After meeting resistance around 11800-11840 for seven weeks, the markets loosened up a bit over the past week while ending with losses. NIFTY spent the previous couple of weeks in a defined range as it remained indecisive and did not make any convincing directional call. This week, the NIFTY witnessed some increased corrective pressure from higher levels and ended with a net loss of 258.65 points (-2.19%) on a week-to-week basis.

The coming week may see a stable start, but the levels of 11700 and 11865 will act as immediate resistance levels. Supports come in at 11440 and 11300.

The Relative Strength Index (RSI) on the weekly chart is 52.5485; it remains neutral and does not show any negative divergence against the price. The weekly MACD has turned bearish following a negative crossover; it now trades below its signal line. A falling window occurred on candles. The falling star pattern has emerged on the candles as the bottom of the previous shadow is above the top of the current shadow. Such a formation usually results in a continuation of the downtrend.

The pattern analysis of the weekly chart reveals that the NIFTY failed to breach the crucial double top resistance formed in the 11800-11850 zone. It appears that the NIFTY formed a congestion zone while making several failed attempts to break above the resistance, before subsequently giving up.

The index presently trades in a secondary channel after breaching its more significant 30-month-long upward rising channel in October 2018. The NIFTY can be seen slipping towards its lower support of the rising channel. If this level is breached, then the possibility of the NIFTY testing its 50-Week MA cannot be ruled out over the coming days. All up moves, if there are any, will keep the markets in a defined range and will remain vulnerable to selloff at higher levels.

Given the present technical setup, we recommend keeping exposures at very modest levels on either side. As the markets are oversold on short-term indicators, it may see some technical pullback, but, again, these pullbacks may not be sustainable at higher levels. We recommend staying highly stock-specific and approaching the markets with caution over the coming week.

Sector Analysis for the Coming Week

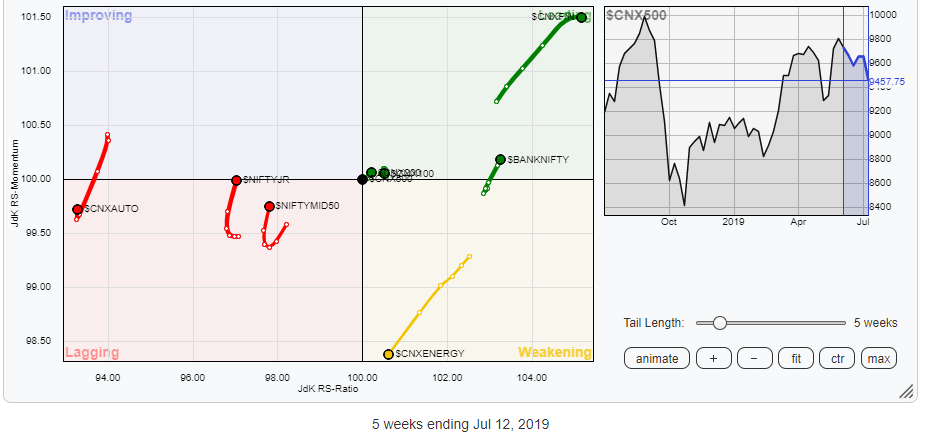

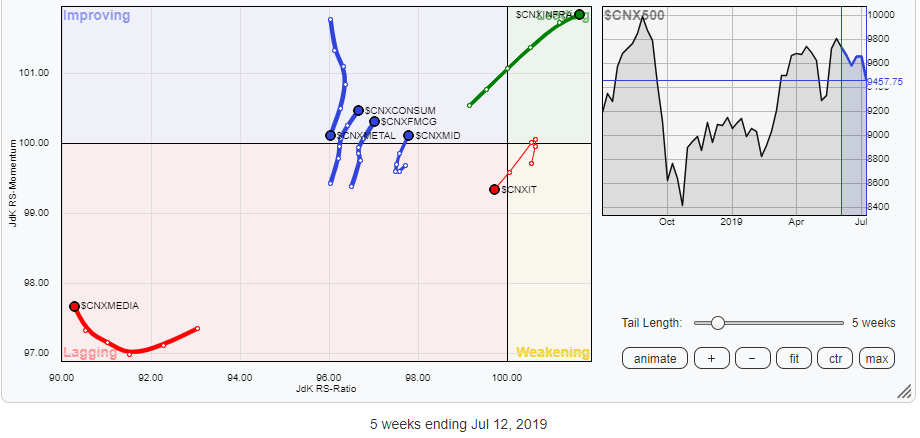

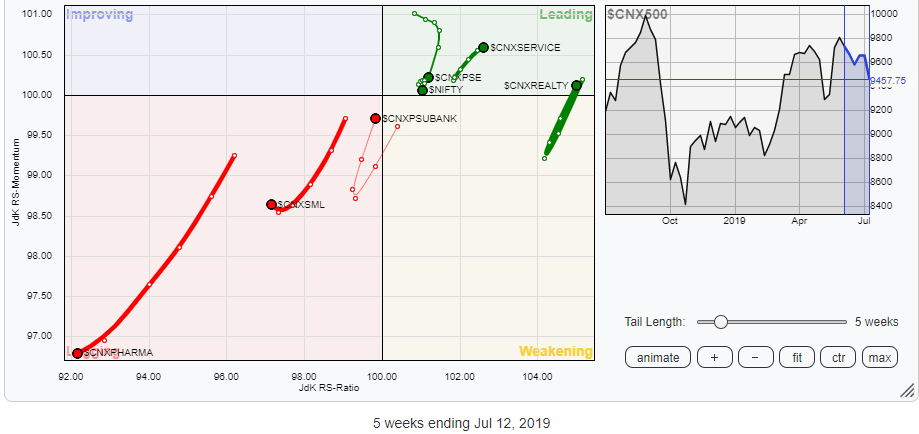

In our look at Relative Rotation Graphs, we compared various sectors against CNX500 (NIFTY 500 Index), which represents over 95% of the free float market cap of all the stocks listed.

Our review of Relative Rotation Graphs (RRG) continues to present a mixed picture. The BankNifty, Financial Services Index, Infrastructure, Services Sector Index, PSE Index and Realty Index are presently placed in the leading quadrant. Out of these groups, the Realty pack has made a U-turn into this quadrant fueled by stark improvement in its relative momentum. The Infrastructure, Services, and BankNifty are seen inching higher, and these groups are expected to relatively out-perform the broader markets. In contrast, the PSE and Financial Services group are taking somewhat of a breather.

The Midcap, FMCG and Consumption indexes have crawled further into the improving quadrant and may continue to see stock-specific out-performance when compared against the broader NIFTY 500 Index. The PSU banks can also show some resilience as compared to the other sectors.

Apart from this, the Energy, IT, Pharma, Media and Auto indexes are drifting and can be seen steadily giving up on their relative momentum. These may relatively under-perform the broader markets.

Important Note: RRG™ charts show you the relative strength and momentum for a group of stocks. In the above chart, they show relative performance against the NIFTY500 Index (Broader Markets) and should not be used directly as buy or sell signals.

Milan Vaishnav, CMT, MSTA Consulting Technical Analyst www.EquityResearch.asia