Market Recap for Monday, February 12, 2018

Wall Street saw more gains on Monday, continuing the strength we saw late during the Friday session. Most of the strength, however, came during the morning session as the benchmark S&P 500 hit 2660, rising 130 points or approximately 5%, off the intraday low on Friday afternoon. That buying momentum did appear to slow Monday afternoon, though, so I'd like to see short-term gap support hold:

The close on Friday was just below 2620. If we fall below that level, we'll likely see the PPO drop beneath centerline support and short-term selling momentum resume. Instead, what I'd like to see going forward is consolidation between perhaps 2620-2670, and then see another breakout. That would suggest the market is growing more confident that a bottom is in. Failure to hold 2620 could result in a sequel to the movie we saw last Wednesday. If you recall, we had a strong recovery Tuesday afternoon, then saw continuation on Wednesday morning. After that, however, we began to drift lower and eventually fell back into another big selloff. Keep in mind that the Volatility Index ($VIX) is still at 25, a very high reading. Losing even short-term price support with VIX readings this high can trigger violent selling episodes. I'd love to explain how to manage risk in this environment, but managing risk is difficult when VIX levels are above 20, especially when they're in the 30s and 40s. Honestly, you just have to be willing to take on very high risks to trade on either side, long or short.

The close on Friday was just below 2620. If we fall below that level, we'll likely see the PPO drop beneath centerline support and short-term selling momentum resume. Instead, what I'd like to see going forward is consolidation between perhaps 2620-2670, and then see another breakout. That would suggest the market is growing more confident that a bottom is in. Failure to hold 2620 could result in a sequel to the movie we saw last Wednesday. If you recall, we had a strong recovery Tuesday afternoon, then saw continuation on Wednesday morning. After that, however, we began to drift lower and eventually fell back into another big selloff. Keep in mind that the Volatility Index ($VIX) is still at 25, a very high reading. Losing even short-term price support with VIX readings this high can trigger violent selling episodes. I'd love to explain how to manage risk in this environment, but managing risk is difficult when VIX levels are above 20, especially when they're in the 30s and 40s. Honestly, you just have to be willing to take on very high risks to trade on either side, long or short.

Materials (XLB, +2.02%) led Monday's action as steel ($DJUSST) and commodity chemicals ($DJUSCC) gained 2.93% and 2.76%, respectively. The DJUSST was particularly strong, closing at a 7 day high. There aren't too many industry groups that can boast that right now.

Technology (XLK, +1.79%) also performed well, as Apple (AAPL, +4.03%) led a computer hardware ($DJUSCR, +3.73%) rally.

Pre-Market Action

U.S. indices are preparing for a pullback at today's open with Dow Jones futures down approximately 100 points with roughly an hour to go before the opening bell.

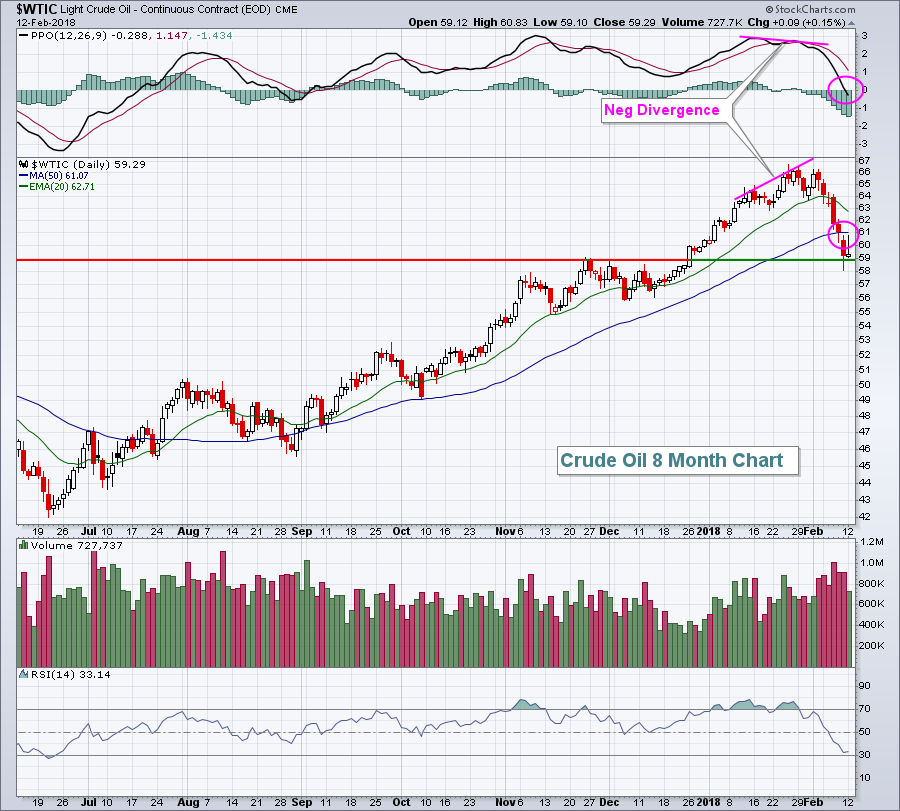

Asian markets were mostly higher overnight, while European markets are mixed this morning. Crude oil ($WTIC) has fallen back to test $59 per barrel again and that's a fairly important level technically:

Slowing price momentum became an issue for crude at the late-January high so we've seen crude pull back with global equity prices. But there's clear price support at 59 per barrel and the rising 20 week EMA (not reflected on the above daily chart) is currently at 58.60. Therefore, losing the 59 level would be a big deal technically and likely lead to another key test near 55 per barrel.

Slowing price momentum became an issue for crude at the late-January high so we've seen crude pull back with global equity prices. But there's clear price support at 59 per barrel and the rising 20 week EMA (not reflected on the above daily chart) is currently at 58.60. Therefore, losing the 59 level would be a big deal technically and likely lead to another key test near 55 per barrel.

Current Outlook

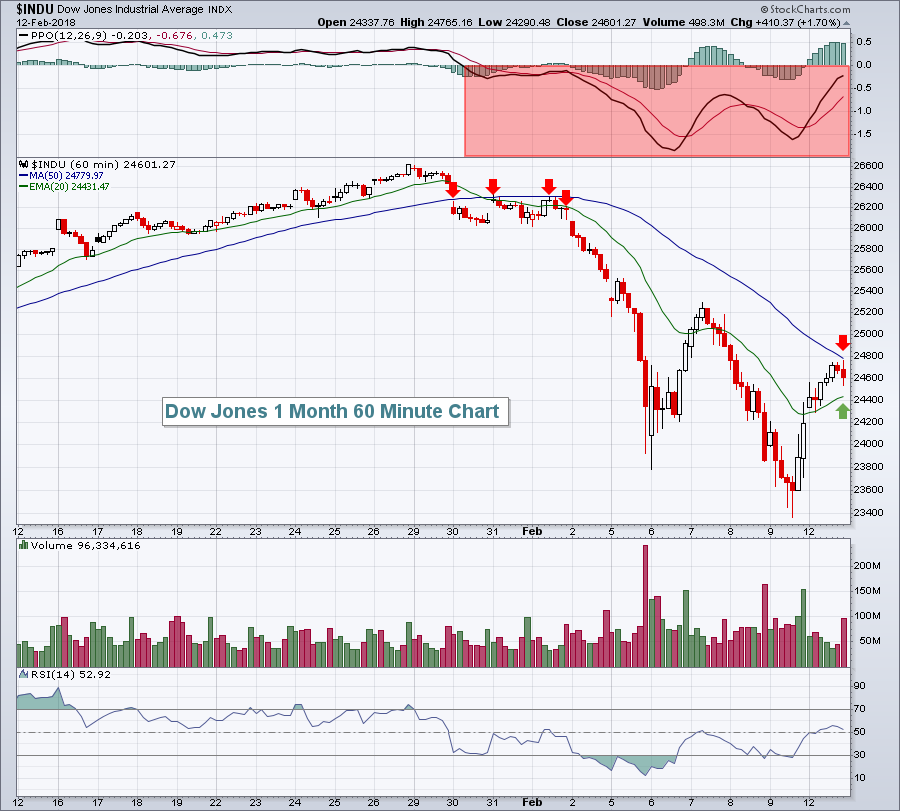

Since this selling episode began in late January, the Dow Jones ($DJI) has not been able to clear its 50 hour SMA. It's tested that moving average on several occasions, but with no success thus far. On Monday, the Dow's intraday high of 24,765 came very close once again as the 50 day SMA currently stands at 24,779. Take a look:

A short-term battle to watch will be overhead resistance at the 50 hour SMA and support at the now-rising 20 hour EMA. A sustained move through either would be a solid short-term indication of where prices are likely heading today. Currently, the PPO remains below the centerline and it's been that way since the bears took control of the action. Therefore, for now, I'd have to give the bears the short-term nod.

A short-term battle to watch will be overhead resistance at the 50 hour SMA and support at the now-rising 20 hour EMA. A sustained move through either would be a solid short-term indication of where prices are likely heading today. Currently, the PPO remains below the centerline and it's been that way since the bears took control of the action. Therefore, for now, I'd have to give the bears the short-term nod.

Sector/Industry Watch

Only one sector currently trades above its 50 day SMA - consumer discretionary (XLY). The XLY also has the highest SCTR at 93. No matter how you slice it, discretionary stocks have been the relative leader since exploding through triple top resistance near 92:

The selling, while scary, was waaaaay overdue with weekly RSI testing 90. Weekly RSI readings at 90 are very, very infrequent and indicated we needed a correction badly. Now that we've seen one, no one wants to buy. That'll likely lead to back and forth action for awhile, establishing bullish continuation patterns where we'll ultimately see new highs later in 2018. When? That's difficult to predict, but the key for me is that I'm remaining bullish until "under the surface" signals begin to tell me otherwise.

The selling, while scary, was waaaaay overdue with weekly RSI testing 90. Weekly RSI readings at 90 are very, very infrequent and indicated we needed a correction badly. Now that we've seen one, no one wants to buy. That'll likely lead to back and forth action for awhile, establishing bullish continuation patterns where we'll ultimately see new highs later in 2018. When? That's difficult to predict, but the key for me is that I'm remaining bullish until "under the surface" signals begin to tell me otherwise.

Historical Tendencies

December is clearly the best month for small cap stocks found on the Russell 2000 ($RUT). However, the best four consecutive month period for small caps has been February through May where the RUT has posted the following annualized returns since 1987:

February: +15.64%

March: +17.21%

April: +14.04%

May: +14.36%

The rapidly declining dollar since late 2016 has sent many investors to large cap, multinational companies that benefit from foreign profits that are translated into dollars during periods of a falling greenback. The U.S. Dollar Index ($USD), however, has hit very significant price and trendline support near 88 and a rise in the dollar from this level throughout 2018 could send investors flocking back towards small cap stocks.

Key Earnings Reports

(actual vs. estimate):

MLM: 1.88 vs 1.42

PEP: 1.31 vs 1.30

WB: .64 vs .58

(reports after close, estimate provided):

AMX: .14

BIDU: 2.05

MET: 1.10

OXY: .40

Key Economic Reports

None

Happy trading!

Tom