Is it really 'all-in' by Central Banks - as analysts persist saying; buttressed for sure by the PBOC rate cut overnight ahead of Friday's New York opening? Or is it, as a Chinese PBOC official said later in their day, not a valid sign of a program of liquidity injection. That makes a big difference on perspective. In either case there's little doubt but that stimulus, or the promise of such, is the 'drug' of choice for market players of this era. Some go to a point of extreme; suggesting that the central bank itself, is actually buying the S&P directly.

As we focus on 'technical analysis'; always remember to ask 'what' underlying or influencing factors, are contributing to moves increasingly away from often might be looked for: regression to the mean. What happens here is our topic.

(Discussion of the Dollar, ECB, China vs. Drahi's ECB; even Boeing and the bounce of triple lows in the wake of projected Dollar strength; all explored.)

Meanwhile, markets rise; contradictory as in many ways, to historically valid relationships between a strong Dollar and chaotic FX markets. Perhaps it's also worthwhile mentioning that currency isn't the only ignored factor here. You're got the High Yield and Credit Market indications that some very large investors and banks have taken note of (a few more remarks on this ahead).

Working against this includes 'seasonality' as this is a normally strong time of year. Working in unknown ways are the strife that 'may' arise from (redacted).

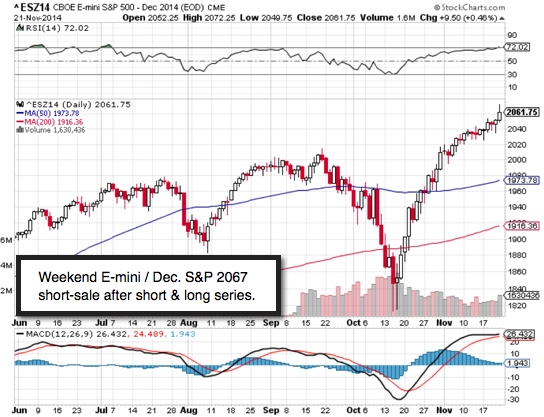

We are flexible toward intraday trading and have suggested several long-side guidelines during both these past weeks; but only for technically analyzed or intraday moves. Solely overnight retained efforts have been 'position-posture' shorts, typically with break-even mental stops to have some skin-in-the game especially (at certain points). By the way we were flat overnight Thursday; so that early run-up did not catch us. Friday's sole short-sale guideline at Dec. S&P 2067, is retained. For intraday traders, a nice gain was booked.

Investors should be skittish - when you see weak inflationary expectations such as the Fed desires; and as reflected by the commodities complex. Their downplaying of 'considerable time' on interest rate increases, is an emphasis by the Fed to focus on data-dependency. (More on this for our members.)

The Fed IS concerned about market volatility, as the report today implies. To adjust portfolios, managers will conclude they don't yet known when rates are going to be raised. BUT there is the global macro overhang, and emerging or other credit markets, which create angst (such as Japan and Asia mostly).

When markets get skittish. you get overreactions; we've seen it on the upside and most likely will on the downside; after what is an historic S&P rebound by the way. We've tried to 'think globally'; which is part of why it's curious to hear 'multiple expansion' arguments for higher prices. (Conclusion.),

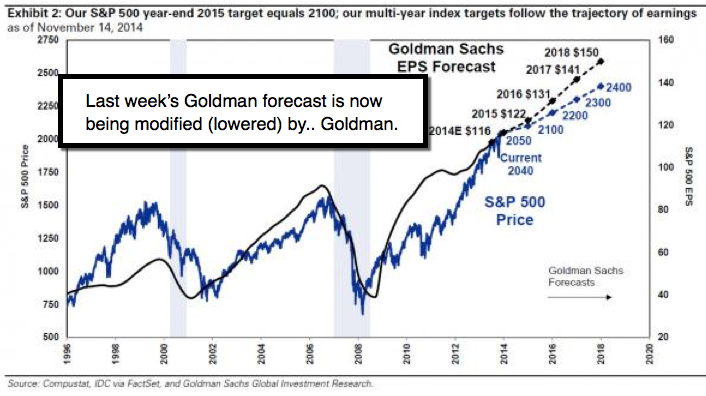

Lots of hard challenges progressively resolving in markets; but progress is a fleeting goal in global economics and geopolitics. Increasing awareness and sobriety has belatedly dawned on analysts. Investors already grasped the unsustainable financially-engineered moves; taking equity markets beyond delusional optimism; as stocks rebound to what now nears suspect levels.

Enjoy the weekend!

Gene

Gene Inger

www.ingerletter.com