Market Recap for Thursday, November 2, 2017

Financials (XLF, +0.94%) and industrials (XLI, +0.57%) led a Dow Jones rally on Thursday. Goldman Sachs (GS) paced the financial stocks in the Dow with more than a 1% gain, while Boeing (BA) was the best performing Dow component and the obvious leader in industrials. It was not really a broad-based rally on Thursday, however, as the NASDAQ actually lost ground despite an early push higher in Facebook (FB) following its better-than-expected quarterly earnings report. It was likely a "buy on rumor, sell on news" type of even for FB as solid earnings were anticipated by traders, especially after seeing Amazon.com (AMZN), Microsoft (MSFT), Alphabet (GOOGL) and Intel (INTC) all report such great quarterly results and watching all four stocks gap higher in response. FB was up temporarily in after hours trading on Wednesday, but gapped lower at the opening bell yesterday. It has short-term support in the 174-176 area as follows:

FB saw very heavy volume to accompany its latest advance, a bullish sign of accumulation. I don't expect weakness to last more than a few days, despite Thursday's gap down to leave Wednesday's candle on an "island". This is a reversing candle so look for a bit more weakness at least down into that 174-177 area before FB breaks out to new highs. I'll be discussing reversing candlesticks on MarketWatchers LIVE at noon EST so join me if you can.

FB saw very heavy volume to accompany its latest advance, a bullish sign of accumulation. I don't expect weakness to last more than a few days, despite Thursday's gap down to leave Wednesday's candle on an "island". This is a reversing candle so look for a bit more weakness at least down into that 174-177 area before FB breaks out to new highs. I'll be discussing reversing candlesticks on MarketWatchers LIVE at noon EST so join me if you can.

The NASDAQ's failure to participate in Thursday's rally in part relates to this index's lack of financial stock participation (other than a few financial administration stocks), which led the rally. Apple (AAPL) reported its quarterly results last night and, from all pre-market indications, it appears the NASDAQ will get a solid boost from AAPL today.

Pre-Market Action

The two biggest pieces of news today are (1) another blowout quarterly earnings report from Apple (AAPL) and (2) a very solid jobs report that managed to come in lower than expected.

Traders were gravitating to bonds earlier, but that appears to be reversing. Still, the 10 year treasury yield ($TNX) remains slightly lower, down fractionally near the 2.35% level. Equity bulls would like to see the TNX reverse from this level as we're currently just beneath the rising 20 day EMA.

Dow Jones futures are higher this morning by 27 points with less than 30 minutes until the opening bell. The NASDAQ looks to significantly outperform - at least in early action - due to AAPL's 3.7% pre-market move higher.

Current Outlook

I'll be looking for leadership in consumer discretionary (XLY, -0.75%) today. The group was very weak yesterday, but did manage to bounce off its lows to hang onto rising 20 day EMA support. Given last week's breakout, this successful support test is important and needs to be followed up with short-term strength:

Price support just beneath 92 was lost at Thursday's open and the intraday lows penetrated the rising 20 day EMA. The Thursday low also approached the rising short-term trendline that's been in play for more than two months. A bounce from the current level on the XLY would help to sustain the bull market rally.

Sector/Industry Watch

Specialty retailers ($DJUSRS) saw renewed strength in the consumer discretionary space on Thursday and, after closing at its highest level since early October, seems poised for another breakout in the days ahead. This has all the markings of a potential cup forming:

I really like the spike in volume to accompany yesterday's multi-week closing high and believe it's likely that this starts the potential formation of the right side of a bullish continuation pattern - the cup with handle. Ultimately, a breakout above 1150 would be the bullish confirmation.

I really like the spike in volume to accompany yesterday's multi-week closing high and believe it's likely that this starts the potential formation of the right side of a bullish continuation pattern - the cup with handle. Ultimately, a breakout above 1150 would be the bullish confirmation.

Historical Tendencies

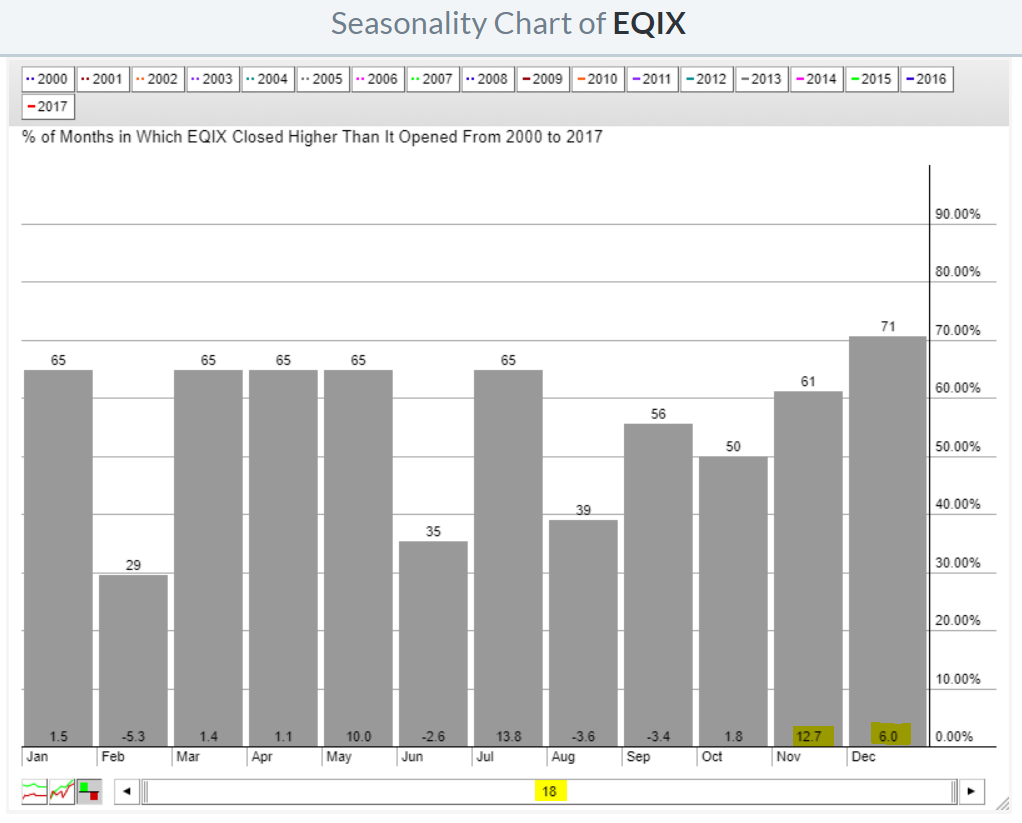

In a recent ChartWatchers article, I pointed out that Equinix (EQIX) was one of the best performing stocks in the S&P 500 during the month of November. Yesterday's 4.6% advance cleared cup resistance as EQIX looks to move higher once again in November. Here's the seasonality chart:

Check out those average monthly returns for November and December!

Check out those average monthly returns for November and December!

Key Earnings Reports

(actual vs. estimate):

DUK: 1.59 vs 1.56

MCO: 1.52 vs 1.44

Key Economic Reports

October nonfarm payrolls released at 8:30am EST: 261,000 (actual) vs. 325,000 (estimate)

October private payrolls released at 8:30am EST: 252,000 (actual) vs. 320,000 (estimate)

October unemployment rate released at 8:30am EST: 4.1% (actual) vs. 4.2% (estimate)

October average hourly earnings released at 8:30am EST: +0.0% (actual) vs. +0.2% (estimate)

October PMI services index to be released at 9:45am EST: 55.9 (estimate)

September factory orders to be released at 10:00am EST: +1.2% (estimate)

October ISM non-manufacturing index to be released at 10:00am EST: 58.6 (estimate)

Happy trading!

Tom