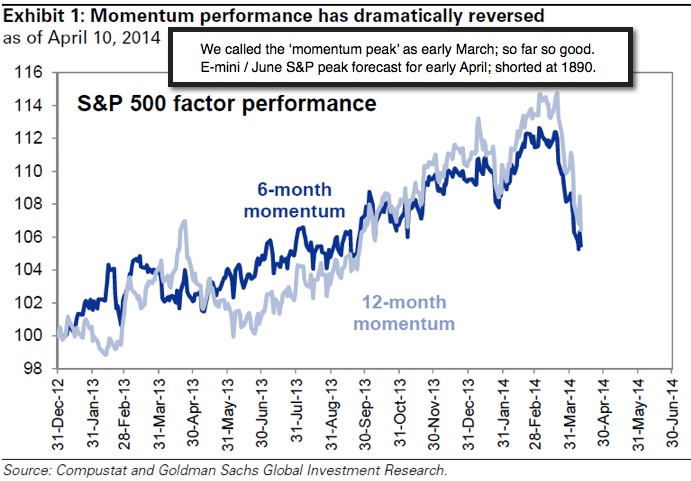

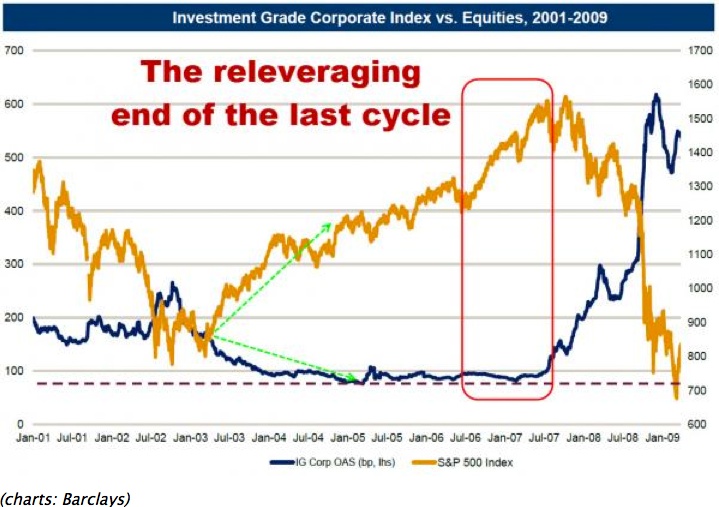

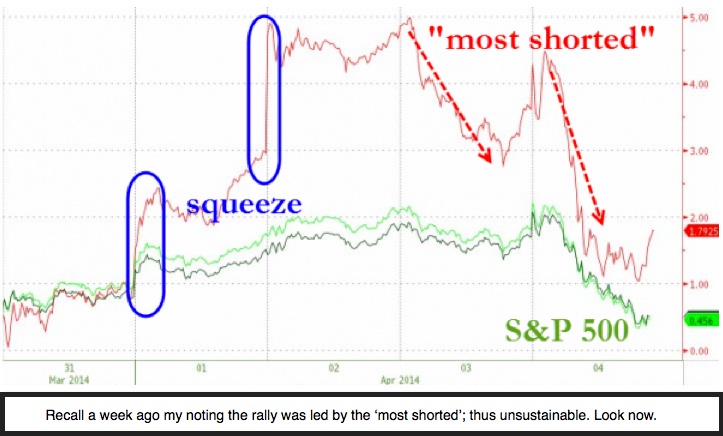

Breaking the momentum sectors - set-the-pace for constructive destruction, at least initially. For several weeks (since early March) we noted rotation out of the 'most shorted' stocks defined as 'growth' into 'value' or 'defensive stocks' (typically Oils, utilities, anywhere they could park money with or without yield), believing that masked the distribution we contended every day as ongoing.

During that month-long time, leading to the position-posture E-mini / June S&P 1890 short-sale (still retained) we captured alternating maret moves; at the same time emphasizing an internal distribution; effort to 'cash-out' by virtue of IPO's (not just an issue of consuming money that might go elsewhere, as so many contended; but I denoted people were either engaged in insider sales, or doing IPO's, to get their money out before the 'house of cards' really fell apart).

All the while, and to this day, the majority of analysts contend it's a bull market; pointing out the term 'meltdown' doesn't describe the move only a few percent off the high. But they fail to note that when they come around to 'your' sector; it is going down not 5-10%; but 20-40% and pretty aggressively at that. What will not be mentioned are things such as: (sorry balance is just for our members).

At the same time (as we addressed the other night) they twist the leverage or record margin aspect to imply 'margin means confidence'; or 'fear outpacing greed' (without mentioning that it's not fear as such, but realization traders with 50-90% leverage can be wiped out by a mere 10-20% move of the market; so they must run for the proverbial hills just as fast as they can). It's glorified spin for all the reasons outlined; as I thank members for your kind comments about how we navigated this entire saga since last year.

March / early-April Keyhole Exit Shut

That's why I said the so-called leveraged professionals, not individual traders, would be first to panic. Analysts waste time 'comforting' or 'hand-holding' the public, when the general public isn't heavily trading; the hedgers and 'pro's' are the ones engaged in leverage. That incidentally is part of 'why' this decline, when viewed overall or with respect to most-killed stocks ('net, solar, biotech or others to come), accelerates on the downside rapidly, as they 'evacuate' due to their exposure or to protect basic capital. Very little to do with individual stocks.

We're honored to have closely-called every meaningful market swing this year (and late last yea, in one of the most complex manipulated environments I've ever seen (and I mean because of Fed facilitation, not just HFT, and so on). At the same time, to us, the distribution has been obvious; while analysts shuffled guidance or estimates to fit the prices; rather than the inverse (dangerous, and also why we predicted months ago most guidance would be lowered over time; including GDP estimates here and abroad, as it was never 'just' weather).

(Redacted) as outlined repeatedly (about S&P's vacuum underlying immediate price levels); we've entered that zone, having rallied and declined as forecast all through these past three weeks; including a very important point I made Thursday; two outside-down days (key reversals) in one week's time. Fortune has it we shorted both times just-in-advance of the breakdowns; catching them.

It was tiring but important that I distance myself from emotional perspectives so prevalent among traders and media this past week; to objectively recognize the rebound on the 'unknown' FOMC meeting / clarifying minutes changed nothing at all substantively; hence we ideally looked for the frantic short-covering rush to 'peter-out' with no follow-through Thursday. In advance I expected midweek rebounds anyway; so it was just a bit more feisty for a couple hours. Perhaps it is worth mentioning that in a 'Bear Market', rallies will be brief but very sharp; a normal characterization of counter-trend moves. Technicians say (much more follows; love to share but we don't take advertising; so really do need you to be a member if you find this useful).

Hard to believe it's only been a week; but as you know we projected upside on the Employment Report 'regardless' of whether it was good or bad; expected it to be sold-into; saying in advance we'd short it. Did so; remains our (incredible) E-mini / June S&P 1890 short-sale position guideline. Subsequently; since I looked for this week's midweek rebound to be a 'B' wave in an A-B-C decline ('C' underway at the moment), we gave another opportunity to short the S&P at 1861 Thursday. That too remains 'live' (newly realistic, since we expected most traders to take 30-40 handle humongous gains early this past week before the rebound; at the same time we did the 1861 short as a spot to resume shorting.

Now that one has an unbelievable almost 50 handle (5000 point) gain in just a couple days. I suspect some will harvest gains during (reserved for members).

As such patterns often unfold, you get downside, a quick rebound (as it rarely pays to short weakness), and then try to resume downside. While we'd be very foolish not to allow for some rebounds (when and where for members).

(To the extent they think it's only about money and leverage; not earnings and credit markets... any who think that way are making a big mistake. Not to in any way overlook the extended nature of the Averages relative to economic growth, which just happens to be why we see downside risk for greater than most will even contemplate. You don't trade for -this is reserved- for regular members.)

This market reflects everything from overvaluation; to geopolitics, to 'tapering'; to Goldman perhaps exiting the Sigma X 'Dark Pool' Business. The industry is transitioning itself; to reduce leverage and get out of controversy or exposure. I therefore suggest titling what the 'Decline of 2014' is about: 'de-risking'. (It's beyond simply 'risk off' versus 'risk on'; it about -reserved for members.)

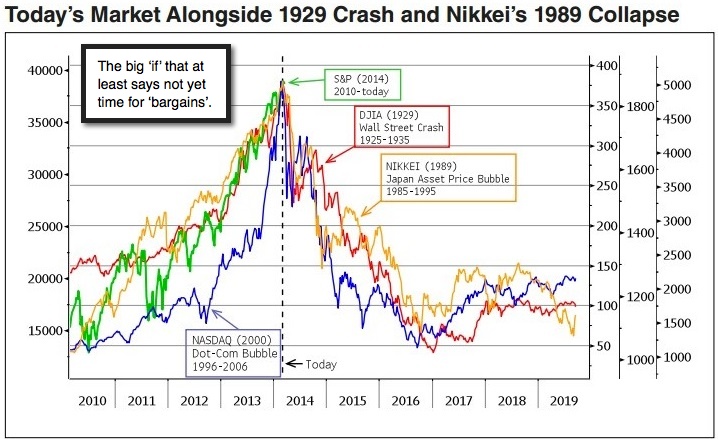

It's important to realize that we had a year of unwarranted 'push' for the S&P as fictional growth was also pushed. While already 'down for the year'; this has no reason to be a (redacted), when viewed later this year in retrospect. That's not requiring any action on your part now; because you're already protected plus profiting in the decline. (Pattern ahead discussed with our daily readers.) Just as all year: as buybacks, insider selling, and lots of IPO's were warnings of big transitioning from bull-to-bear, this is a 'process' not a (conclusion follows).

Daily action - conformed to both our expectation and intraday reflections also; as there was a fairly snappy morning rebound Friday, which we thought would 'not' gain traction like a couple days back, and fade shy of June S&P 1830. As it did, we suggested that anyone who 'scalped' gains on the daily 1860 short of Thursday either near the finale that day, or into weakness early Friday since we had suggested carrying it overnight (hence yielding an incredible 30-45 handle gain depending on whether one retained it overnight).. then go short anew.

As it turns out, that also worked out well for intraday scalpers. In no event was any mental stop touched; so one could still be short from Thursday's 1861-62 level, and certainly with the 'inflection point' position-posture short from 1890 a week ago. We added the 1861 E-mini / June S&P short guideline not only as it conformed to our forecast 'B' wave reversing with little follow-through Thursday but also as there's been so much volatility we didn't suspect many stayed 'live' in shorts for the entire week since Friday's proclaimed June S&P 1890 top.

Nevertheless June S&P 1890 continues to represent my belief early April peak realized, upon the projected phony rally on Jobs numbers last week, (expected reversing up-to-down regardless how those number got reported.) Simple: we stayed short and added a new short at S&P 1861 early Thursday this week.

Again don't get excited about panic; and if the market crashes; (forward hints).

Prior highlights follow:

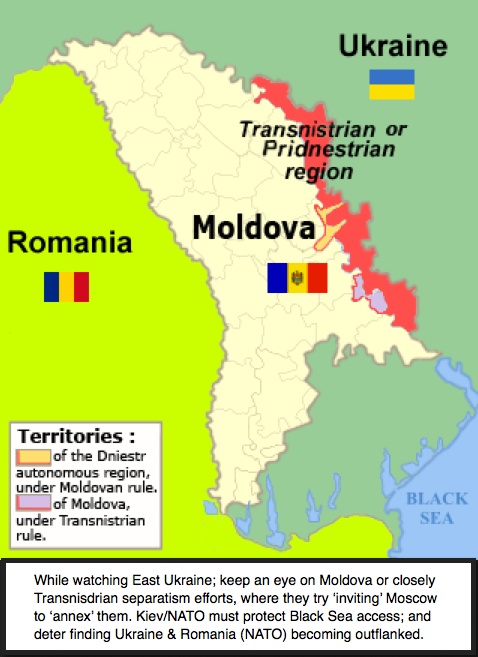

Geography determines destiny - is a rather well-known prophetic geopolitical expression, that handily is used by pro-Russian sympathizers or propagandists to justify the suppression of the legitimate sovereign rights of Ukraine.

But also 'geography' can be a form of 'mapping' the stock market, where all the 'boisterous' pundit optimism will not offset the market's destiny implied by break points coming-out on the charts. Algorithmic and conventional technical analyst traders and investors cannot deny the factual behavior of the charts. (More.)

For a moment let's return to the 'Eastern Front', as it does matter to markets in so many direct or indirect ways. The media today was talking about protester occupations in buildings in Donantsk, East Ukraine. I reported that last Sunday; and also noted Tuesday morning that Ukrainian Special Forces (much more).

This is suggesting that Russia believes 'only it' can determine regional futures, or political structures, in neighboring areas. A dangerous precedent if allowed to get away with it; and one that will impact global growth; the price of Oil; lots of currency shifts (and even currency wars); and ironically help Europe and the United States focus on being self-sufficient not only in energy; but emphasizing home-grown manufacturing capabilities (so much of was mostly dismantled).

Here's the rub: while there's an historical history of Crimea as part of Russia; it is different with respect to Ukraine; although communism had its roots there (of course most think about the Bolsheviks attacking the Czar's Winter Palace in Saint Petersburg, but communism's origins were really in Kiev. Khrushchev in 1954 returned Crimea to Ukraine; Khrushchev himself was Ukrainian. So there is a close cultural, but not sovereign, relationship. Moscow has done more now to restore nationalism and a sense of (balanced reserved for regular readers).

Clearly Putin's 'mindset' isn't merely about expanded territory. His worldview is shocking Washington as it's not the perspective of the 'new world order' (more).

At the same time we've never cared for the 'new order' because of how it would make everyone so interdependent that it would slow recovery (as is the case of course as you see). The desire to reduce exported monetary policies abroad (a risk that leverages too much of the world 'as if' it were run by Goldman and the Fed), is being resisted by some responsible nations, such as Germany and of course Austria and the Nordic countries; but that's not the point in this remark.

Washington seems stunned weakness in the West (lack of capacity to finance 'expeditionary forces' or armament equivalent on the ground to counter Russia) is being exploited by Putin. (More on the topic and the expected escalation.)

Why are they surprised? Are they naive? (I won't answer that.) Putin indicated for a couple years now a degree of independence and even confrontation that the West pretended was non-existent. Anyone noticed (this is for members; I'm hoping you understand as this is what we do; nothing more; nothing less).

Knowing this, Putin moves now. The West is weak; the U.S. is tired from wars. Ukraine actually is more important as a buffer between Europe and Russia as this evolves (large portion redacted) Turkey too; which shows the ramifications of a policy naivete in the U.S., and an opportunist Moscow trying for an ascent.

Bottom-line: symbols are a powerful 'visual' clue in political theater. Putin can not legitimately claim a symbolic pretext for protest-based intervention; in the way they cry 'foul' when anyone resists their adventurism. The propaganda is fairly transparent; as they accuse everyone but LA and Chicago street gangs of interfering with their agitators trying to destabilize East Ukraine. NATO needs a fast and transparent (rest reserved for our Daily Briefing members).

(There's more; mostly technical analysis; but I covered more than the usual 'highlights', as I want to give a flavor of our flexible nature in addressing what needs addressing in markets, which varies at times; it's not a static formula.)

(For new visitors; a summary of what we wrote last week to sum-up the flow to here.)

Two weeks ago - we staunchly embraced these prospects: 1) that there would be an effort to extend the S&P above the 'double-top' in early April, as a result of Quarterly Re-balancing being out of the way (relief rally of sorts), and also a bit of support from the last vestiges of 'seasonal reinvestment funds flowing in'; 2) the 'shift' from 'already faltering' momentum stock leaders into 'laggards', as so many pundits urged, along with buying of energy stocks, would 'cover' what already was an internally-topped broad stock market; 3) some of this occurs as mutual funds are not allowed to short or have a high liquidity percentage; so it's their shifting to be as defensive as they can, that reflects this characteristic (it's not a conspiracy but we called it a 'rearranging of the Titanic deckchairs' due to this required behavior of many money managers); 4) such behavior historically correlates with either the end, or near the end, of an uptrend; 5) that the equity market would 'not' survive April / May without a meaningful shakeout or worse; and finally 6) that ideally the ensuing two weeks (now ended) would complete this activity; setting-up the Averages to reflect the ongoing internal distribution.

During the preceding year's advance, 'monetary policy' has been doing virtually all the heavy lifting. The profitability outside a handful of technology leaders or financial firms (many of which won't have the same backdrop for free-wheeling trading and profits as we forewarned as well) was due to productivity; which in many cases helped bottom-line but not top-line results. Furthermore repeatedly focused on 'global growth slowing'; misplaced optimism about a greater growth prospect in Europe & Asia too; not just the USA (affirming our view 'weather' was 'a' factor', not the 'only' or even key factor of slowing).

Our view has been that it's not a terrible economy in some ways; but that Fed policy drained capital out of the private sector; absence of fiscal policy throttled recovery for a long time. Even decent growth rates couldn't justify price levels artificially achieved by virtue of Fed facilitation. It meant downside risk could exceed (certain levels; we suggested both investment & trading strategies.)

Special note: I would like to congratulate stockcharts.com on their recently completed acquisition of DecisionPoint.com . We enjoyed many years as a participant in 'Top Advisors Corner' section. We were with Carl Swenlin, it's founder ,all the way back since it was part of CompuServe and later AOL (American Online), and when he began his own site until now. Carl is an early pioneer of computerized charting; with roots back to my original LA financial TV show, along with Sherm McClellan, the late Kennedy Gammage & others.

The merger adds their talents to those of Chip Anderson, John Murphy, and other analysts at stockcharts.com. Their service is complimentary to ours (as we provide objective assessments probabilities across a wide range of market aspects), and are pleased to continue sharing a few of our thoughts, as 'Top Advisors' effectively becomes a 'weekly blog' within their service. This doesn't preclude our continuing our 'highlights' to our own group of investors not yet determined to take the market seriously enough to subscribe. No 'Holy Grail' to nail the market; but lots of understanding can assist informed investors. On occasion, we do nail the market (humbly, such as every key move this year).

There are lots of hard challenges ahead; and this time, there must be sobriety in geopolitics; fiscal policies; beyond monetary shell games; even in technical analysis where too many think they can proscribe the 'extent' of forward risk.

Enjoy the weekend and join us Monday !

Gene

Gene Inger

www.ingerletter.com