Leading into 2015, we choose to focus on the longer term trends currently in place, extrapolating them into the first quarters of next year. To illustrate this multi asset review, we will use FinGraphs Mosaic Views of Weekly charts (one point per week). They offer an investment perspective over the next few quarters.

We will first review equity markets globally. Then using US markets as a proxy, will focus on market internals and sector dynamic to try to identify where we may stand in terms of the business and market cycles. We will then turn to currencies and interest rates in light of the diverging monetary policies of Central Banks before focusing on Europe, Japan and China. Finally, we will consider the Commodities markets and Oil producing countries and finish off with other developing markets.

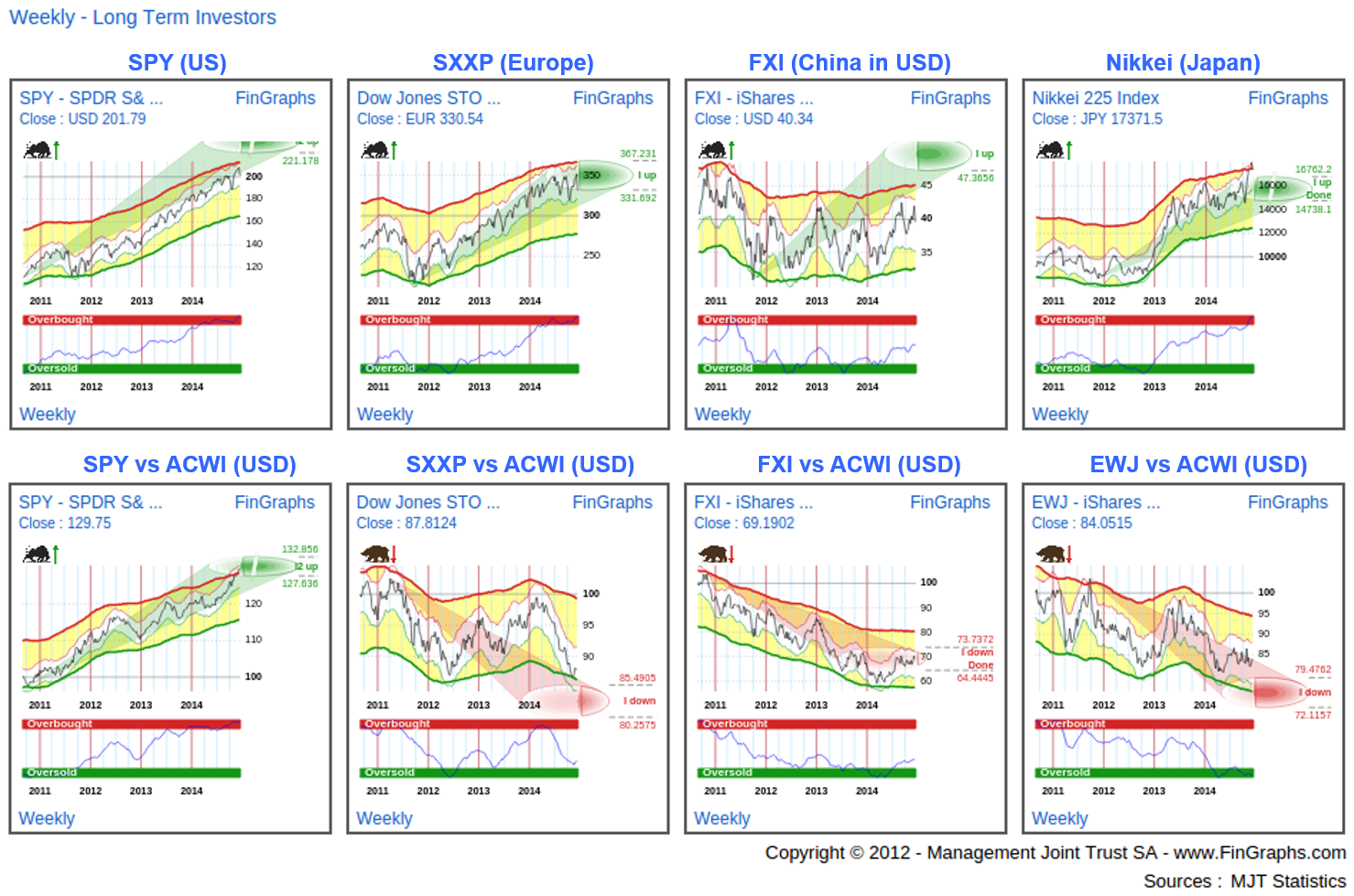

Global equity markets:

In the following Weekly Mosaic View, we lay out in the first line the world major markets on an absolute basis (US: SPY – SPDR S&P500 ETF Trust, Europe: Stoxx 600 Europe Index, China: iShares China Large-Cap ETF and Japan’s Nikkei 225). On the second line, we highlight these various markets vs ACWI in USD terms (the iShares MSCI ACWI Index Fund). We will use the same three indexes mentioned above for the US, Europe and China and the iShares MSCI Japan Index Fund (EWJ) for Japan.

On an absolute and local currency basis, all major equity markets have performed well in 2014. These trends are likely to continue in the first quarters of 2015. US markets have been the strongest performer both in absolute and relative terms. China is on par as it attempts to break out from a 3 year reversal pattern. On a relative basis and in USD terms, it is slowly turning up (Risk Index moving up above the Oversold zone, targets fulfilled “I down done”). Japanese Abenomics have had their positive effect on an absolute and local currency basis. The shake-out it initiates on domestic capital allocation still needs to prove it can add value from a USD perspective and in relative terms (still in a downtrend for now, although prices have stabilised and the Risk Index is Oversold). Europe is the weakest link. On an absolute basis, it has consolidated for most of 2014. Risk Index is Overbought and potential targets have been reached. Although much hope is set on promises of Qantitative Easing next year, on a relative basis, the trend still follows EUR/USD down with more downside potential remaining. Hence in USD terms, we would continue to favour the US and China vs Europe and Japan.

Current position in the business and market cycles:

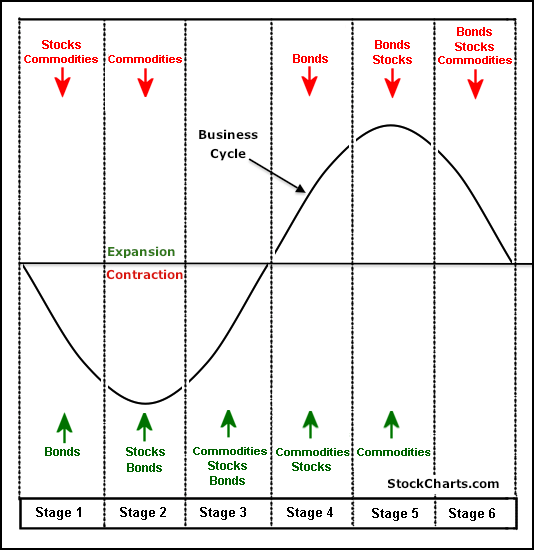

Whenever we try to position ourselves in the business cycle, the Pring Turner 6 stage business cycle is always a good guide (Martin Pring is one of the reference contributors on StockCharts.com and author of several books considered as part of the foundation of modern technical analysis). It separates the business cycle into 6 distinct stages and highlights the performances of Bonds, Stocks and Commodities in each one of these. The business cycle is considered to be 4 to 5 years long so that each stage last approximately 3 quarters.

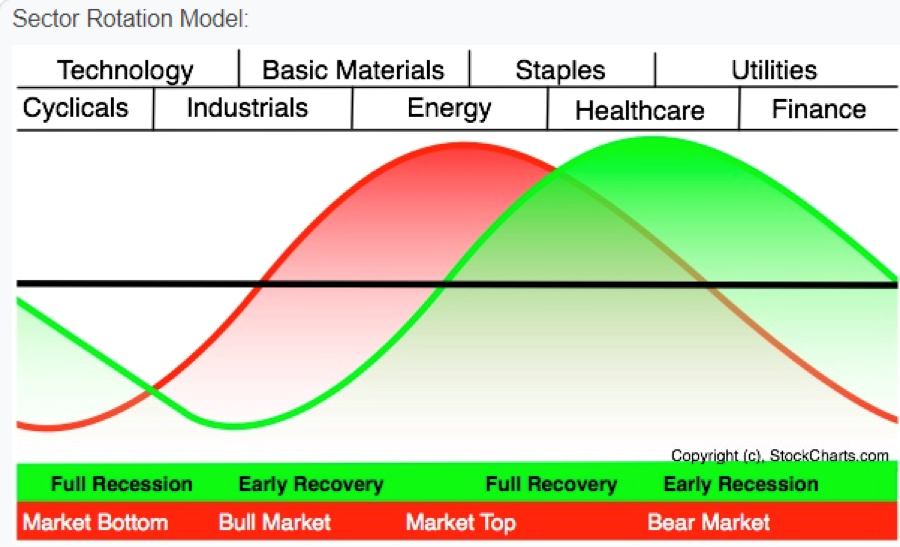

To complete the business cycle, we also consider the Sam Stovall’s sector rotation model (Mr Stovall is Managing Director at S&P’s Capital IQ and Chairman of S&P’s Investment Policy Committee). It highlights how market cycles tends to lead the business cycle (“they anticipate”) by 9 to 12 months (or one to two stages in the Martin Pring Model) and how the different equity sectors rotate during this process.

One would notice that the stock market starts turning up while the economy is still in Full Recession and accelerates on early signs of Economic Recovery. Similarly, the stock markets tends to top while the economy is still in Full recovery and accelerates down on Early signs of Recession. In an Upturn, the first sectors to react up are usually Cyclicals, Technology and then Industrials. As growth and inflation accelerate, Basic Materials and Energy lead up to a market top. As the markets starts to correct, Defensive sectors (Staples, Healthcare and Utilities) outperform. Financials finish off the cycle as they show resilience through the downturn and in the early stages of the new cycle (2008 would be an exception as the Lehman crisis rocked the financial system).

We will use these two cyclical models and the recent market performance of sectors and asset classes to try to identify where we currently stand in the business and market cycles. We will then attempt to confirm this position by considering FinGraphs Weekly charts.

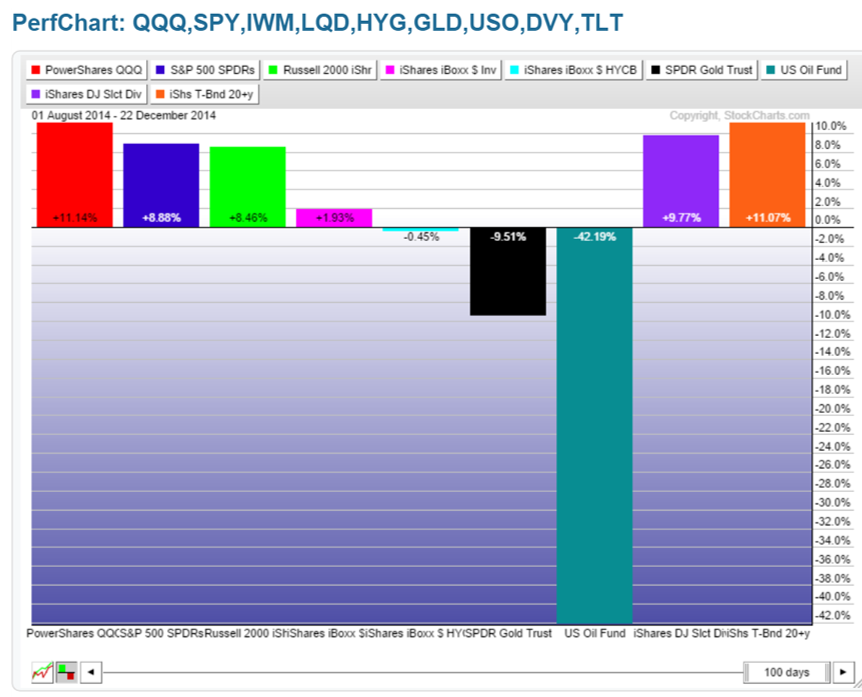

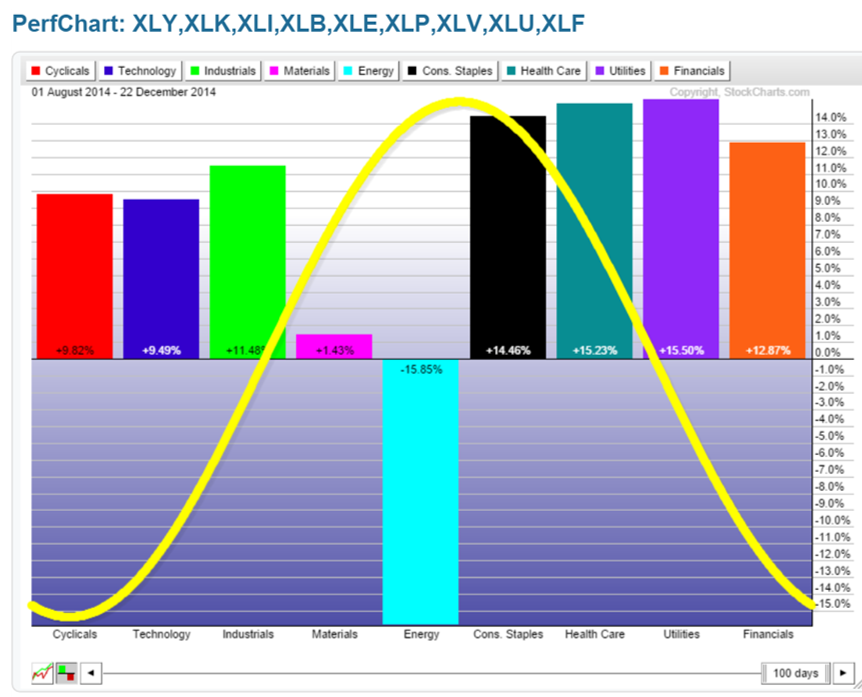

In the chart below, we lay-out the performance of the main US asset classes using StockCharts.com’s built in PerfChart functionality. We have chosen to feature this performance over a relatively short period, i.e. the last 100 days (or circa half of the 3 quarters average Business cycle Stage length) to take the latest developments into accounts.

We have ordered these asset classes in what we believe could be the sequence of performance along the cycle. With the tech heavy NASDAQ QQQ taking the lead, followed by the more balanced S&P500 and then small & mid caps, corporate bonds and high yield as growth expectations are confirmed and credit spreads contract. Inflation sensitive Gold and Oil then accelerate until the market tops. High dividend stocks and then Government Bonds close-off the cycle as investor focus on income and finally safety.

The first thing that stands out on this performance chart is the significant underperformance of commodities (SPDR Gold Trust [in black] and the US Oil Fund [in greenish blue]). When reverting to Mr Pring six stages model, this should not be possible in Stages 3, 4 and 5 of the business cycle or if we consider that the market anticipates by 9 to 12 months, the run-up to the top and the early correction periods in the market cycle. Positive equity performance across the board as well as strength in Treasuries could also exclude Stage 6 (where all three asset classes fall in synch) unless accommodative Central Bank policy around the world have succeeded in massaging this Stage 6 out. So considering the above, we would be left with, possible Business cycle Stages 1, 2 or perhaps 6.

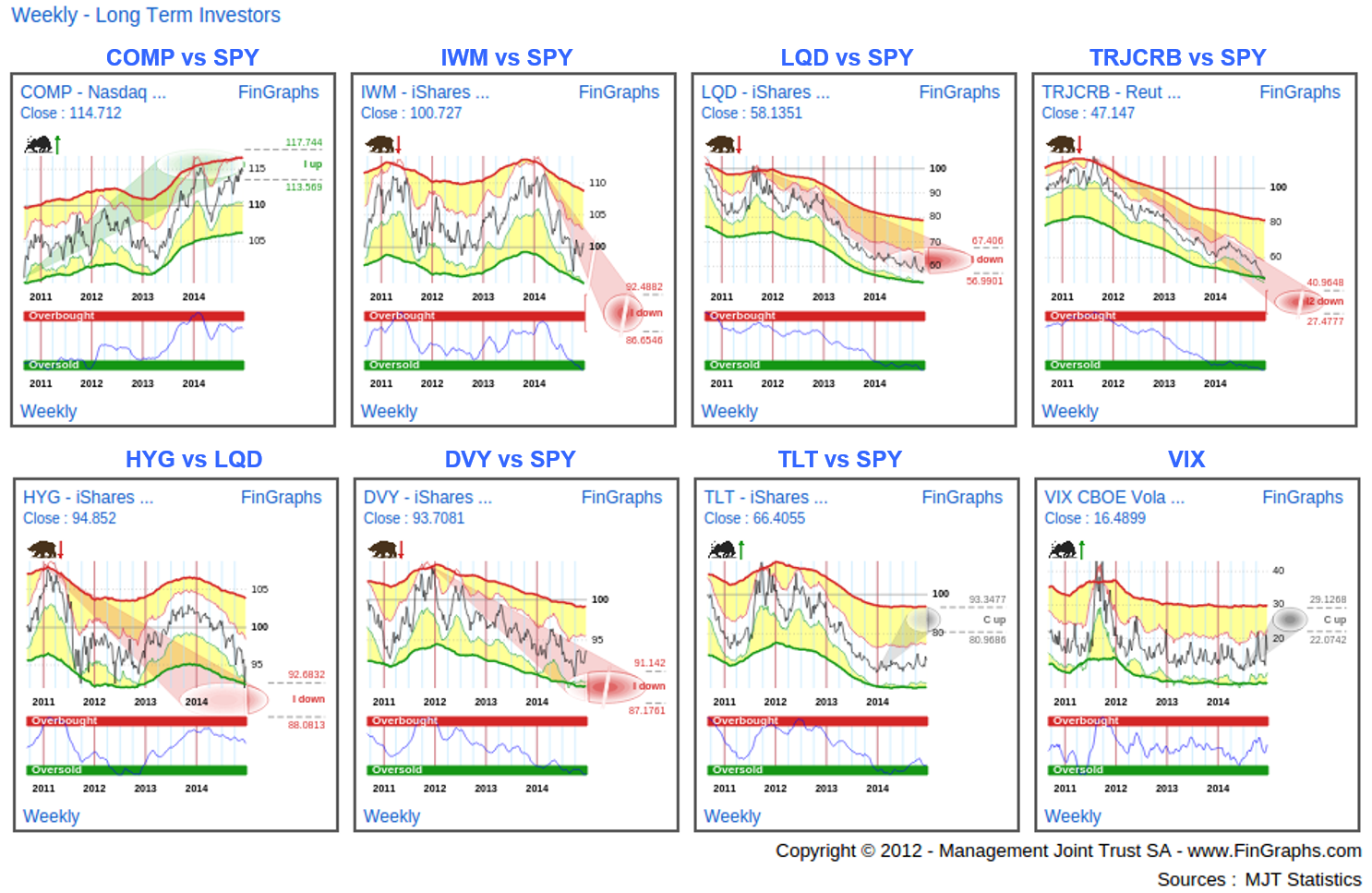

Let’s consider the market internals in the US with the following Mosaic View:

Most of these charts are quite defensive. Starting from the end of this Mosaic View, we notice that TLT (iShares Barclays 20+ Yr Treasury Bonds ETF) has been correcting up vs the SPY for the last 12 months. Such action would be typical of later stage Bear markets and early Bull trends (Stage 6 and 1 in the Pring business cycle model). This would be confirmed by the VIX which over the last 6 months has been attempting to break higher. Other market internals such as small & mid caps IWM (iShares Russell 2000 ETF) vs SPY, investment grade corporate bonds LQD (iShares iBoxx $ Investment Grade Corporate Bond ETF) vs SPY, a widening of credit spreads (HYG - iShares iBoxx $ High Yield Corporate Bond ETF vs LQD) or DVY (iShares Select Dividend ETF) which although volatile has performed on par with SPY, would also highlight this flight to quality. Finally, Stage 6 or 1 would justify, the bloodbath in the Reuters Commodity Futures Index (TRJCRB) vs SPY. What may come as a surprise is the strong relative performance of the tech heavy Nasdaq composite (COMP vs SPY) over the last 6 quarters. Its relative trend is still heading up, its Risk Index is not yet Overbought. It may lead us out of this downturn sooner than the other internals would suggest.

To gain more insight, we will now focus on the performance of main US equity sectors. We have overlaid the ideal market cycle (not the business cycle which is 9 to 12 months behind) to identify which sectors should outperform at different stages in this cycle. Again, we have used a 100 days performance as a reference.

The performance is heavily skewed towards the back end of the chart or what is possibly Stages 5 and 6 of the business cycle. Utilities is the strongest performer, a typical stage 6 phenomenon usually corresponding to a late Bear market in the market cycle. As mentioned above, these performance charts are based on the last 100 days. We will now turn to the future and consider FinGraphs Weekly Mosaic Views in order to gain market perspective over the next few quarters. We have classified these sectors into three main categories: “late Bears / early Bulls”, “confirmed Bulls” and “late Bulls / early Bears”.

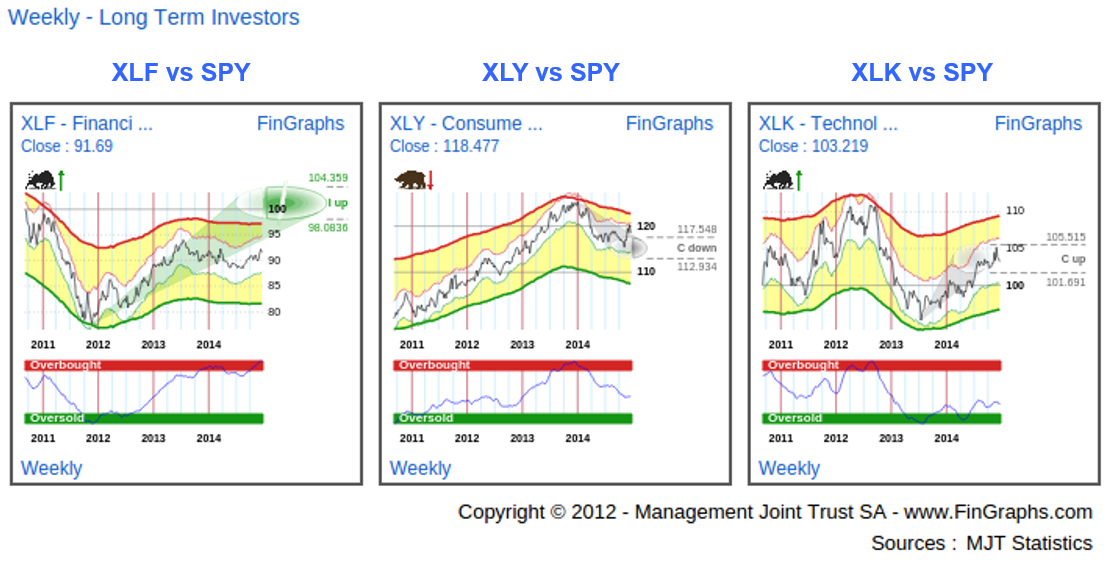

Late Bear / early Bull sectors (outperformers in Stages 1 and 2 of the business cycle):

XLF (Financials), XLY (Consumer Discretionary), XLK (Tech)

Strong potential up for the Financials (Impulsive Up “I up” on XLF vs SPY), a mild consolidation for Consumer Discretionary (Corrective Down “C down” on XLY vs SPY) and close to breaking above corrective targets into impulsive mode for Techs (Corrective Up “C up” on XLK vs SPY): positive perspective vs SPY for these bottoming Bears and early stage Bulls.

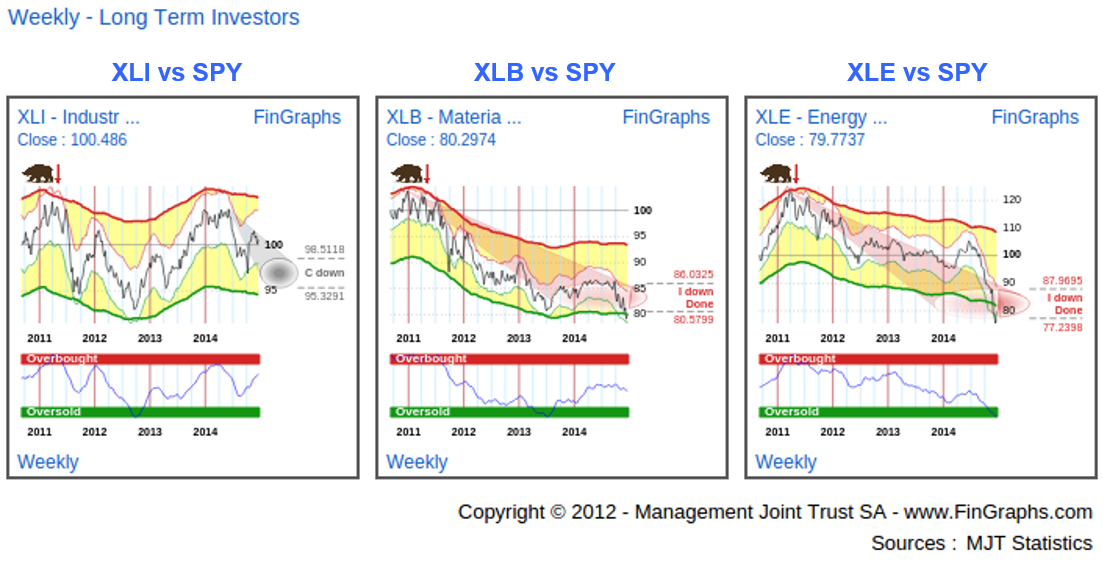

Confirmed Bull sectors (outperformers in Stage 3 and 4 of the business cycle):

XLP (Industrials), XLB (Materials), XLE (Energy)

Although Industrials are only in a correction down, the sell-off in the third quarter 2014 was quite strong (Correction down “C down” on XLI vs SPY for now). Materials and Energy although within their impulsive targets down (“I down done” on XLB and XLE vs SPY) are still in impulsive Bears: a reversal of fate on XLB and XLE is not awaited in the near future although XLI may manage to resume its uptrend over the next quarters.

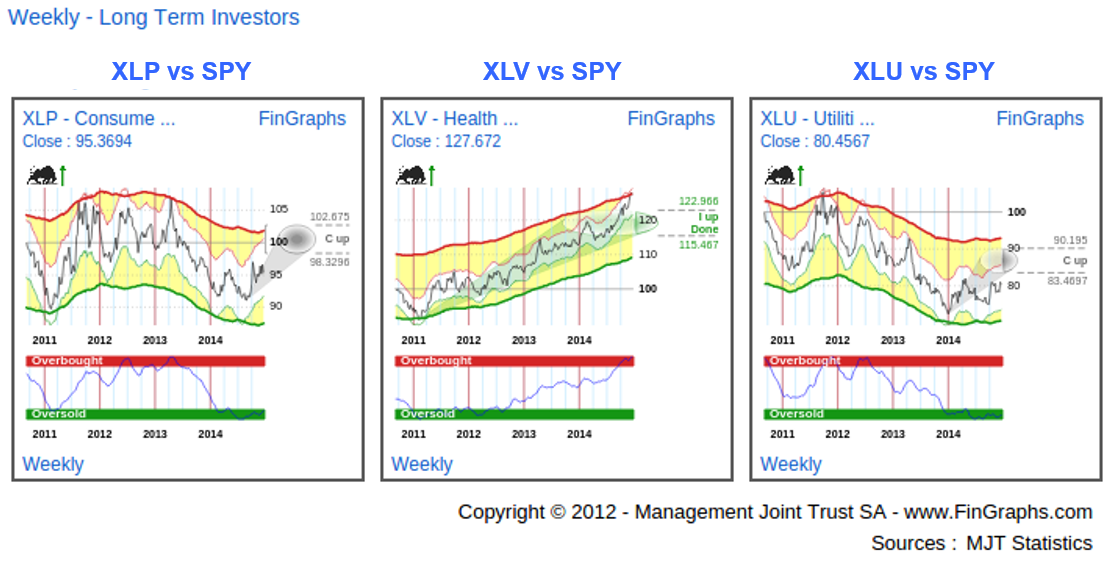

Late Bulls / early Bears (Stages 5 and 6 of the business cycle)

These defensive sectors have been the strongest performers over the last 100 days. Although their Risk Indexes are well Oversold, XLP and XLU are still in the early stages of corrections up for now vs SPY (“C up”), they could still resume their downtrend. We believe the fate of the market over the next few quarters will depend on the shift in relative performance from these defensive sectors to the early stage Bulls (XLF, XLY, XLK). We would want to give the market the benefit of the doubt on this. We would hence tend to identify our current position as being Stage 1 or in early Stage 2 of the business cycle. Indeed, Stage 2 is the only one where Bonds and Equities rise and Commodities fall. It also matches what the FED is leading us to believe as it projects growth to accelerate and intends to raise rates in 2015.

Note: we have not discussed XLV (Healthcare) vs SPY in this last paragraph as we believe it may capture the best of both worlds. It benefits from a supporting secular trend (an Aging population), is considered defensive, but is heavily tilted toward biotechnology, a innovative industry which should benefit from an early stage Bull market.

Currencies:

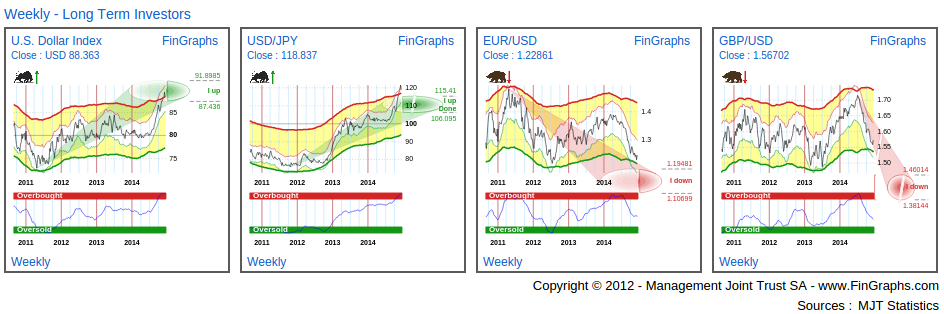

Considering that the economy and the market may be in the early stages of a recovery could appear as a bold statement, especially when many equity markets are hitting all-time highs. However, one thing that can be said about quantitative easing is that it has succeeded in sustaining asset inflation throughout the cycle. When we consider the period of low growth between 2011 and 2013 across all developed economies, the negative impact on equity markets (and the US markets especially) has been very limited. In fact, markets have “climbed a wall of worry”. Now, that US GDP is growing again at 5% yoy (i.e. the recently released 3Q revised GDP figures), could the markets be ready to re-accelerate? The answer is probably not as clear-cut. Indeed, the US is only one of three large trading blocks and markets are still struggling with the growth story in the other two. Europe and Japan are battling deep structural problems, the first is growing at circa 1%, the second is still in outright recession. In China, growth is also decelerating and is coming dangerously close to the 7% - 7.5% minimum target. To different degrees each one of these, is applying its own version of monetary easing (repeated rate cuts during 2014, TLTROs and the prospects for outright Quantitative Easing early next year in Europe, Abenomics in Japan, measured rate cuts combined with an opening of its capital markets in China). What this highlights is that the US, as it leaves Quantitative Easing 3 behind and intends to raise rates in 2015, is clearly ahead of the curve. This is having a huge impact on the FX markets and Dollar strength should continue in the first quarters of 2015. Indeed, all trends on FinGraphs Weekly charts are still positioned in favour of the Dollar.

In terms of price target potential, there are several percentage points left on the Dollar Index (DXY) until impulsive targets are met. USDJPY has already reached its impulsive targets (“I up done”), but it is hard to believe that it will not go into Impulsive 2 mode: Impulsive 2 targets would imply a range between 130 and 140. EURUSD is heading lower possibly into our projected 1.19 - 1.11 Impulsive target zone over the next few quarters. Cable has just moved through corrective targets and is now pointing to below 1.50.

Interest rates:

Again, these rapid currency moves are the resultant of the current discrepancy in Central Bank policies. Indeed, the rest of the world seems to be at a different stage in the economic recovery that the US. As we analysed above, based on the sector rotation as well as market internals, it would appear that the US is well within Stage 2 of an economic recovery. The rest of the world is probably still stuck in Stage 1, a period of restructuring and pro-cyclical intervention. This is where we believe an important risk lies in 2015 as there are no guarantees that the monetary and structural programs put in place in Europe, Japan, the UK, China or elsewhere will meet the same cyclical success as the ones coming to completion in the US. Other risks, we also highlight for 2015 are 1. the instability caused by the drop in oil prices in oil exporting countries as well as 2. the possible impact of USD deleveraging in emerging markets where some countries have large exposures to USD denominated debt (will only get worse with a rising USD).

We believe these underlying uncertainties are somewhat reflected today in the trends of interest rates and the yield curve. In the Mosaic View below, we have displayed the 2 Years and 10 Years Interest Rates Swap rates for the US and Europe:

In the US, the 2Y swap rate is in an impulsive uptrend with more potential up over the next few quarters. This reflects the end of Quantitative Easing 3 and the perspective of rising rates in 2015. The 10Y US swap rate however is in decline and showing significant downside potential. It mirrors doubts over the improving economy (US or Global?) and tamed inflation expectations (as a matter of fact inflation data has been weak recently, especially on the back of dropping oil prices). The result is a flattening yield curve, a phenomenon which often precedes a period of recession. In financial markets, “Perception is reality” and there really needs to be a shift in this perception over the next few quarters to validate the growth story: US inflation expectations must rise and economic attractiveness abroad must improve so that bond selling moves out the curve to the longer maturities.

In Europe, by contrast, the expectations are focused on quantitative easing. Hence, both short and long term rates are trending down and should continue to do so in the first quarters of 2015.

Let’s now turn to international markets (non US), commodities, oil exporters and other emerging markets or what we believe are areas of potential risk in 2015.

European markets:

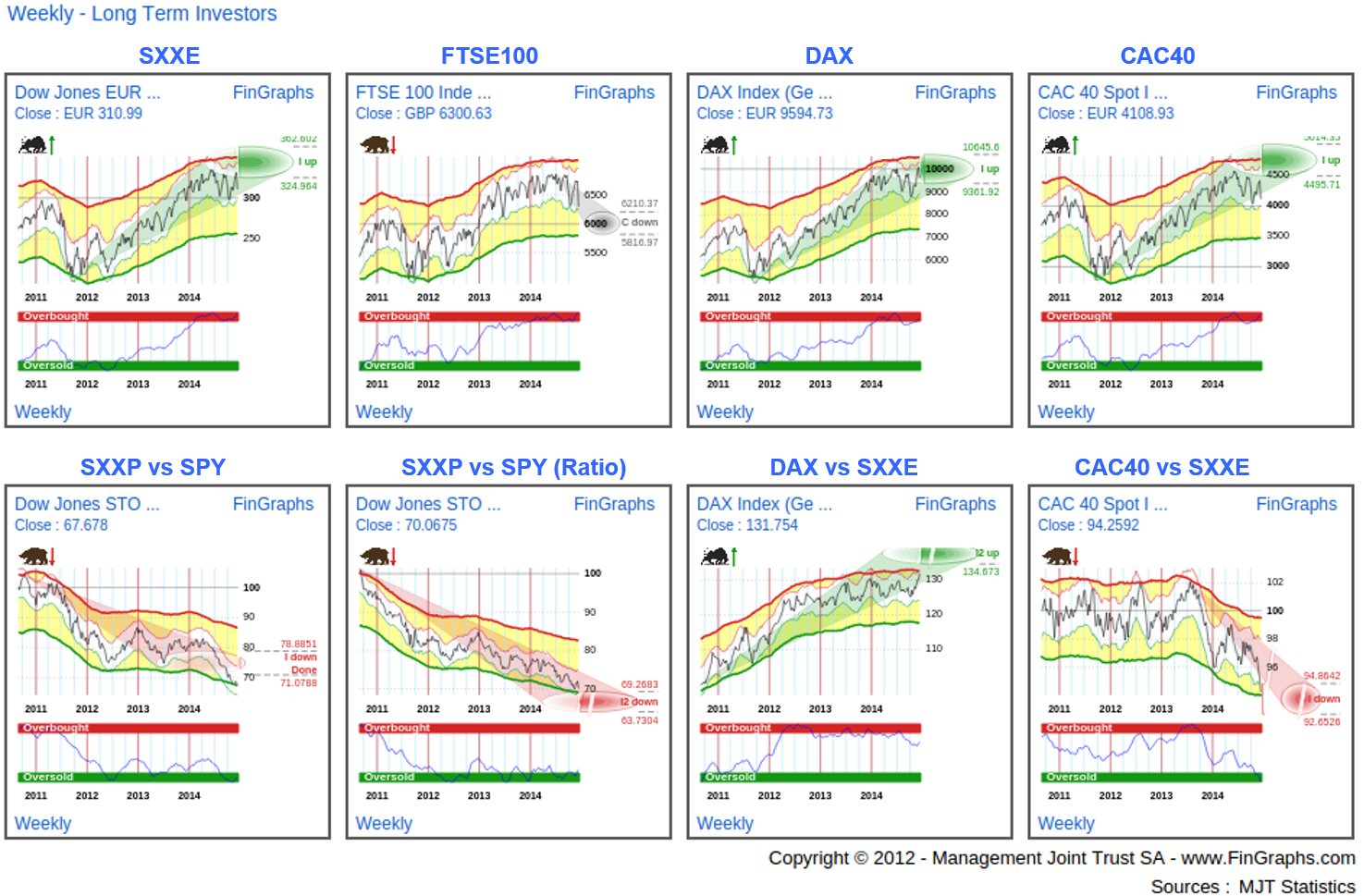

On this Weekly Mosaic View, we have displayed major European markets in the 1st line (SXXE: EuroStoxx 600, FTSE100, DAX and CAC40) and several relative charts in the 2nd line.

Although most trends are still heading up on a Weekly absolute basis, the secondary correction that affected these markets in 2015 is still underway. The DAX is the only one to have made new highs this last quarter and for the other three, the recent December sell-off has been very damaging (for the FTSE100 especially, which is now in a correction down mode). On a relative basis, the European Stoxx 600 Index (SXXP) is still underperforming vs the SPY both on a non-hedged (relative chart) and hedged basis (ratio chart). These trends although extended are still negative over the next few quarters. Internally, in the Eurozone, the DAX is showing strong momentum vs SXXE (EuroStoxx600), while the CAC40 is hit by renewed underperformance, which should extend into 2015. To a lesser extent, this is also the case (not shown here) of Italy (Eurozone’s 3rd largest economy) and most recently Spain (Eurozone’s 4th), which have both started to underperform again over the last 2 quarters.

Japan and China:

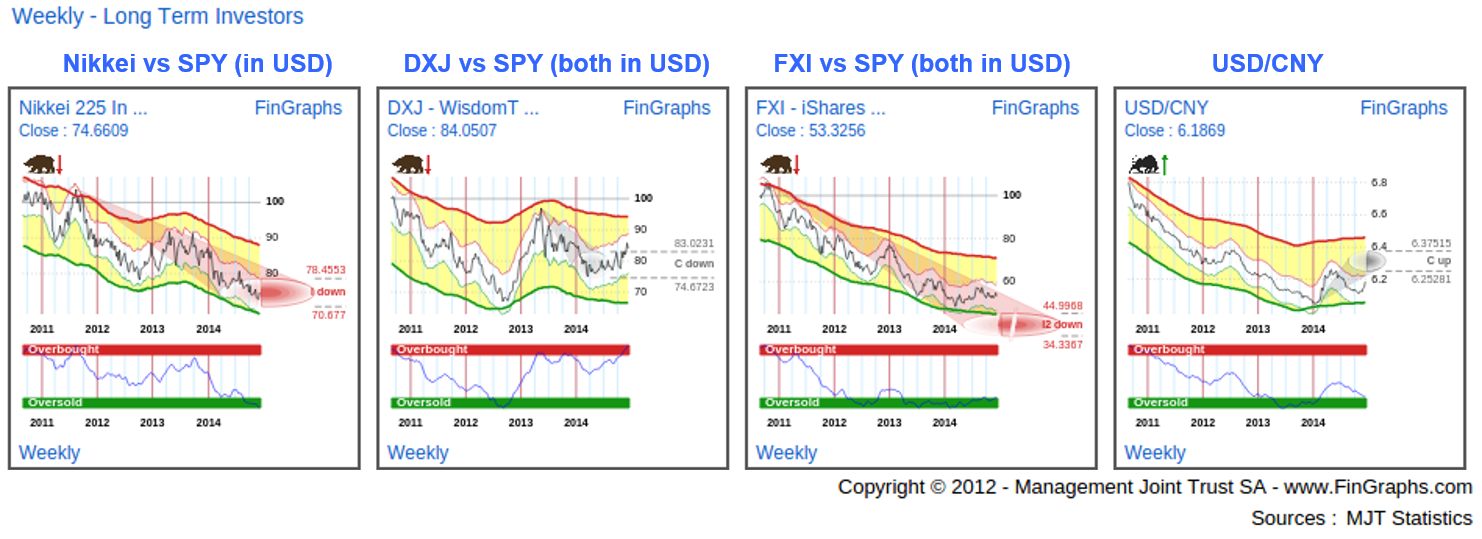

The following Mosaic View displays the relative charts of the Japanese market both on an un-hedged (Nikkei 225) and hedged (the investable DXJ ETF) as well as China vs SPY and Chinese Yuan vs USD.

On a relative basis, the Nikkei did attempt to move up vs the SPY in the first half of 2014. Lately, however, it has started to underperform again mostly on the back of an acceleration in Abenomics and the related YEN weakness. This trend is likely to continue in 2015. Even on a hedged basis, as shown here with the relative chart of the WisdomTree Japan Hedged Equity Fund (DXJ) vs the SPY, the trend is still negative: although prices have corrected up during most of the year, the Risk Index was quick to move back in the red Overbought zone. Abenomics is an aggressive attempt to reflate as well as shake-out Japanese traditional risk averse investment habits (get domestic investors out of Japanese Government bonds and into Japanese Equities), the large scale of the program does however make it a dangerous experiment and may run the whole country into bankruptcy.

On the other hand, China’s FXI ETF has turned up in 2014 vs SPY. Although, cyclical problems in China have accumulated over the last 24 months (growth targets in jeopardy, inflation coming down, bad debt exploding), we believe the People Bank of China is sending the right signals through measured interest rates cuts and programs to open Chinese equity markets as well as internationalize its official currency, the Renminbi. We believe that although the trend on the FXI vs SPY is still negative, the Risk Index, which is very Oversold and turning up, could help confirm a reversal of trend in 2015. We do not see large risks of devaluation in 2015 (USD vs CNY is in a mere Correction up) as it would very counterproductive to Chinese efforts to rebalance their economy from exports and investments to consumers and services (for more, read of recent TAC contribution on China: http://stockcharts.com/articles/tac/2014/12/fingraphs-china--skyrocketing-and-could-continue.html).

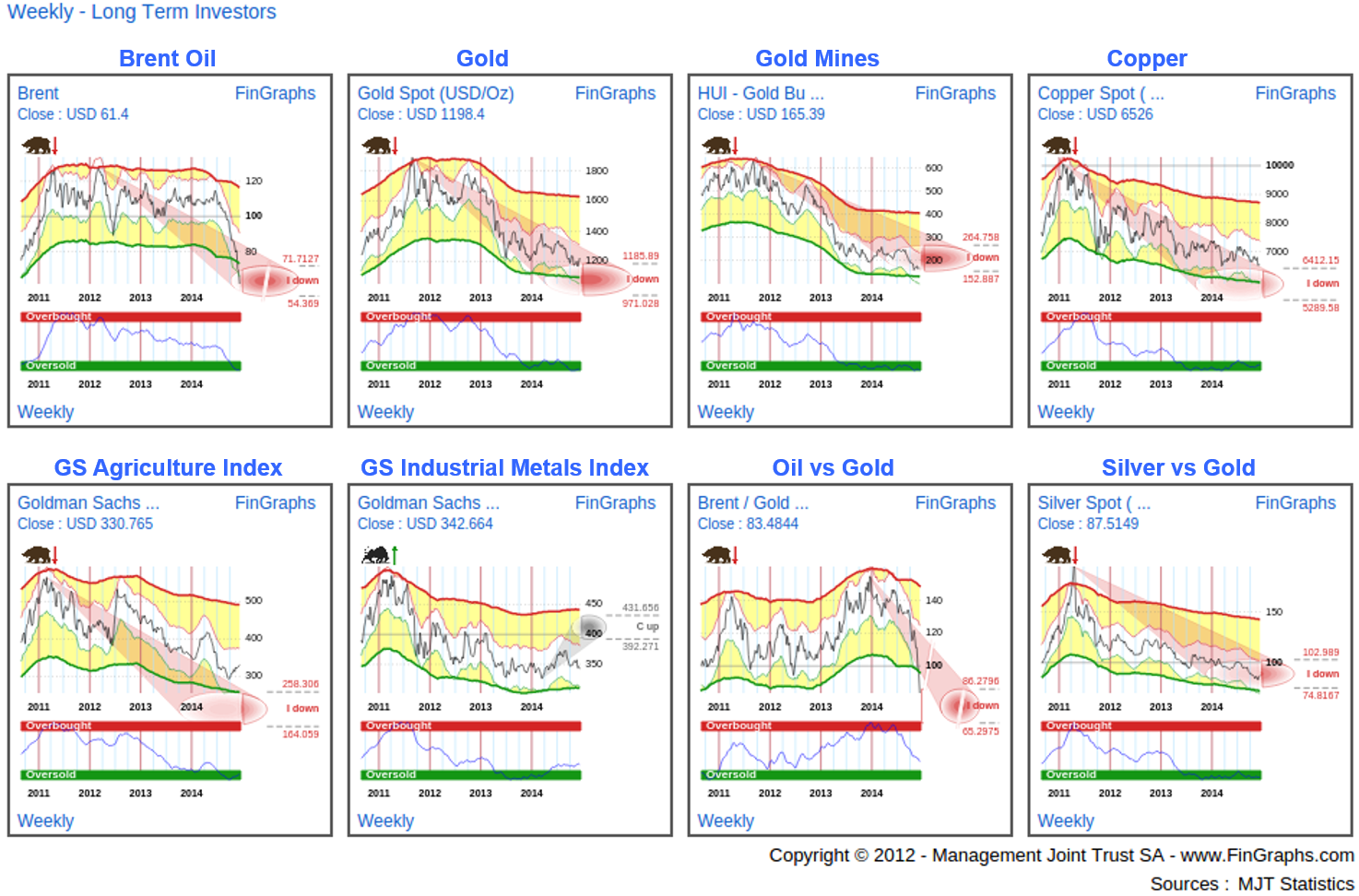

Commodities:

2014 has been a hard year for commodities. Although well underway, these negative trends sill show some downside potential across the board in 2015.

Oil has exited a large distribution pattern in a historical breakdown to lower levels. This impulsive trend is still underway and shows more downside potential over the next few quarters. Gold (and Gold Mines), although quite Oversold, is still heading lower possibly into low 1’000 price levels. In the absence of an outright financial crisis (flight to quality) and on the back of low inflation expectations and rising financing costs (flattening on the US yield curve), we believe that for now there is little potential for a significant rebound. Copper and Agricultural commodities are also still heading lower and although Industrial metals have corrected up in 2014, this correction is still weak and could easily resume its downtrend. Relative charts of Oil vs GOLD and Silver vs Gold are still counter cyclical and mirror risk averseness rather than a pick in inflation sensitive assets (such a pick-up would normally set the stage for Stage 3 of the Business cycle, we are not quite there yet for now).

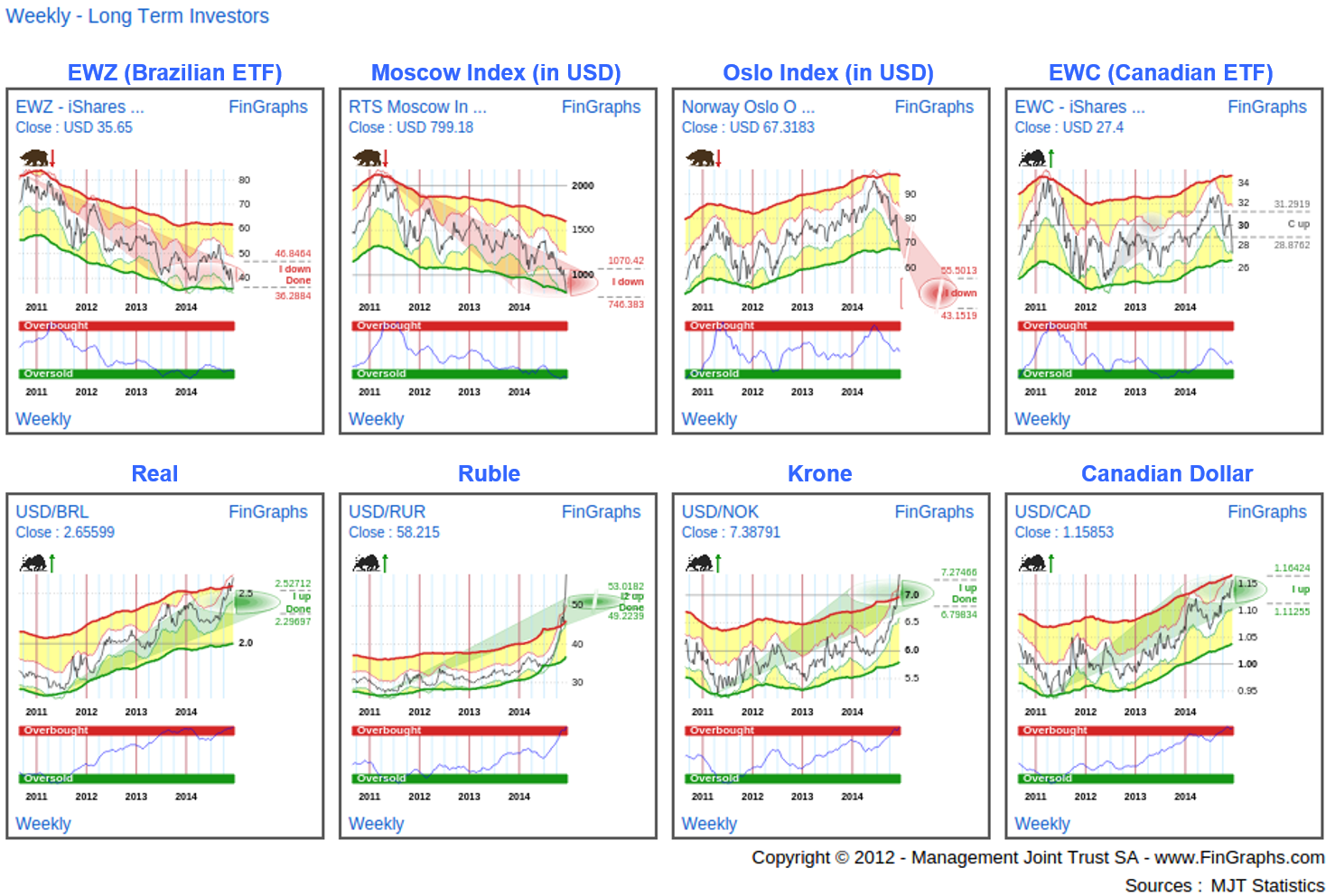

Oil producing countries:

On the back of the Oil sell-off, Oil exporting countries are hit hard. The following Mosaic view displays several examples, with the respective equity markets in the 1st line and the USD exchange rates in the second.

Developing markets such as Brazil and Russia have been hit especially hard, but developed Norway and Canada are not immune. These trends are likely to continue into the year as oil continues its descending Weekly trend. We would avoid bottom fishing this exposure in the new year. Please see again our related recent TAC contribution on the subject (http://stockcharts.com/articles/tac/2014/11/fingraphs-cheaper-oil--possible-winners-and-losers.html).

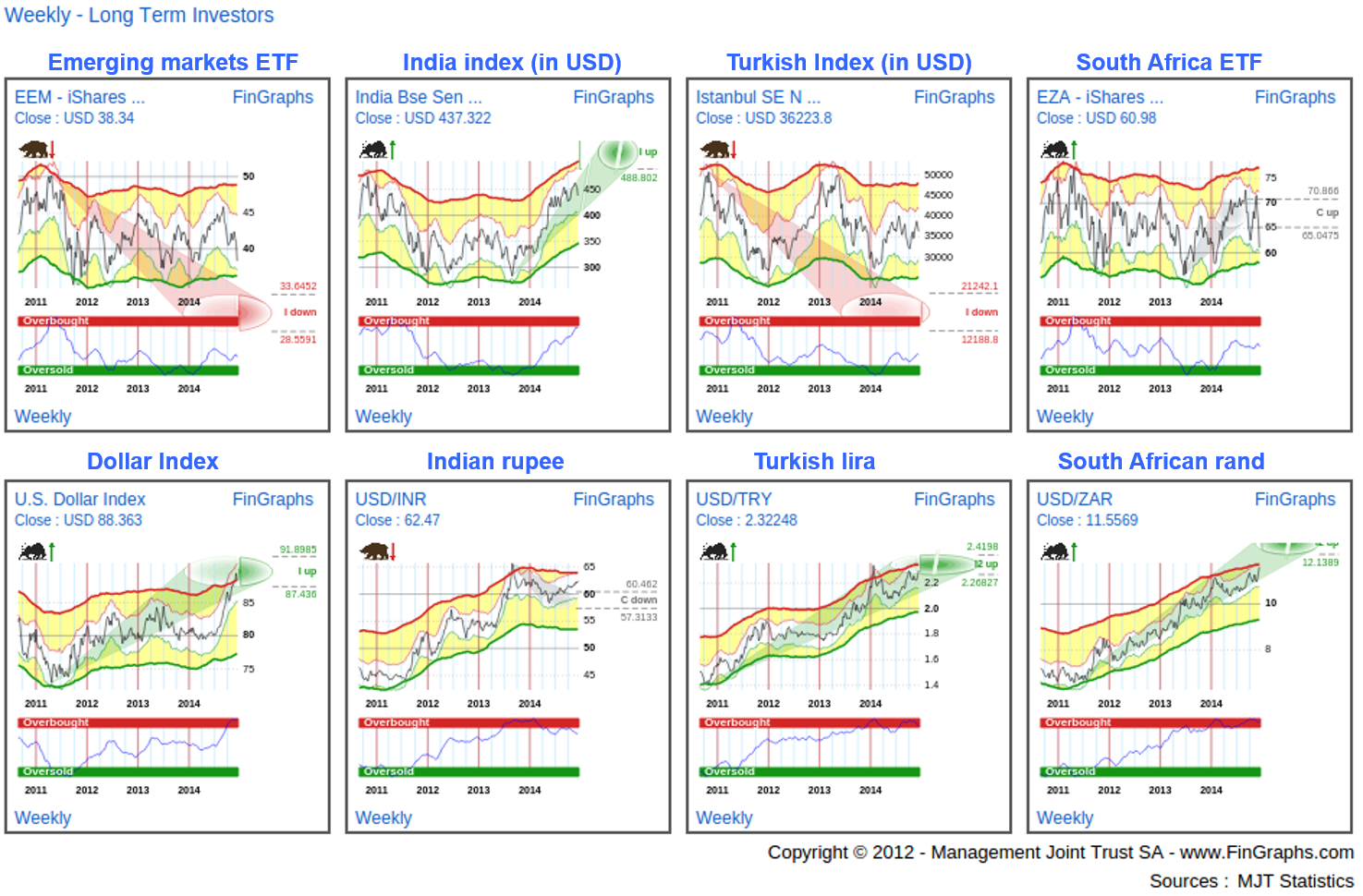

Other Emerging Markets:

Other emerging markets (especially the net Oil importers), should benefit for the drop in oil prices. That said, they are also heavily exposed to a slowdown of their exports markets (devaluation pressure from Europe and Japan as well as a slow-down/recession in growth in China, Europe and Japan). In many countries, this is often accompanied by a large exposure to USD denominated debt obligations. As the USD continues to rise, the cost of carrying and reimbursing USD denominated increases. This incidentally creates a deleveraging and credit tightening cycle in these local markets and negatively feeds back to generate further Dollar strength.

As you can notice from these examples, the larger the currency depreciation against the Dollar, the more significant the absolute under-performance in USD terms (please see our related recent TAC contribution for more insight: http://stockcharts.com/articles/tac/2014/12/fingraphs-usd-deleveraging-in-emerging-markets-a-significant-risk-in-2015.html).

Wrap-up:

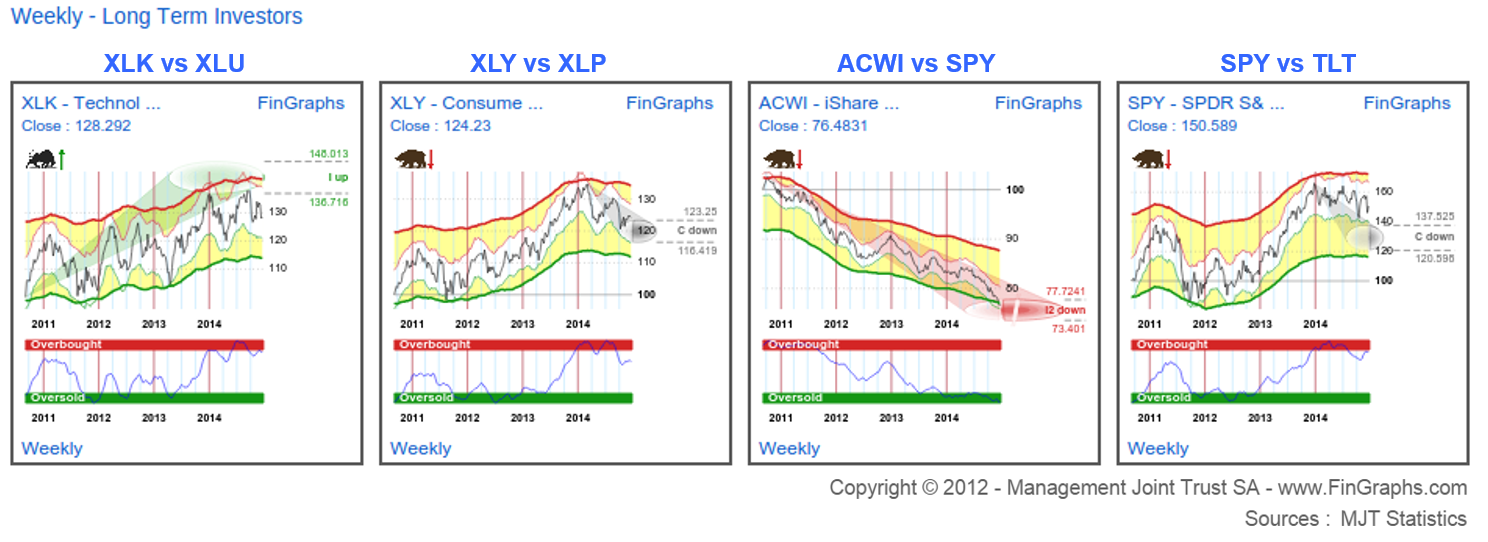

US Quantitative Easing Programs may have finally succeeded in creating the conditions for a cyclical upturn in the US GDP data. However, these positive developments come from a very high basis in financial asset prices and are threatened by sluggish growth and structural challenges in other international markets. We will give the benefit of the doubt to the current rising equity market trends in the new year (especially in the US and China), but will monitor the situation closely. Below as several examples of what we will be looking at:

• XLK (Techs) vs XLU (Utilities) and XLY (Cons. Discretionary) vs XLP (Consumer Staples): these relative US sector charts compare defensive sectors with early movers in the cycle. XLK and XLY have been correcting vs XLY and XLP in recent quarters. We would really need to see them reinstate their uptrends and move forward to confirm that a positive growth scenario is sustainable

• ACWI vs SPY: in order to comfort the rising trend in US economic growth and markets, we would want to see some pick-up in the relative performance of other international markets vs the US in 2015 (we need other success stories apart from the US)

• SPY vs TLT: growth won’t be sustainable if confidence doesn’t pick up. The current strength of long dated Treasuries highlights this uncertainty. SPY has started to correct down vs TLT. It could jeopardize this whole recovery if it were to accelerate down.

As a last caveat, we would stress than not all 4 to 5 years economic cycles share the same strength. Some show 3 to 4 years up and 1 sideways year (tilted to the right hand side), others may prove to be much weaker (tilted to the left hand side). There are a lot of structural issues still outstanding (internationally, but also in the US) and they could come back to haunt us if the cycle uptrend was especially short-lived.

For more information on our methodology click here (http://www.fingraphs.com/#couponid-STKCHARTS14) and then visit ‘About Us/Press release’ and ‘User Guide’ sections of our website. Clicking that link also qualifies you for a 7 day demo and a 10% discount on our services if you choose to subscribe.

We wish you a good start to 2015 and all the best for the year. We will be back in the second week of January.

Have a great weekend, J-F Owczarczak (@fingraphs)