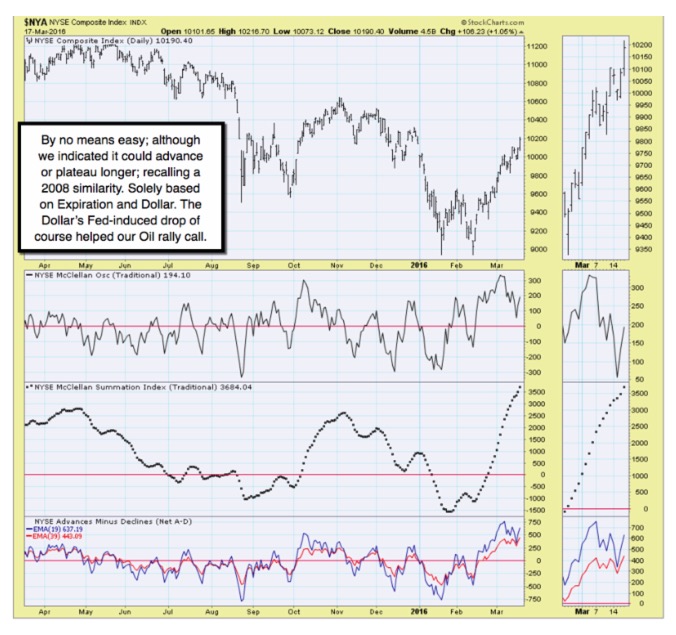

Platitudes promoting a bullish thesis - out of what's going on now are close to absurd; though no doubt this is a tricky market as we work through Expiration finales, with the Dollar down; Oil up (related obviously) and pundits promoting all kind of stories about being past any real or imagined risks (including defaults).

Actually 'some' are mitigated, as I've known would be the case if Oil prices rose; some can be mitigated if the Dollar stays down (that's the least likely prospect in the fullness of weeks ahead); as what should be mitigated is upside potential.

Of course our desired 40-45 Oil (50 would be better!) lifts stocks for now; while higher retail gasoline prices (lagging always) won't be attributed as meaningful until after Oil settles back some; and that can be as the U.S. 'engaging' in what they really will not acknowledge, finds the ying & yang coming from other sides.

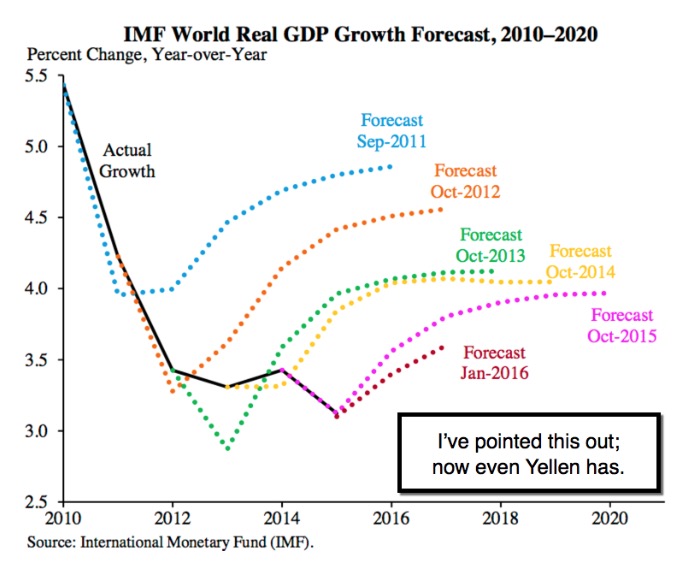

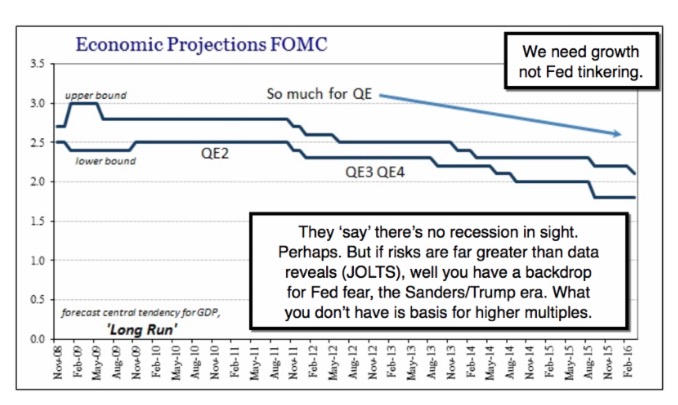

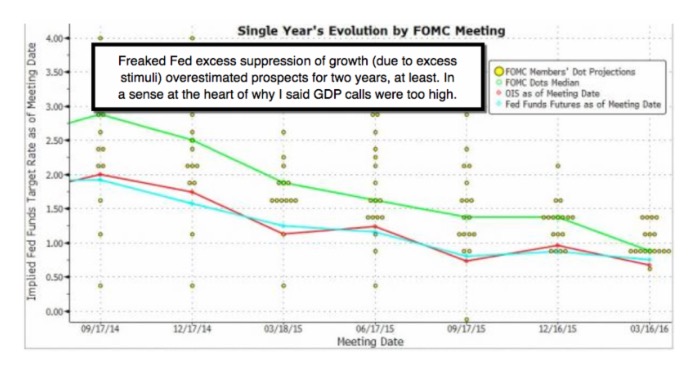

Here I'm addressing competitive devaluations, which 'are' now dragging-in the U.S.; and they won't go unmet; as the Asian countries have little else to do but devalue currencies in this economic race to the bottom. Most hoped the U.S. would not engage; but that's basically what this Fed did. They had sufficient if of course massaged data (because the economy is only better in some sectors) to firm things up or at lest be a bit hawkish; but they went 'full Monte' in a sense; by calling for slow growth for the next few years!

That's counterproductive for CapEx, encourages more buybacks, and artificially props earnings. Yes, the hints were there, by virtue of Oil making our low back in the 28-30 area (where we thought those calling for 15 or 20 were nuts after the downside); and now you DO have a Doha Oil Producer / OPEC meeting back in the coming week's calendar, so that (reserved, as anticipates next week).

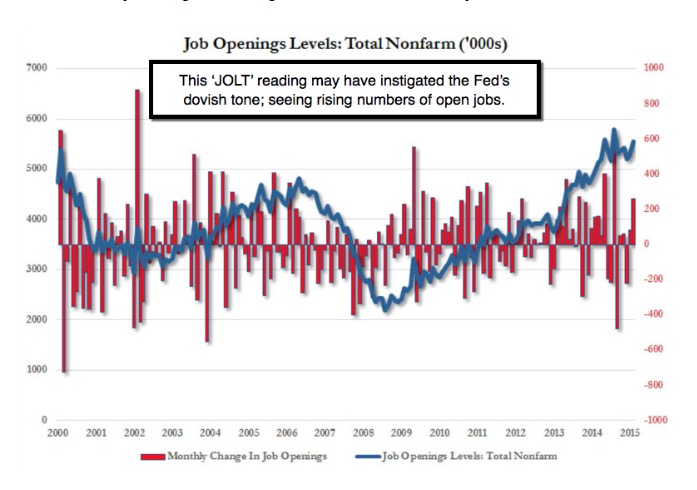

Bottom-line: as I've contended this was not and is not any sort of 'lock'; not for the Bulls who think happy days are here again; nor the bears, who are run-in big time. Technically, all the market did was make it up to our higher resistance zone in a blow-off type 'rush', spearheaded by bullish views of a Fed's insanely dovish statement, which probably was triggered a bit by a view of the JOLTs data too.

In-sum: for a couple weeks I've contrasted this effort to conclude the rebound in a sense (noted); where we had market advance in the face of negativity, through much of the Spring (which hasn't even arrived this year) before getting seriously 'clocked' again. It may not replicate that; (reasons why shared with subscribers).

It's also a potential 'bull trap' (spelled with a 't') for those who initiate chasing the upside; especially if they actually believe this is some sort of enduring economic turnaround, or surge in coming profitability for multinational companies. (More.)

Daily action - recalls G20 in Shanghai last month; where central bankers and finance ministers provided pledges to maintain currency stability; stop rocking all the boats so much; and promote global economic growth.

I suspected those were mostly platitudes too; as the Chinese PBOC head came out the next day with contrary views. Now the U.S. Fed and last night the BoJ as you know, both acted in ways that discourage believing anything from the G20. I think with the U.S. global role is so significant; it's why all markets reacted wildly; including U.S. bank stocks declining, to the point where JP Morgan did their own unusual buyback announced late Thursday.

I believe this is unhealthy leadership by our Fed; as it validates global moves we previously disdained, in terms of the 'race to the bottom'. Nobody wins if this will keep going. For pundits to hail the Dollar's drop and presume China or the ECB won't follow somehow going forward, is naive wishful thinking.

We had almost gotten to a point (at least with official language) where China, a double-speaking ECB, Japan, the U.K., and the U.S., had taken a barrage of all sorts of actions to keep the global economy afloat and currency markets calm. It is in that sense that many are aghast at what our FOMC just did (redacted); as reverberations in foreign central banks and currency markets, remain ahead.

That 'temperament' of central bankers is now in-question. Some are likely going to ponder if there's a 'secret' Shanghai Accord (none has been referred to), akin to those reached in earlier eras in New York (The Plaza Accord) or Paris (at The Louvre Museum). So if the others do not respond, then you have (reserved). We know that; but there has to be more to it, for the Fed to have been dismissive of their pledge at G20; or (discussed where this heads with our members).

Futures on equity gauges from Sydney to Hong Kong suggest Friday gains. The global impact of all this is of course still pending. It's not at all on solid footing. A for-instance (at press-time); early Friday Nikkei has Tokyo -263.

Prior highlights follow: (limited, in fairness to our subscribers).

Economic growth and higher wages - historically weren't always associated, at least for decades (typically before the Gold standard was dropped and global growth expanded, largely -in time- at the expense of American workers and our industrial expansion), with 'inflation' as somehow being 'desirable'. The idea was to see profits and growth occurring consistently, amid organically-achieved GDP gains; not any sort of financial engineering beyond consistent slow M2 growth.

In-sum: my takeaway from today's Fed 'chat' was that the global economy has and is slowing 'more' than they previously anticipated (recall there was criticism late last year about the Fed justifying their slight increase based on 'recovery').

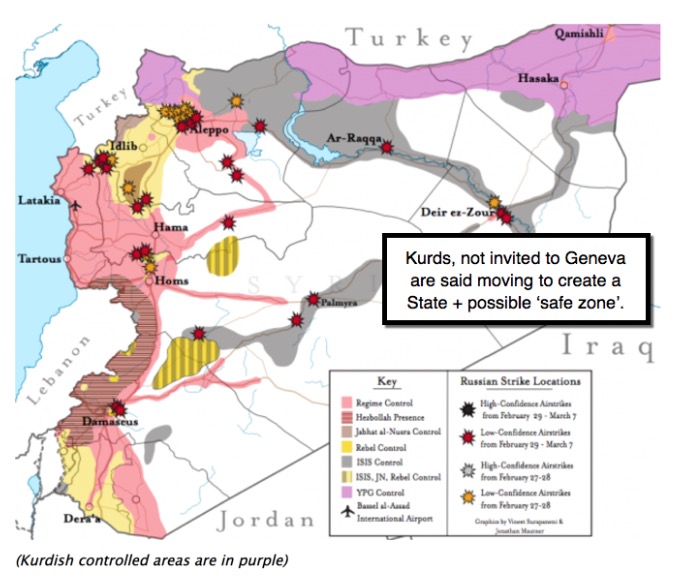

Teheran's rug merchants probably got so hard to deal with (remember originally a Russian Oil meeting which got cancelled because Kuwait, and especially Iran, despite said beholden to Russia as it relates to their cherished 'Shia Crescent', wouldn't support Russia's need for oil prices to firm); that Russia announced the partial withdrawal from Syria. Their Army was more present than widely known; as I've pointed-out a couple times. Now; whether nervous about eroding what's been achieved (from their perspective) or not, they reversed course yet-again; and a meeting in Doha is scheduled for next week regarding oil production level concerns. That supported Oil stocks and Oil; and is part of the rest of the story.

Bottom-line: the Fed's so data-dependent; and now that the S&P is challenging upper resistance levels (or threatening too), some are going to scamper from all shorts, perhaps just in-time for (balance reserved for subscribing members).

Enjoy the weekend!

Gene

Gene Inger

www.ingerletter.com