Market Recap for Monday, November 6, 2017

Energy (XLE, +2.29%) shares made a huge advance on Monday as money rotated to this once-forgotten sector in a very big way. Bull markets thrive on broad participation in rallies and the XLE had been one sector not participating. That is no longer the case as all technical signs point to higher prices in this space. Here's the latest look at the XLE:

If you had any doubts about the staying power of the September rally in XLE, they should be gone now. Price action and volume trends do not lie and serious accumulation is taking place in energy. Recent quarterly earnings reports are also supporting higher prices as many more energy companies are now beating Wall Street consensus estimates. Pullbacks represent opportunities.

If you had any doubts about the staying power of the September rally in XLE, they should be gone now. Price action and volume trends do not lie and serious accumulation is taking place in energy. Recent quarterly earnings reports are also supporting higher prices as many more energy companies are now beating Wall Street consensus estimates. Pullbacks represent opportunities.

Consumer discretionary (XLY, +0.73%) also performed very well on Tuesday and I feature that sector below in the Sector/Industry Watch section. The other side of the consumer space - consumer staples (XLP, -1.07%) - is not faring so well as traders are clearly making their choice among consumer stocks. They want the more aggressive discretionary stocks and that suggests improving economic conditions ahead. Remember, Wall Street is a leading economic indicator as it looks ahead and anticipates upcoming economic conditions....and which areas of the market are most likely to benefit.

Pre-Market Action

With about 45 minutes left to the opening bell, Dow Jones futures are higher by 13 points. S&P 500 and NASDAQ futures, however, are down ever-so-slightly. Crude oil ($WTIC) is pausing, down 4 cents to $57.31 per barrel, after a major breakout above $55 per barrel in recent days. WTIC had not closed above $55 per barrel since late-June 2015. The next stop on crude would appear to be the consolidation from the May-June 2015 reaction high (off the steep 2014 downtrend) in the $65-$67 per barrel range. Movement to that level would no doubt help to "fuel" a further advance in energy shares.

Overnight, we saw a huge rally in both the Tokyo Nikkei ($NIKK) and Hong Kong Hang Seng ($HSI), with these two indices rising 1.73% and 1.39%, respectively. China's Shanghai Composite ($SSEC) added 0.80%. Thus far, we're seeing fractional losses across many indices in Europe this morning.

Current Outlook

My favorite relative ratio to view the underlying strength of any bull market rally is to compare the relative strength of consumer discretionary stocks to consumer staples stocks (XLY:XLP). The reason is quite simple. Consumer discretionary stocks' earnings increase much more rapidly during periods of economic expansion. Consumers feel wealthier and spend more money on items they want, or discretionary items. Staples companies produce items we need and are typically purchased no matter the economic conditions. As an example, do you decide whether to buy toothpaste, soap or deodorant based on how you feel about your wealth or earnings potential? I certainly hope not or this would be a horrible place to live during bear markets. Discretionary items, on the other hand, are impacted greatly by economic conditions or perceived economic conditions.

So as the S&P 500 moves higher, I look to the XLY:XLP ratio to determine the sustainability of an S&P 500 advance. This ratio has been very strong of late and gives me little reason to doubt the rally in U.S. equities:

Bear markets do have a history of beginning with a shift in leadership to defensive areas of the market. One look at the chart above and "bear market" is the furthest thing on my mind.

Bear markets do have a history of beginning with a shift in leadership to defensive areas of the market. One look at the chart above and "bear market" is the furthest thing on my mind.

Sector/Industry Watch

The above relative ratio shows the XLY performing relative to the XLP. Below I show how the XLY is behaving bullishly on an absolute basis. Take a look:

After advancing throughout the first five months of 2017, the XLY sideways consolidated with defined areas of price resistance (red arrows) and price support (green arrows) for the next five months before breaking out just last week. The behavior since that breakout has been quite bullish, with the rising 20 day EMA (blue arrow) providing excellent support on its first test - as it should when price momentum is expected to accelerate.

After advancing throughout the first five months of 2017, the XLY sideways consolidated with defined areas of price resistance (red arrows) and price support (green arrows) for the next five months before breaking out just last week. The behavior since that breakout has been quite bullish, with the rising 20 day EMA (blue arrow) providing excellent support on its first test - as it should when price momentum is expected to accelerate.

Historical Tendencies

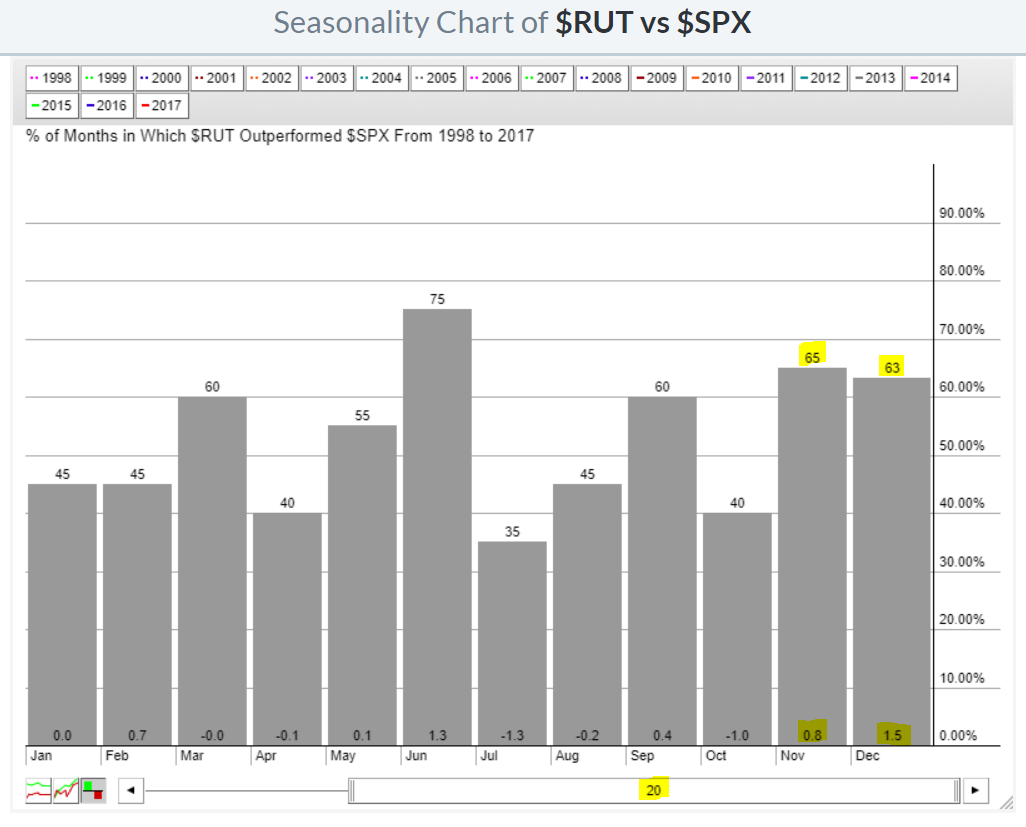

Over the past two decades, November and December are the best two months in terms of Russell 2000 outperformance with respect to the benchmark S&P 500:

I mention this because the RUT has been consolidating strong gains accumulated during the six week period that ended in early October. We're now bullishly consolidating at the rising 20 day EMA and I'd look for short-term acceleration to the upside and near-term outperformance from this small cap index.

I mention this because the RUT has been consolidating strong gains accumulated during the six week period that ended in early October. We're now bullishly consolidating at the rising 20 day EMA and I'd look for short-term acceleration to the upside and near-term outperformance from this small cap index.

Key Earnings Reports

(actual vs. estimate):

CBOE: .89 vs .88

CCE: .68 vs .68

EMR: .83 vs .80

HCN: 1.08 vs 1.05

(reports after close, estimate provided):

AGU: (.01)

CLR: .03

DXC: 1.53

EC: .23

ETE: .34

ETP: .22

MAR: .98

SNAP: (.14)

TTWO: .74

XEC: .97

Key Economic Reports

None

Happy trading!

Tom