Extreme caution - approaching the market seems advisable; not just for risks of rate shifts (and the reality of semi-deflation or stagflation conditions in much of the world continued to sustain the bond market as we thought it would throughout the overall year; while risk of that ending is now soaring).

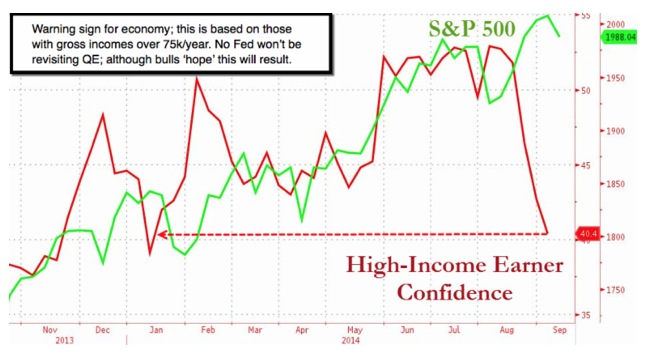

On a short-term basis; recent stability is not a function of the (Bloomberg) Comfort Index decline among higher incomes. It is more a structural result: a shift we noted to the December S&P from the September; which retained a substantial 'open interest'. This tended to create what I termed 'superficial support' for the S&P Thursday; as outlined intraday; and the expected (very good) trading day on Friday. Many noted everything 'but' open interest; as with over 2 million Sept. E-mini's yet to be unwound; it's not insignificant.

This is important because it suggests the market isn't 'really' healthy; plus it ignored some positives as well. If we're right; it was mostly such structural aspects as 'open interest' rolling (etc.) related to the upcoming next week's Quarterly Expiration; it suggests stability was a mere temporary reprieve.

Daily action - The main financial point was the idea of a breakdown of the global perception of a credit bull market persisting; as things can sort of falter, even if we continue to see global slowing.

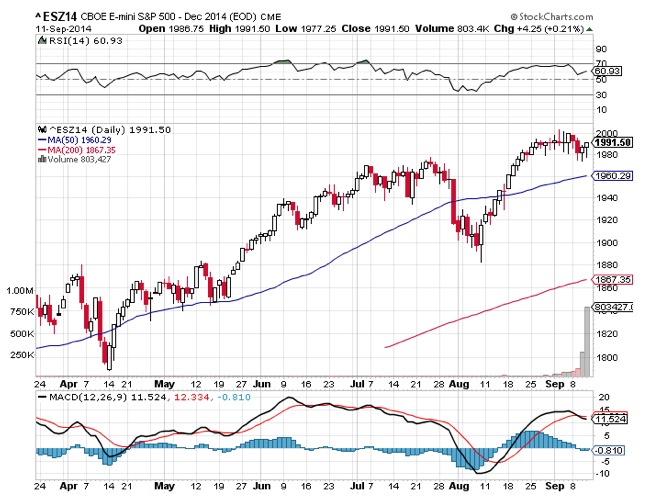

(Dec. S&P ideally formed a bit of a 'dome' and an A wave decline; a B wave rebound and now threatening to break into a 'C' wave delcline, as well as a breech of the 'standard deviation' mean. A break of last week's low might be delayed due to the FOMC or Expiration; but clearly algo's would trigger if it breaks noted levels before or after those events.)

Either way this remains a market in search of an accident; pure and simple. It has enough ammunition. It's failure to break really hard is a product not of all the 'confidence' that some analysts suggest; and not just the Fed either.

(We described the recent low in VIX as a secondary test of the base, and a build-up that followed as a short-term breakout, followed by some stability, and then odds favor higher levels as outlined daily.)

We persist short; adjusted to the December E-mini / S&P from 2002 or so.

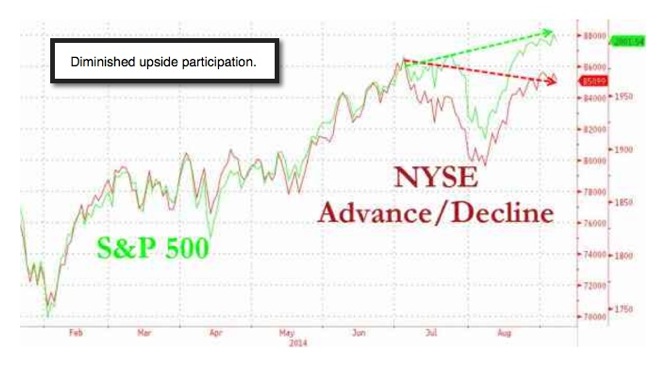

Lackluster momentum - and basically unimpressive breadth have been a hallmark of this market's otherwise-stoic tenacity of holding up; while many analysts try rationalizing a bullish case out of an overpriced market.

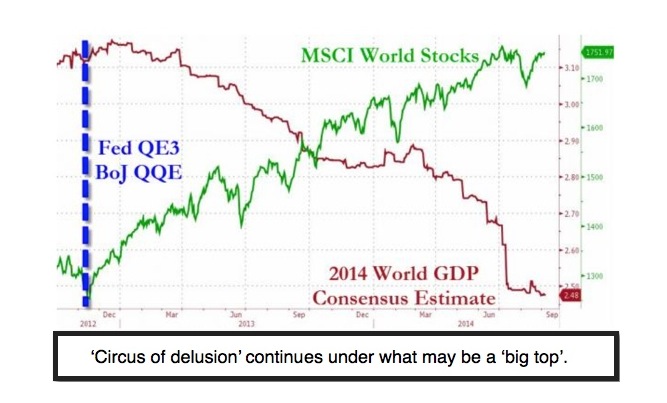

Financial engineering - is beginning to grope for ways to sustain not merely an aging uptrend, but distorted fundamentals.

But lets focus on the stock market; which 'the Street' comfortably feels must be completely controllable at this point. That's a dangerous fear to maintain.

Even more complacently; they believe markets can hold up regardless how much central bank money-printing or financial engineering remains viable. That distinction is more than a distraction.

The intrinsic nature of markets allow 'systems' some degree of success, but in this case only with the Fed wind at their back. That is diminishing so they expect growth & earnings to replace the Fed. Really?

Gene

Gene Inger

www.ingerletter.com