Market Recap for Wednesday, December 28, 2016

It's been awhile since this happened, but on Wednesday all nine sectors declined, led by energy (XLE, -1.08%), industrials (XLI, -1.05%) and financials (XLF, -1.02%). The carnage was evenly spread as consumer staples (XLP, -0.61%) and consumer discretionary (XLY, -0.69%) were the best performing sectors, but not much better than the worst. Still, the overall market remains technically sound although a few cracks in the technical foundation are emerging. The first issue could be industrials, which yesterday closed below its 20 day EMA for the first time since its latest rally began on November 7th. Check it out:

There was a slight negative divergence on the XLI's most recent price high so I typically look for a MACD centerline test and/or a 50 day SMA test (pink arrows) and a drop back to price support isn't completely out of the question. Check out the price action in mid-July. The XLI retreated back just beneath its 20 day EMA (red circle), but quickly recovered above that trending EMA. It later posted a high in late August and a negative divergence printed. From there, the XLI traded sideways down to price support (green dotted line). The current rally broke out above those highs at roughly 58.50 and that's the most significant price support on this chart in my view. The second red circle marks yesterday's close beneath the XLI's rising 20 day EMA. This time it comes with a slight negative divergence in play. Therefore, holding on is much riskier at this point. I'd look for a close back above the 20 day EMA quickly or the momentum swings back to the bears in the near-term.

There was a slight negative divergence on the XLI's most recent price high so I typically look for a MACD centerline test and/or a 50 day SMA test (pink arrows) and a drop back to price support isn't completely out of the question. Check out the price action in mid-July. The XLI retreated back just beneath its 20 day EMA (red circle), but quickly recovered above that trending EMA. It later posted a high in late August and a negative divergence printed. From there, the XLI traded sideways down to price support (green dotted line). The current rally broke out above those highs at roughly 58.50 and that's the most significant price support on this chart in my view. The second red circle marks yesterday's close beneath the XLI's rising 20 day EMA. This time it comes with a slight negative divergence in play. Therefore, holding on is much riskier at this point. I'd look for a close back above the 20 day EMA quickly or the momentum swings back to the bears in the near-term.

Heavy construction ($DJUSHV) was the worst performing industry group yesterday within industrials and the short-term problem here is a bit more obvious. Take a look:

The break beneath its 20 day EMA is more severe as is its negative divergence. The 440-460 price range is relatively solid support in the very near-term and the rising 50 day SMA, just beneath this range currently, should provide support as well. If this range is lost, look to the major price support just beneath 420 as the likely level for the group to pivot.

The break beneath its 20 day EMA is more severe as is its negative divergence. The 440-460 price range is relatively solid support in the very near-term and the rising 50 day SMA, just beneath this range currently, should provide support as well. If this range is lost, look to the major price support just beneath 420 as the likely level for the group to pivot.

Pre-Market Action

U.S. stocks are poised for a flat open on Thursday following its broad-based profit taking on Wednesday. Overnight, Asian markets were mixed with the Tokyo Nikkei ($NIKK) falling 257 points, its worst showing in six weeks. Other key global markets are relatively flat, including Europe this morning where the German DAX ($DAX) continues to struggle with overhead resistance at 11500.

The 10 year treasury yield ($TNX) is down this morning to 2.49% and there's 20 day EMA support at 2.46% and yield support at 2.44%. A close below those two levels would likely to lead to more buying of treasuries and lower treasury yields, an event that would put much more pressure on financial stocks, particularly banks ($DJUSBK) and life insurance companies ($DJUSIL).

The U.S. Dollar Index ($USD) remains near its recent high so the recent rally in gold ($GOLD) is not likely to stick unless we see weakness from the greenback. Gold will most likely struggle in the 1155-1165 resistance area without support from a falling dollar.

Current Outlook

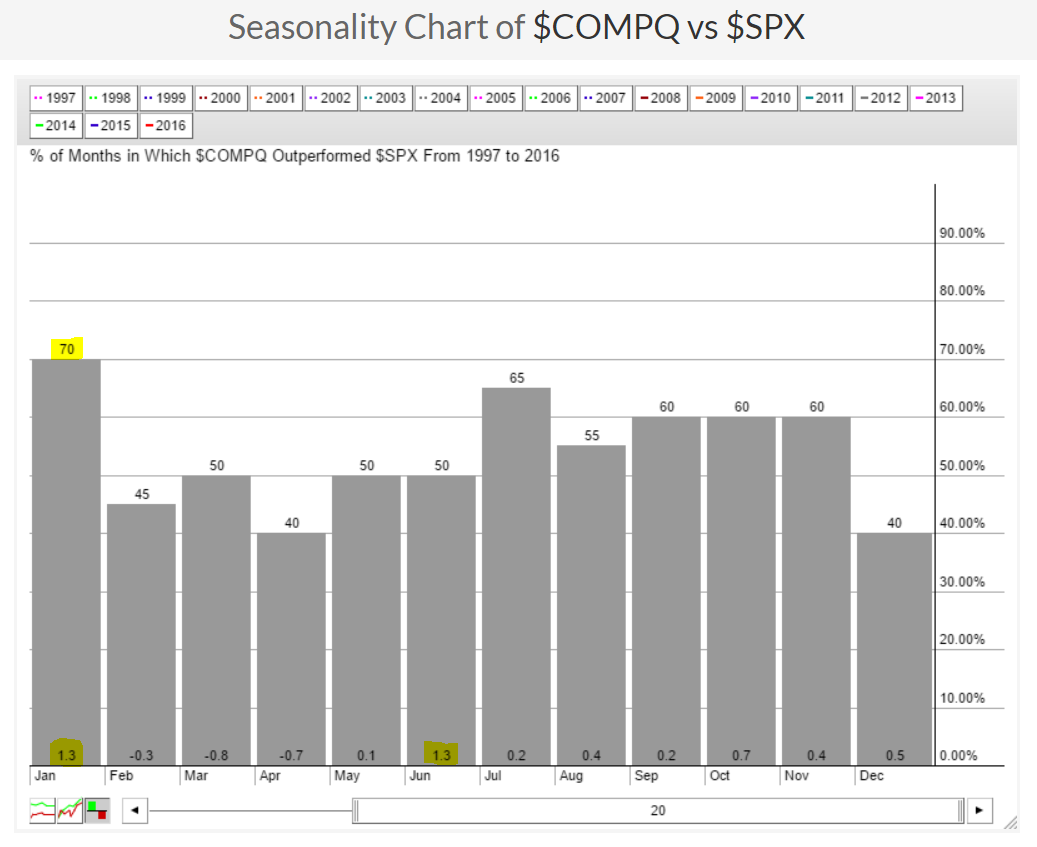

Historically speaking, the NASDAQ is the best investing alternative in January, at least vs. the S&P 500 and Russell 2000. Below are two seasonal charts comparing the performance of the NASDAQ vs. the benchmark S&P 500 (repeat from chart shown yesterday) and then the Russell 2000. Check this out:

NASDAQ vs. S&P 500:

The NASDAQ has outperformed the S&P 500 70% of the time during January over the last 20 years with an average outperformance of 1.3% each January. June is the only other month with an average outperformance of 1.3% and that month has been more of a crapshoot with the NASDAQ leading only 50% of the time.

The NASDAQ has outperformed the S&P 500 70% of the time during January over the last 20 years with an average outperformance of 1.3% each January. June is the only other month with an average outperformance of 1.3% and that month has been more of a crapshoot with the NASDAQ leading only 50% of the time.

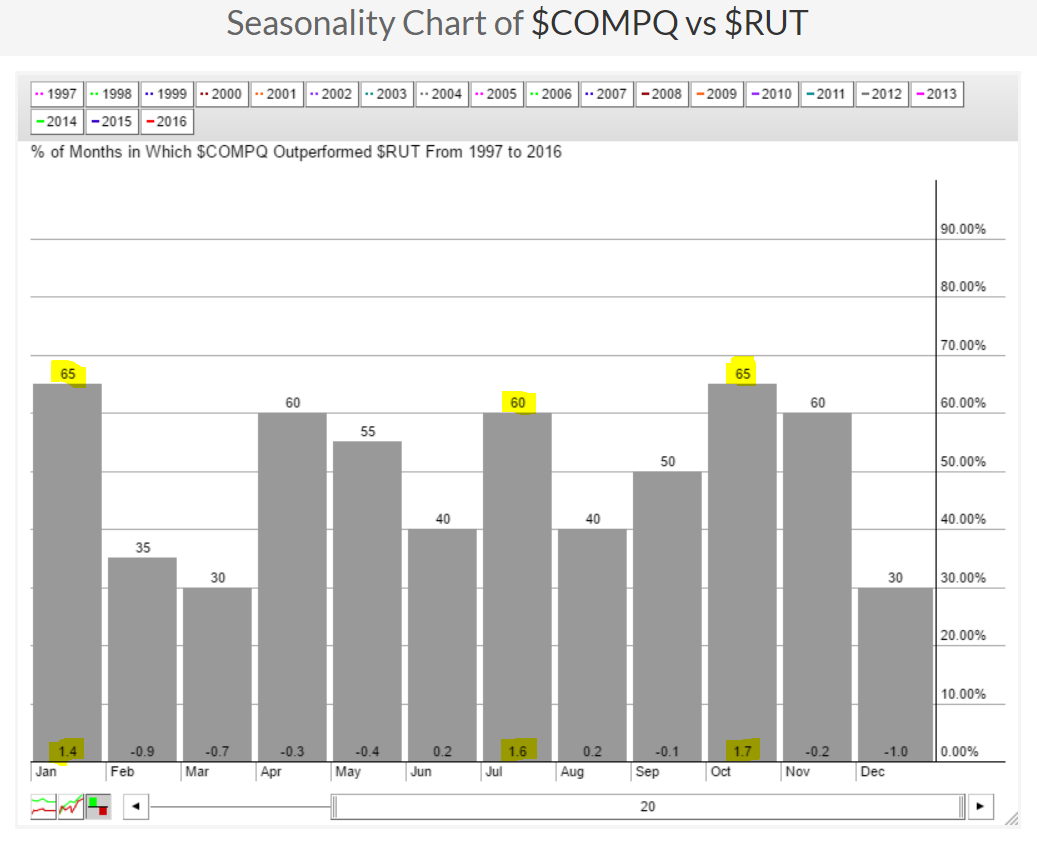

The NASDAQ also outperforms small cap stocks during January as you can see from the next seasonal chart:

The relative strength swings between these two aggressive indices is more significant but the NASDAQ's relative strength is obvious in January with its relative outperformance stronger only during October and July.

The relative strength swings between these two aggressive indices is more significant but the NASDAQ's relative strength is obvious in January with its relative outperformance stronger only during October and July.

Given this history, I'd weight NASDAQ stocks heavier in my portfolio over the next 4-5 weeks, especially those with strong technical conditions and patterns in play.

Sector/Industry Watch

The only strength to be seen in the stock market on Wednesday was in beaten down groups like clothing & accessories (the only industry group in consumer discretionary to finish higher), gold mining and distillers & vintners. Take a look at these leading groups on Wednesday and how poor their technical price action was previously:

While much of the market sold off yesterday, money did rotate somewhat into groups that simply have been abysmal the past several months. All of the above remain technically weak and I'd avoid the groups until their respective downtrends have been broken and rising 20 day EMAs begin to act as support.

While much of the market sold off yesterday, money did rotate somewhat into groups that simply have been abysmal the past several months. All of the above remain technically weak and I'd avoid the groups until their respective downtrends have been broken and rising 20 day EMAs begin to act as support.

Historical Tendencies

Bringing in a new year typically results in higher stock prices. Below are the annualized returns for each calendar day from December 29th through January 6th on the S&P 500 since 1950:

December 29: +43.90%

December 30: +41.05%

December 31: +33.68%

January 2: +71.26%

January 3: +62.06%

January 4: +7.83%

January 5: +36.14%

January 6: +17.89%

Despite the above, the S&P 500 has lost ground during this period over the last three years so the bulls will be looking to end their recent losing streak.

Key Earnings Reports

None

Key Economic Reports

Initial jobless claims released at 8:30am EST: 265,000 (actual) vs. 262,000 (estimate)

Happy trading!

Tom