Rationales & Targets

The rally from the October 15th low has been stunning for the rapidity of the advance, the complete reversal of volatility and the complete reversal of sentiment, which finally turned excessively pessimistic for the first time in 2014. However, the pessimism lasted for only five days, a ridiculously brief period of time for bears to be in control over an entire year. As we have claimed for many months, bears are nearly extinct at this juncture. We have now registered several record breaking circumstances for our own proprietary sentiment measures and for standard indicators, like the Rydex Ratio. As if we needed more about sentiment, newsletter writer bulls are back to 56.5% and bears have fallen to a mere 13.8%. The ratio of 4.09 is the third highest this year.

A few of the negative divergences we have previously illustrated look a bit better now but the appearance of new divergences, such as our combined cumulative breadth measure [previously shown], accentuate out belief that we are in a very late stage of the bull market. Finally, the broadening top we see in the Dow Industrials is deeply disturbing. Like 2000 and 2007 before, we have zero doubt that this is a veritable bubble and it will end as it has before. The Federal Reserve has done everything they can to accommodate bulls and in the process, have created a dependency that is akin to drug addiction. Bulls are convinced they will be bailed out of every bad decision and that nirvana always lies ahead. It does not

When Push Comes To Shove

Gold bullion is down 39.3% from the August 2011 peak of $1920 per ounce, certainly equivalent to the definition of a bear market by most, if not all standards, but these are unusual times. Economic growth through the last decade of the 20th century and thus far in the 21st century has been driven by a number of factors exclusive to our day and age, most importantly, the utilization of credit and debt. There have been vast increases from credit cards, consumer loans, mortgages, home equity credit lines, margin debt, student loans, and corporate debt. As well, there have been several quantitative assists by the Federal Reserve buying U.S. Treasuries to create money and ensure support for the economy. Like never before in our history, we are a society leveraged to the hilt.

In times like these, one must wonder about the viability of fiat currencies. If a society can always be bailed out of problems by simply printing more money and infinitely ramping up debt, then how can one value the currency of that society? Indeed, how can the currency have any validity? Creating more money must mean each unit of currency is worth less. Close to five decades ago, in a moment of perfect lucidity, former Fed Chairman Alan Greenspan wrote, “under the gold standard, a free banking system stands as the protector of an economy's stability and balanced growth... The abandonment of the gold standard made it possible for the welfare statists to use the banking system as a means to an unlimited expansion of credit... In the absence of the gold standard, there is no way to protect savings from confiscation through inflation.”

President Nixon ended the U.S. dollar’s link to the gold standard in August 1971 and over the next ten years, inflation averaged over 8.5% per year, up from an average of 3.1% during the previous decade. Americans could not keep pace with the rate of inflation and even stocks wound up well short of the inflation rate, rising roughly 0.5% per year plus about 4.6% in dividends. However, during the same period, the price of gold increased at an average of 26.5% per year.

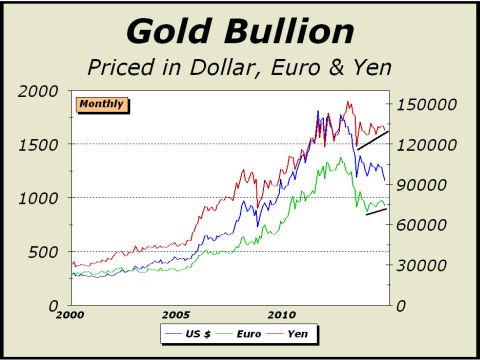

The world has known a strong dollar and accepted the dollar as the reserve currency for many years, a situation that has served us well. Anything other than the status quo brings up questions that cannot be answered, thus we seek to avoid any doubts and preserve the status quo. The Federal Reserve and the Treasury are happy to see gold in decline if only for the reason that it tends to makes the dollar a preferred asset. Meanwhile, there are other currencies and in terms of those currencies, the case is easily made that gold is only correcting the tremendous super bull move from 2001 to 2011. As our featured chart on page one illustrates, in Euro and Yen terms, gold has clearly held support. This is an additional buttress for our thesis of a super bull market. The decline of gold versus dollars does not automatically equate to the end of gold’s super bull market. Lest we forget, stocks suffered an equivalent collapse in only two months of 1987, followed by 11 annual gains in the next dozen years.

We believe gold’s super bull market remains intact. At lower left, the Dow/Gold ratio is 15 and should be on its way to eventually achieving our targets of 5.67 or 5 and we cannot rule out lower ratios either. The 5.67 ratio simply equates to the average ratio over the 20 year period from 1975-1994 and equates to bullion at $3144 per ounce. The 5-1 ratio that we pegged as realistic as far back as our super bull call of 2001 equates to $3565 per ounce. These targets rise with inflation. Given our assumption that inflation is understated, our targets could be considered conservative.

Alan M. Newman,

Editor, Crosscurrents

www.cross-currents.net