In our last submission, I said that the never-before (since the early 1990s)-seen reading from our Wall Street Sentiment Survey of ZERO Bulls was Bullish. Period. I strongly felt that we had to be longer-term bullish. After that fairly strong pronouncement, the S&P 500 dipped just a bit more and then launched into a 450-point (and counting) rally.

This week, our Wall Street Sentiment Survey has just 17% Bulls and 75% Bears. This crew is often immediately right when they get heavily leaning, but, afterward, the excesses that led to such sentiment ameliorate and the market reverses. Am I expecting a rally like what we saw after last October's minor pullback? Well, only maybe, though we absolutely cannot rule it out. No matter what, though, this reading is intermediate-term bullish.

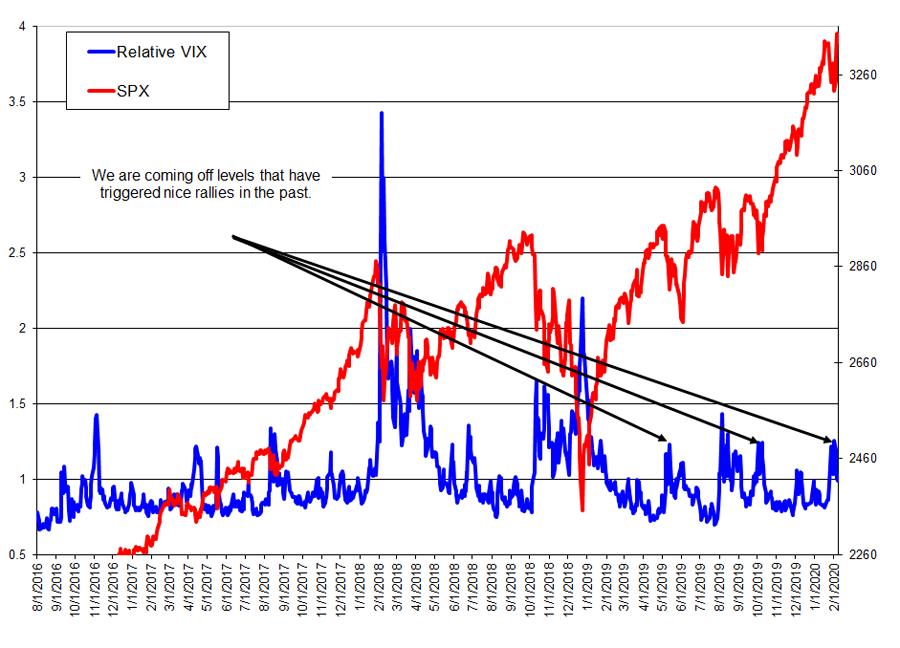

After the rather ugly January pullback, what heartened me was how quickly AAII, NAAIM, II, and especially the "FinTwit" poll (at 69% Bears) backed away from their Bullish readings. These measures are still showing remarkably little Bullishness for a market at new highs. In addition to these measures, our confidence was also bolstered by a surge in the Relative VIX. This indicator is a gold standard bottom spotter--in my view, a high Relative VIX represents "incentive" for a rally. During the January decline, this indicator shot up to Buy territory quite quickly on 1/27, triggering a bounce, then shot back up into Buy territory again on 1/31, triggering a very respectable 120 point rally in three days. This indicator, even now, is at constructive levels. It sure looks to me like there's still "incentive" to take prices higher.

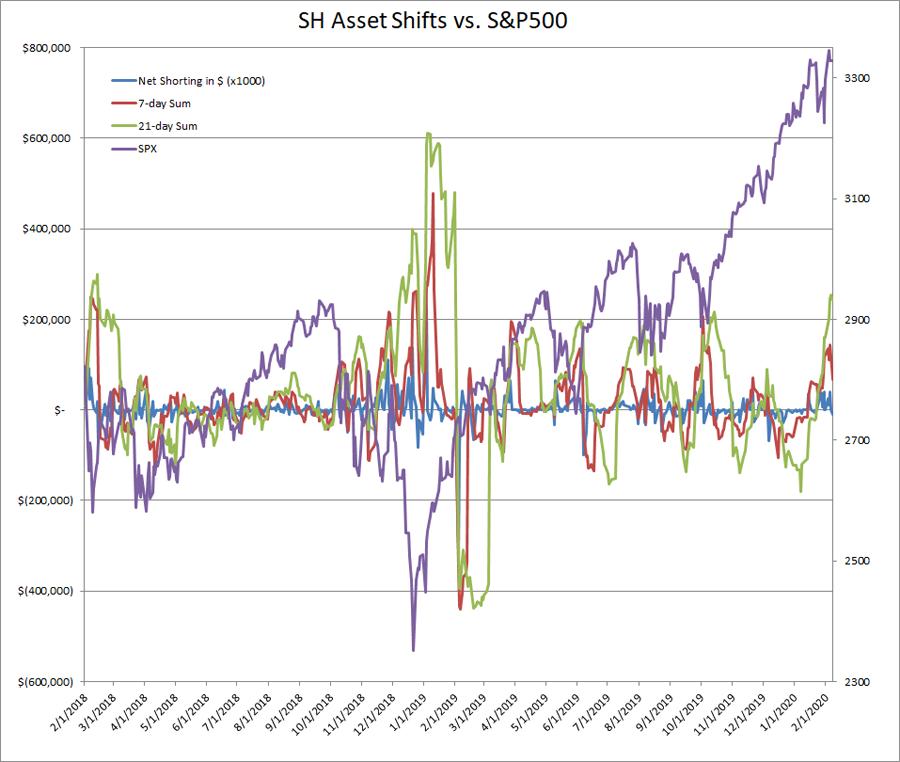

Another indicator of excessive bearishness is accumulated net new shorting via the SH (the ProShares inverse S&P 500 ETF). If there is excess demand for this ETF, sponsors will issue more shares rather than allow it to trade at a premium. We measure this share issuance. Over the past 21 trading days, traders have caused the fund sponsors to issue more than $253MM worth of new SH shares (i.e. there has been $253MM in net new shorting). This is at levels that have supported substantial multi-week rallies in the past.

Another indicator of excessive bearishness is accumulated net new shorting via the SH (the ProShares inverse S&P 500 ETF). If there is excess demand for this ETF, sponsors will issue more shares rather than allow it to trade at a premium. We measure this share issuance. Over the past 21 trading days, traders have caused the fund sponsors to issue more than $253MM worth of new SH shares (i.e. there has been $253MM in net new shorting). This is at levels that have supported substantial multi-week rallies in the past.

Overall, these indicators suggest that near-term weakness, while reasonably likely, will be met by buying and that, longer-term, we have higher prices in the works. Remember, the context that had us looking for MUCH higher prices has not meaningfully changed. We have to be generally constructive barring something major happening. Which leads me to my caveat: the technicals are fine and so is the sentiment at the moment, but international events could swamp both the economy and the stock market. A true uncontrolled pandemic would have lasting negative effects and easy visibility -- a bad combination for the stock market. So far, things seem to be contained, with the death rates seeming to be falling and relatively low outside of ground zero. If this changes meaningfully for the worse, especially outside of China, we will become much more cautious.

Have a prosperous week!

Mark Steward Young

Wall St. Sentiment

http://www.wallstreetsentiment.com/trial.htm