Market Recap for Wednesday, January 24, 2018

Only the Dow Jones was able to end Wednesday's session in positive territory, but all of our major indices remain very strong with accelerating bullish price momentum. Sectors and industries have taken their turns leading U.S. stocks higher and yesterday it was banks ($DJUSBK) and insurance - full line ($DJUSIF), brokers ($DJUSIB) and life ($DJUSIL). The 10 year treasury yield ($TNX) jumped three basis points to 2.65% and that sent traders right back into interest-sensitive stocks that benefit from higher rates.

Goldman Sachs (GS) was the best performing Dow component, rising 2.15% and breaking out:

Meanwhile, we saw weakness throughout many areas of the stock market and the S&P 500 saw notable weakness from airlines ($DJUSAR) after United Continental (UAL) hinted at price wars looming in the industry. Five of the seven worst performers on the S&P 500 were airline stocks with UAL being the biggest loser, falling 11.44% on the session.

Meanwhile, we saw weakness throughout many areas of the stock market and the S&P 500 saw notable weakness from airlines ($DJUSAR) after United Continental (UAL) hinted at price wars looming in the industry. Five of the seven worst performers on the S&P 500 were airline stocks with UAL being the biggest loser, falling 11.44% on the session.

Texas Instruments (TXN) reported its quarterly results on Tuesday after the bell and traders were not impressed. The semiconductor giant posted EPS that matched Wall Street expecations and revenues that actually exceeded analysts' projections, but TXN had climbed more than 25% in the seven weeks leading up to earnings. Put a simpler way, TXN was priced for perfection and their results just weren't good enough to sustain that prior advance. Chalk it up to the "buy on rumor, sell on news" theory.

Pre-Market Action

Solid earnings in many prominent U.S. companies continue to aid the major U.S. stock indices. Caterpillar (CAT) is the latest company to power past its quarterly revenue and EPS estimates. CAT is up nearly 2.5% in pre-market action this morning.

Crude oil ($WTIC) is continuing its rally from Wednesday, up 1.16% and above the $66 per barrel level. Gold ($GOLD) and the 10 year treasury yield ($TNX) are flat. The U.S. Dollar is weak this morning against most foreign currencies and that contributed to overnight weakness in Asian shares. Europe, however, is seeing small gains in early action.

Home Depot (HD) followed in the footsteps of JP Morgan Chase (JPM) and Starbucks (SBUX), citing tax reform as a reason to provide employees a pay boost. HD announced that hourly employees would receive up to a $1000 bonus.

With a little more than 30 minutes left to the opening bell, Dow Jones futures are up 119 points.

Current Outlook

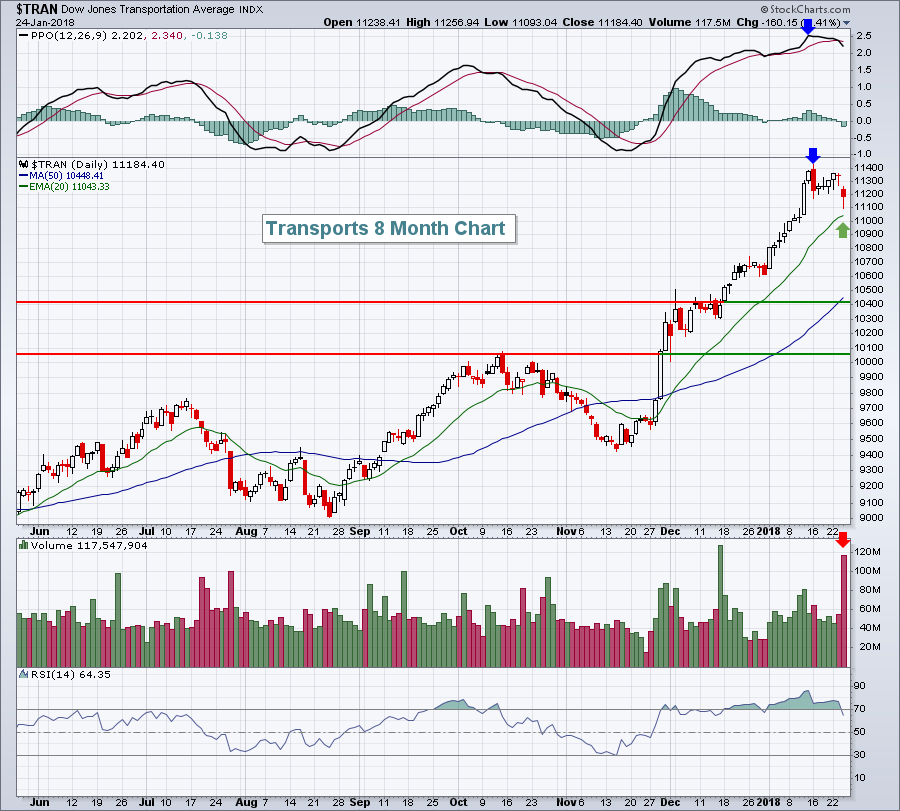

Transportation stocks ($TRAN) took a hit on Wednesday, primarily due to a very weak airlines group. However, the short-term chart remains quite bullish and, outside of a bit of short-term profit taking down to perhaps a 20 day EMA test, I'd look for higher prices in transports:

The RSI has been above 70 for much of the past two months and could certainly use a rest. The red arrow highlights the heavy volume that accompanied Wednesday's selloff - much of this accompanied airline stocks. On the bullish side of the ledger, however, is the higher PPO at the most recent price high (blue arrows) and that indicates accelerating bullish price momentum. Finally, when we see bullish price acceleration, we also typically see the rising 20 day EMA (green arrow) provide excellent support. Despite the selling yesterday, transports remain quite bullish in my view.

The RSI has been above 70 for much of the past two months and could certainly use a rest. The red arrow highlights the heavy volume that accompanied Wednesday's selloff - much of this accompanied airline stocks. On the bullish side of the ledger, however, is the higher PPO at the most recent price high (blue arrows) and that indicates accelerating bullish price momentum. Finally, when we see bullish price acceleration, we also typically see the rising 20 day EMA (green arrow) provide excellent support. Despite the selling yesterday, transports remain quite bullish in my view.

Sector/Industry Watch

Over the past month, the Dow Jones U.S. Waste & Disposal Services Index ($DJUSPC) has gained ground (+2.58%), but has trailed most of its peer industry groups within the four aggressive sectors - technology (XLK), industrials (XLI), consumer discretionary (XLY) and financials (XLF). The reason? Well there could be plenty, but technically it appears that price momentum to the upside has slowed in January, making it difficult for the DJUSPC to build on its prior gains:

Volume (ie, interest) in the DJUSPC has slowed considerably and that has accompanied a stalling of price momentum, or negative divergence. This group, while still quite bullish longer-term, is subject to more short-term selling or sideways consolidation. Better entries into stocks within this industry group lie ahead, in my opinion.

Volume (ie, interest) in the DJUSPC has slowed considerably and that has accompanied a stalling of price momentum, or negative divergence. This group, while still quite bullish longer-term, is subject to more short-term selling or sideways consolidation. Better entries into stocks within this industry group lie ahead, in my opinion.

Historical Tendencies

February has been an interesting month for the NASDAQ. Since 1971, it's produced annualized returns of +8.34%, which ranks February 9th among all 12 calendar months. However, the last two decades have produced wild annualized returns. During the 2000-2009 decade, there were two bear markets and February was hit very hard. Its annualized return of -35.18% trailed only September as the worst calendar month of the decade. From 2010 through today, February has been a shining star in terms of stock market performance, producing annualized returns of +50.70%, trailing only October's astonishing +69.38% annualized return.

Key Earnings Reports

(actual vs. estimate):

AAL: .95 vs .92

AEP: .85 vs .81

BIIB: 5.26 vs 5.44

CAT: 2.16 vs 1.77

CELG: 2.00 vs 1.95

FCAU: .65 vs .59

LLL: 2.35 vs 2.30

LUV: .77 vs .76

MMM: 2.10 vs 2.03

NOC: 2.82 vs 2.75

PX: 1.52 vs 1.48

RCI: .70 vs .68

RTN: 2.03 vs 2.02

SHW: 2.95 vs 3.18

STM: .41 vs .35

UNP: 1.53 vs 1.54

(reports after close, estimate provided):

INTC: .86

ISRG: 2.27

KLAC: 1.72

SBUX: .57

WDC: 3.77

Key Economic Reports

Initial jobless claims released at 8:30am EST: 233,000 (actual) vs. 240,000 (estimate)

December new home sales to be released at 10:00am EST: 680,000 (estimate)

December leading indicators to be released at 10:00am EST: +0.5% (estimate)

Happy trading!

Tom