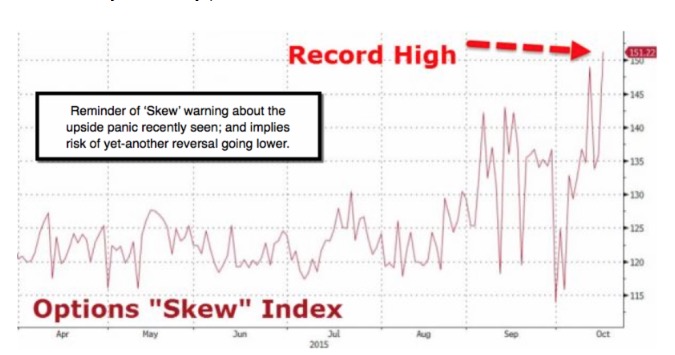

A returning 'spell' of illiquidity - was thought on-tap to bode poorly for S&P and broad market behavior; without bears being spooked until Halloween. One of the main problems is that nothing has been done to deleverage debt levels, which generally have not been unwound, but increased by monetary policies.

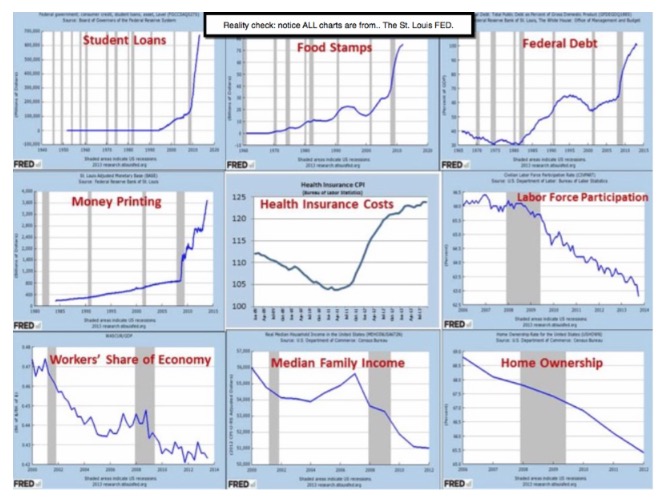

At this point, nearly 90% of the developed world is dealing with interest rates at zero; a couple just 'below zero'. Almost half of all bonds in the world actually are now paying less than 1%. The end result: there's no real incentive to save money by the public, and it's part of why companies have leveraged buybacks, without consideration that this hobbles their business (because funds aren't at all being used for expansion), while creating debt for shareholders, typically all unaware it's like being on indirect margin; while they think it's a plus (of course to artificially embellish earnings by virtue of a lower floating share supply).

On the contrary to being useful as politically-sensitive central bankers proclaim regularly; these low interest rates entice people and corporations to borrow, in many cases more than they should. It's also contributed to (for members).

Thus, even though too much bad debt triggered our 2008 'Epic Debacle' calls, in 2007; the ongoing mountain of debt has not been (net) reduced, but rather increased. Thus on a balance sheet, there has been no deleveraging, even as of course the obligations (debt) have shifted around.

Wall Street's 'ice-rink Zamboni'

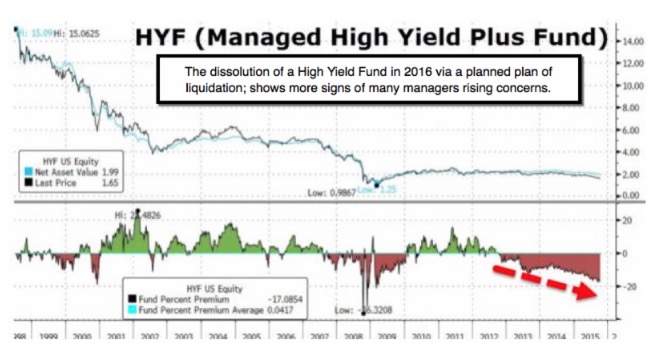

Rather than deleveraging and savings; the opposite occurred. Total world debt now exceeds $200 trillion. That's about 40% greater than before the financial crisis hit. In 2007 we called for a 'liquidity & credit crisis', elevating that later in the year to an 'Epic Debacle' call because of the derivatives issue and the Fed taking down the firewalls to allow banks and brokers to co-mingle funds; which is exactly what a firewall intends to prevent (why have it if you'll not use it).

All year we've had many superb short-sale guidelines which captured gains as the ice floes melted; as we viewed it as one of history's greatest distributions. I know it's been like the competition between 'Ice Capades' and 'Holiday on Ice', because either way the 'rink' is smoothed over at the last moment before most of the big performers (momentum stocks) totally fall through that 'thinning ice', at the same time as most remain well off their rotational highs during the year.

I'm also suggesting that it's a Zamboni effect, unrelated to basic valuations or US economic prospects, since it becomes a 'show must go on', not just should persist, (behavior). That means (discussion of how the show will progress this 4th Quarter is generally outlined to ingerletter.com subscribers only).

In sum: the downside of the 'ice cracking' should have global repercussions; so as this Expiration week is now behind, I wanted to reflect on the dangers as relate to this aspect alone. (Redacted in fairness to actual subscribers.)

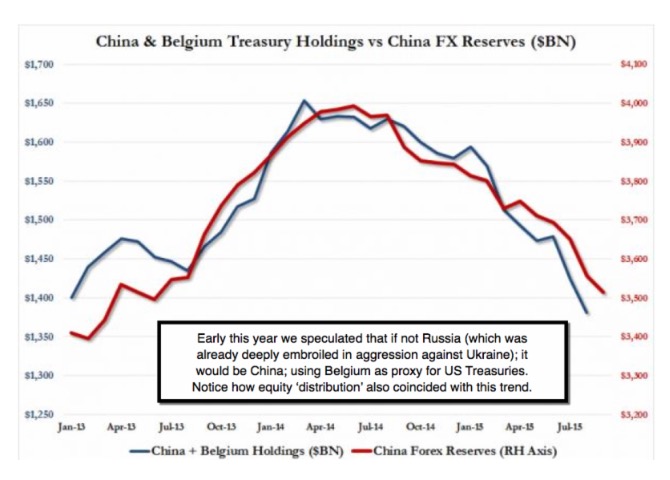

We go into the weekend with a 'rare' retained near-close Dec. S&P 2026 new guideline short, which represents 'some' skin-in-the-game not only related to a 'chance' for a shake post-Expiration; but also given suspicions Sunday night's Chinese economic news won't bolster markets overseas; and thus potentially lead to a soft New York opening. (Balance fairly just for our actual members.)

Everywhere you look there are landmines and sinkholes; while markets rely on faith in central bankers and fund-flows; while avoiding fundamental analyses or even technical analysis which doesn't say the S&P can't go higher; but clearly can chart the disconnect between market levels and any historical period that provided such an increasingly slow pace of both domestic and global growth.

That doesn't mean the market has to break here; but it means (for members).

We're short for the moment from E-mini / Dec. S&P 2026; which is a risky low probability partial bearish exposure, with a reasonable 2030 fixed mental stop for now. We'll address more for traders as we get into Monday's session.

Prior highlights follow: (generally redacted in fairness to subscribers).

That matters (redacted Intel disccussion; associated with our more favorable view weeks ago in-anticipation of SkyLake processors): as expected, Apple released a slew of new iMacs; their flagship all-in-one desktops; now mostly in high resolution Retina form. However, (pro & con discussion for members).

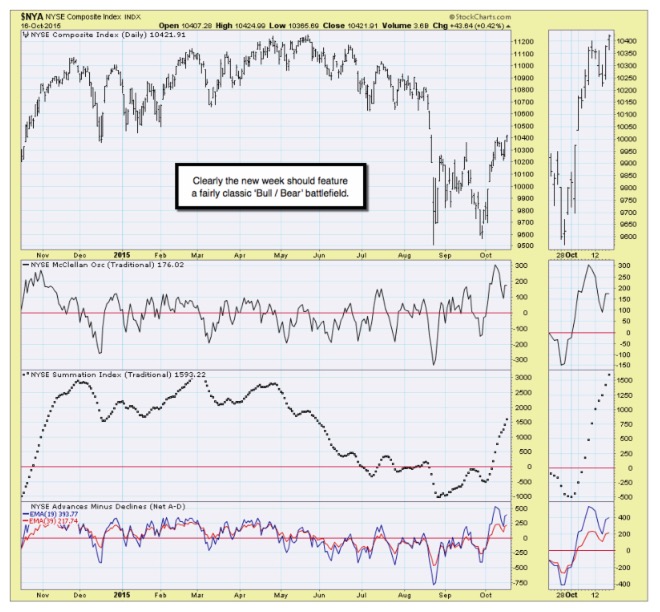

Bottom-line: this market remains (near) 'most' overbought it's been on a daily basis (stochastic work; not others) since just before the August breakdown; but that came after several weeks of 'erosion' that sapped market prior to the 'flash crash'. On a weekly basis it is not yet overbought; which (was) an argument for prior S&P extensions we've shared with members daily.

Treacherous times. The process evolves. Likely akin to 'surfing' as it nears what's sometimes called 'point break'. (In this case the rebound rolling over.)

Enjoy the weekend!

Gene

Gene Inger

www.ingerletter.com