Market Recap for Thursday, March 30, 2017

It was another strong day on Wall Street Thursday as six sectors advanced while only three declined - utilities (XLU, -0.78%), consumer staples (XLP, -0.20%) and energy (XLE, -0.02%). The four "power" sectors, the aggressive groups, finished 1-2-3-4 yesterday so clearly money rotated to offense - a very good sign. In fact, that rotation to aggressive areas of the market this week is illustrated in the Current Outlook section below.

Leading the charge were the financials (XLF, +1.31%) as banks ($DJUSBK) have re-emerged as leaders again. The current technical view of banks is highlighted below in the Sector/Industry Watch section below. Life insurance ($DJUSIL) surged along with banks this week, bouncing off of key price support during its four month consolidation. Here's the visual:

The reversing candle to hang onto price support was huge technically and set the DJUSIL for gains this week. Now the test will be clearing that declining 20 day EMA with a MACD that's below its centerline. We cleared it fractionally yesterday, but I'd like to see follow through today to be more comfortable.

The reversing candle to hang onto price support was huge technically and set the DJUSIL for gains this week. Now the test will be clearing that declining 20 day EMA with a MACD that's below its centerline. We cleared it fractionally yesterday, but I'd like to see follow through today to be more comfortable.

Pre-Market Action

I've put a couple charts in this article today, highlighting key resistance areas on both banks and life insurance companies. Their leadership will be very dependent on a rising 10 year treasury yield ($TNX). The TNX currently resides at 2.43%, up one basis point this morning. A move back toward 2.62% would no doubt continue to lift the DJUSBK and the DJUSIL.

Dow Jones futures are down 8 points this morning, with 30 minutes left to the opening bell, following weakness overnight in Asia and overnight in Europe.

Current Outlook

I've been waiting to see how the "under the surface" signals would react during the next market rally. Why? Because we've seen a bit of deterioration in the underlying strength of the bull market rally since the end of 2016. Monday had been rotating toward defense. The action this week, however, has been extremely bullish as you can see below:

This is a quick visual to show us that the stock market rally this week is being led once again by aggressive areas of the market. I especially like the XLY:XLP ratio as I've found that ratio to be one of the most reliable in evaluating the sustainability of rallies. Based on the current "beneath the surface" action, I'm looking for further strength in U.S. equities to open April. We'll see.

This is a quick visual to show us that the stock market rally this week is being led once again by aggressive areas of the market. I especially like the XLY:XLP ratio as I've found that ratio to be one of the most reliable in evaluating the sustainability of rallies. Based on the current "beneath the surface" action, I'm looking for further strength in U.S. equities to open April. We'll see.

Sector/Industry Watch

The Dow Jones U.S. Banks Index ($DJUSBK) led the market rally in November and December and has been somewhat dormant since. However, the group resumed its leadership and strength this week and with earnings coming up on several of the major banks over the next 2-3 weeks, I would not at all be surprised to see a pre-earnings run up. There are technical obstacles that must be cleared though. Here's the current look at the chart:

The technical issues should be clear after looking at this chart. There's a "potential" topping head & shoulders pattern in play with a heavy volume close beneath 390 as your confirmation for more weakness ahead. I don't believe it'll happen though. Instead, watch that declining 20 day EMA and MACD (red circles). Normally, after a bearish MACD centerline cross, the declining 20 day EMA becomes very significant resistance. The bulls are hoping to see a confirmed close above that moving average to kick start the DJUSBK to more significant gains.

The technical issues should be clear after looking at this chart. There's a "potential" topping head & shoulders pattern in play with a heavy volume close beneath 390 as your confirmation for more weakness ahead. I don't believe it'll happen though. Instead, watch that declining 20 day EMA and MACD (red circles). Normally, after a bearish MACD centerline cross, the declining 20 day EMA becomes very significant resistance. The bulls are hoping to see a confirmed close above that moving average to kick start the DJUSBK to more significant gains.

Historical Tendencies

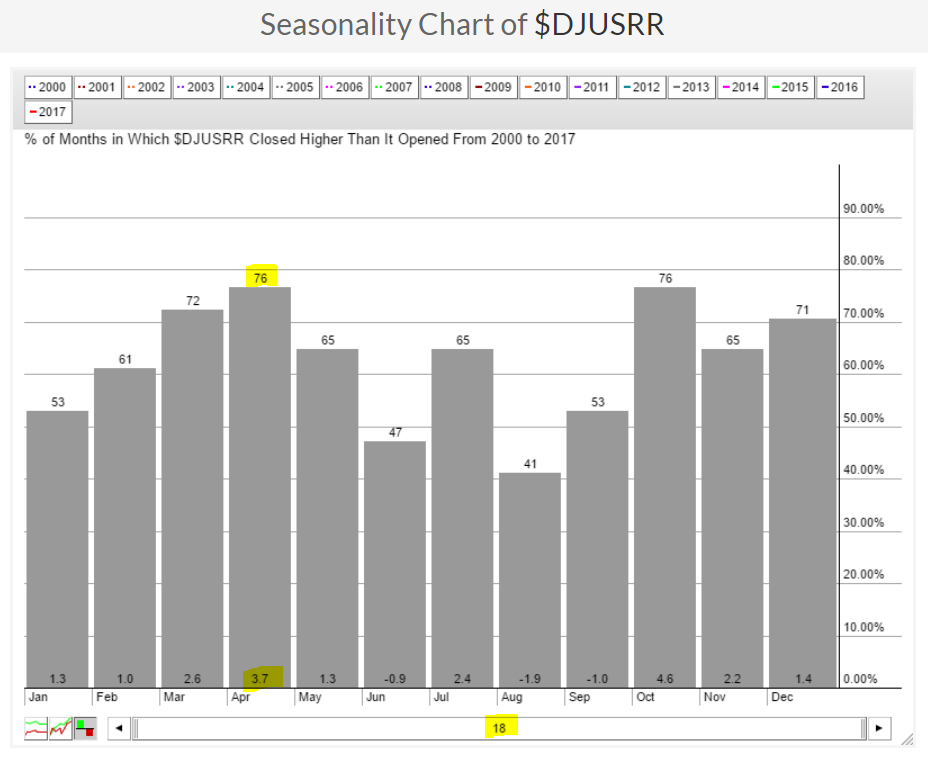

The Dow Jones U.S. Railroads Index ($DJUSRR) hit key gap support earlier this week and has bounced nicely since. The DJUSRR was the leading industry group in the industrials sector on Thursday and if seasonal patterns are any indication, I'd look for this strength to continue. Check out the historical performance below:

Railroads show a history of strengthening throughout the first four months of the year and technically the group appears strong right now. Therefore, I consider the historical April strength as simply one more reason to look for April leadership from this area of the market.

Railroads show a history of strengthening throughout the first four months of the year and technically the group appears strong right now. Therefore, I consider the historical April strength as simply one more reason to look for April leadership from this area of the market.

Key Earnings Reports

(actual vs. estimate):

BBRY: (.01) vs (.04)

Key Economic Reports

February personal income released at 8:30am EST: +0.4% (actual) vs. +0.4% (estimate)

February personal spending released at 8:30am EST: +0.1% (actual) vs. +0.2% (estimate)

March Chicago PMI to be released at 9:45am EST: 57.0 (estimate)

March consumer sentiment to be released at 10:00am EST: 97.6 (estimate)

Happy trading!

Tom