stock-specific and modest. A cautious approach is suggested for the week ahead.

Sector Analysis for the Coming Week

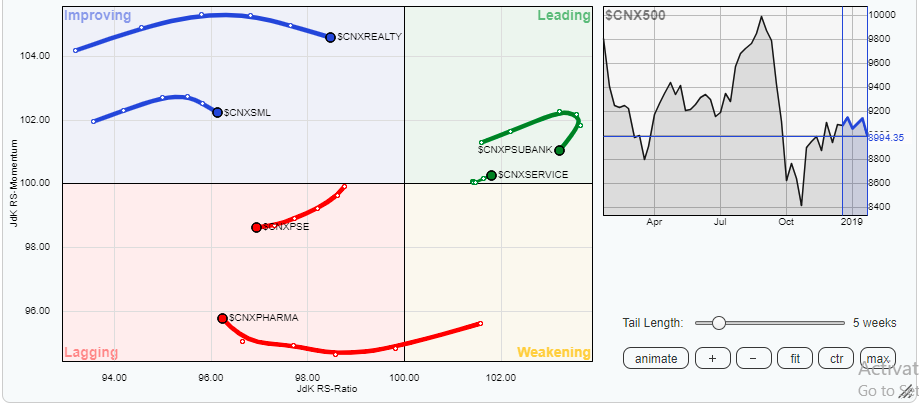

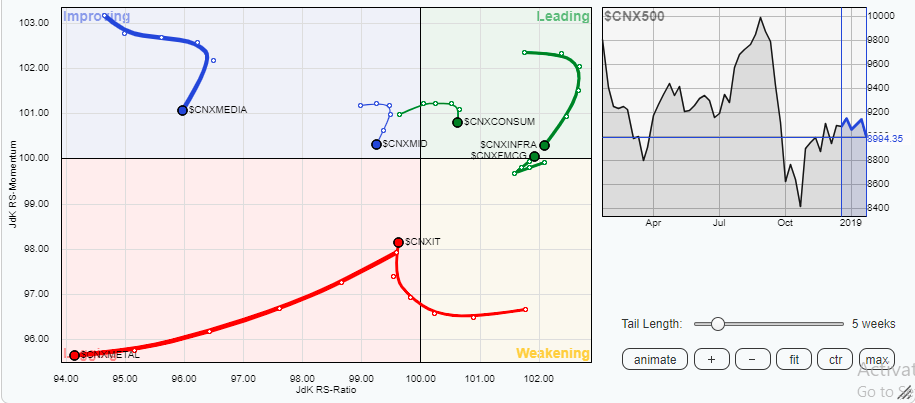

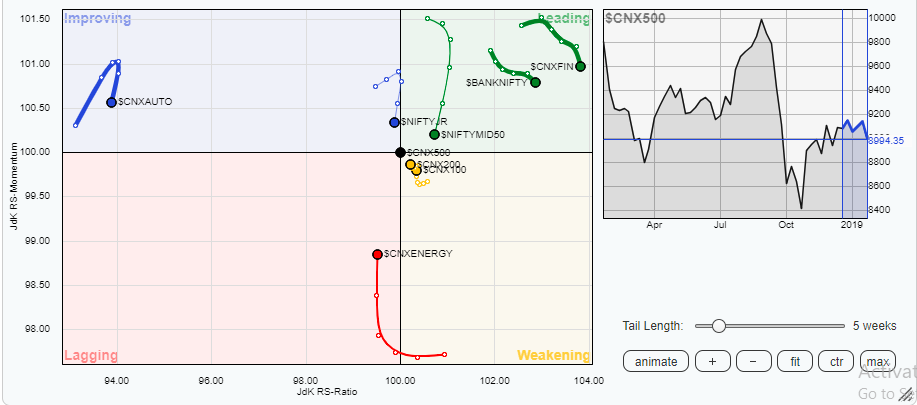

In our look at Relative Rotation Graphs, we compared various sectors against the CNX500, which represents over 95% of the free float market cap of all the stocks listed.

In looking at the Relative Rotation Graph (RRG), it can be observed that most of the indexes like Financial Services, Infrastructure, BankNIFTY, NIFTYMID50, Consumption and PSUBanks are taking a breather and slowing down while mildly losing their momentum against the general markets. These groups are expected to show milder performance unless given some triggers and will be seen consolidating their positions.

On the other hand, the FMCG has reversed its pace and moved back into the leading quadrant. Along with this, a sharp improvement in momentum can be seen in the Energy and IT indexes. CNXPharma, too, is seen bettering its relative momentum. These packs are expected to collectively improve their performance against the broader markets, even as they remain in the lagging quadrant.

The Auto pack appears to be faltering again and sharply losing its momentum, even though it remains in the improving quadrant. Though some stock-specific gains can be expected from the Realty pack, no major show is expected from the CNXPSE, CNXMID or CNXMedia indexes in the coming week.

Important Note: RRG™ charts show you the relative strength and momentum for a group of stocks. In the above chart, they show relative performance as against the NIFTY500 Index (Broader Markets) and should not be used directly as buy or sell signals.

Milan Vaishnav, CMT, MSTA

Consulting Technical Analyst

www.EquityResearch.asia