Extremes get overdone - on the downside or the upside; as the June swoon of course was seen before the projected washout on a Brexit 'Leave' vote; with the combination of both straddle and short-sale strategies, given our expectation the day ahead of Brexit, that the vote would be to 'Leave'. But either way the market had run-up so much, that it would be 'buy the rumor sell the news' (if our bias for the vote being to 'leave' hadn't occurred). The down-and-up move worked great.

From the start of this; we viewed 'alarmist' talk from everyone from UK leaders, to speculators like Soros, as probably playing to a hidden agenda; and that they would cause a panic (further op-ed's did just that Monday); but that in a sense would lead into a turnaround not later than Tuesday morning; running-in all the fear-monger types; even though all that does is take markets right back to a very risky level. Worked out quite well for options/futures and S&P swing ideas.

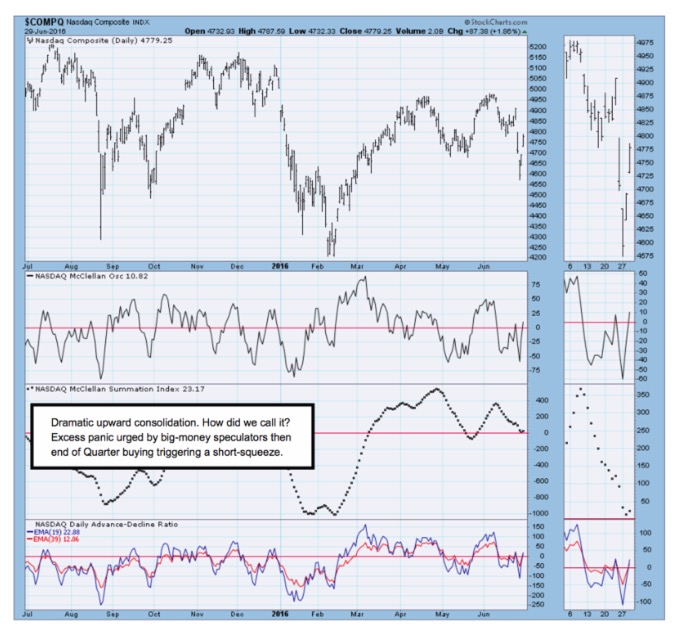

Now, some are warning that markets set-up a major bottom and we'll see newer highs; and others that because of heavy volume down and light volume on the rebound, it's the last chance to get out of everything. Both are off-base a bit for a couple reasons. (Reasons are illustrative of a combined technical-psychological approach which is just for members.) Furthermore I expected an end-of-Quarter rebound, which at the end of Q2 was part of our overall projection (more).

Still, even with the limited debates about the future of Europe; or the challenge of financial profitability at a time of difficult EU integration, raising concern about the future, and making capital spending plans difficult; beyond obvious issues in a complex world (including debt structure) by banks and sovereigns. The FTSI recovered all that was lost post-Brexit; by inference validating (our assessment that the panic sell-off would be reversed at the same time being a warning).

Markets were far from pricing-in the global economic and earnings slowdowns in the days ahead of Brexit, and while the impact of Brexit itself is (redacted for our members). However they have created a great deal of uncertainty which goes beyond always being dicey for markets. Even consumer contraction in spending plans is impacted by Brexit, and incidentally by the sadly-rising terror risk.

(By the way, though jittery, I am flying to Barcelona for a Cruise next week. With these wild markets, just as last year, I will strive to do brief daily reports as often as feasible, given internet connections. As a 'holiday special' and with reports being brief or slightly less frequent over the next 3 weeks, 'new members' only are invited to join 'now' with a larger-than-ever rebate on initial subscriptions.

Just subscribe in the normal way before July 4th, and we will promptly rebate $50 for new Daily Briefing and $100 for new MarketCast membershps. It's not only a special, but more than offsets limited reports during July's travels. Again this is available only until my flight, and for new members only.)

Bottom-line: this was a very dramatic panic on shock (to most others; we were leaning toward Brexit passing, and positioned in the market for it as well), with a requisite trampling of any investors or traders who reacted impulsively after the 'event'. To wit: shorts got run in big-time, as we forewarned from last weekend.

At the same time traders needed to harvest most gains before the turnaround; it was not a time for investors to dive in, unless their time horizon is days or at the most a couple weeks (and we said all this in outlining the prospects days earlier which matters, because while it's all been pretty wild, that's about the best guide to navigating this as close as possible to how it panned-out).

Conclusion: with extremely volatility (market spike before Brexit, collapse on it, turnaround rebound, followed by Quarter's-end activity); things should calm a bit, as we move into an early-mid July effort to stabilize and (more follows).

Daily action - saw persistent blow-off behavior which we believe is tied-into the Quarter's end prospects now; with less related to the evolving Brexit prospects. We thought S&P would rebound; the low 2070's is about the 'mean' charts will show; but intraday I suggested it could overrun; and ideally attack (reserved).

No it's not bullish; it's just a reverse panic and confused positioning by money managers, or for that matter precisely what we speculated about with regard to how some big vocal speculators were talking before and after Brexit; seemed like they were not only playing it, but driving fear into the hearts of investors to get prices even lower (so they could play the rebound). (Details follow.)

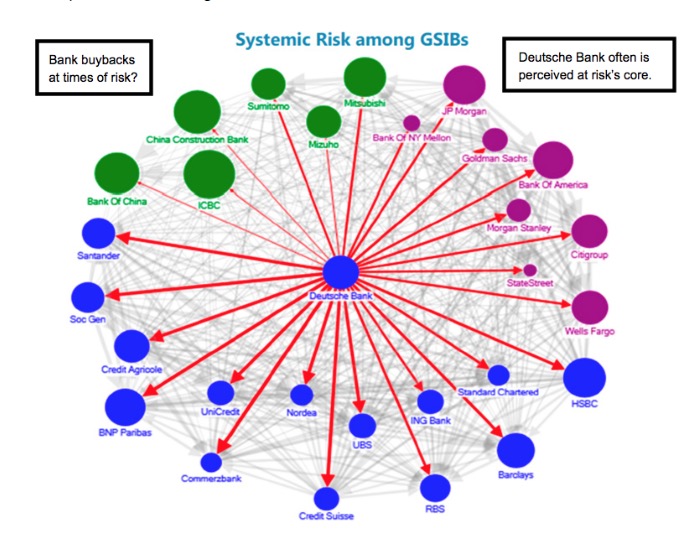

As to market pricing. Either way this is a market overhang going forward, with balance sheet worries; risks of more central bank interventions, and extended lower interest rates with a continued pressure on bank and financial institution earnings power. The huge buybacks and some dividend increases released just after Wednesday's close make one smile; with profitability challenged they're of course trying to revitalize matters by essentially leveraging the institutions more; rather than tightening their belts. A couple have to re-submit stress tests as you heard; though of course. It's really a challenge to capital markets with such low or negative interest rates for these guys to stoke interest thusly; and works just for awhile. In a sense it's interesting a few picked 'this' day; coordinated? Or did all of them have the same chutzpah coincidentally at the same time?

Zero or negative rates have significant bearish implications for the long-term as they are a reflection of exasperation or desperation by central bankers, partially in-absence of sensible fiscal policy initiatives to execute realistic new growth. If you combine the questions about liquidity, sorting-out Brexit, the FX market, as well as not exactly highly predictable, but favors relative Dollar strength, and of course blend-in the prospective mediocre earnings and revenue picture; do you really believe fundamentals don't matter, or that they will catch-up with this.

For a tiny example; the horrid Istanbul attack isn't exactly going to help tourism, or even drive more Americans to Europe with more favorable exchange rates; nor help airline profits (new bouts of fee increases imposed on behalf of security and other services, with England having among the highest already, looms as likely; and nobody will complain... we already spoke about outer security-ring as well as ground-crew security issues).

The Quarter's-end rally followed-by early July sustaining efforts (include volatile swings) is slightly reminiscent of what I used to call a 'Mom's Birthday rally' (God rest her soul); primarily because of the frequent seasonal strength into early-mid July, especially with a preceding a June swoon. This year's doing it in-spades to say the least. After that (is the likely 'process' evolution outlined to members).

Right now we want to watch fairly closely to see if this market runs into a sort of brick-wall as we move into early July; (trading details provided). For investors, it was neither wise (as we said) to sell into panic after Brexit, nor buy an upside rebound unless, as I said Monday, your time-horizon was in the realm of days.

Finally, keep in mind (and we don't wish it); but a couple major declines in stock market history were preceded by an irregular period; a sharp drop; and then the sharpest of rallies (even to higher highs) reassuring investors that all was great. Of course it was not; and declines or even a crash or two, ensued. In this case the fundamental underpinnings are not there and won't be. Danger will recur.

Prior highlights follow: (very brief summary).

'Never let a good crisis be wasted' - might be the hallmark of the incredible as well as both tardy and premature effort, by EU founding members, sending-up a couple 'trial balloons' to see how members (particularly in the new bloc of older Soviet captive nations) would react to (a special story about EU possibilities).

In the future, if it proves to be more than a 'trial balloon', it's something that risks fracturing markets for longer than otherwise would be the case.

Bottom-line: speculative reflex reaction Friday and Monday by markets and of course politicians, was actually tempered (more reflections provided).

Market technicals (via video) reviews the behavior; it's a short-covering squeeze and normal post-panic snapback; and not any sort of affirmation of a long-term bottom. Stay tuned as suggested; recalling the future 'process' agenda.

Rallies will occur (such as this; as was projected within long ongoing distribution structures with origins pushing two years old. Remember; longer the distribution; the greater the potential risk. One disconcerting aspect is most funds remain not only long or even leveraged, but in what is denial, wishful thinking, or belief they can perennially control it. We'll assess it all; join us during the best pre-holiday special we've ever offered.

Battlegrounds continue 'fluid', with multiple dynamics unfolding.

Enjoy your Independence Day!

Gene

Gene Inger