Market Recap for Friday, April 27, 2018

The news heading into Friday couldn't have been much better. The initial reading of Q1 GDP came in stronger than expected at 2.3% vs. 2.0%. We had blowout earnings from key leaders including Amazon.com (AMZN), Microsoft (MSFT) and Intel (INTC), yet the NASDAQ finished with a one point gain. The morning started with great promise as the NASDAQ surged 77 points at the opening bell, but as we've seen many times recently, the gains didn't stick. In fact, within 90 minutes of the opening bell, the NASDAQ found itself down 35 points - a complete and disappointing reversal. The final several hours saw consolidation more than anything.

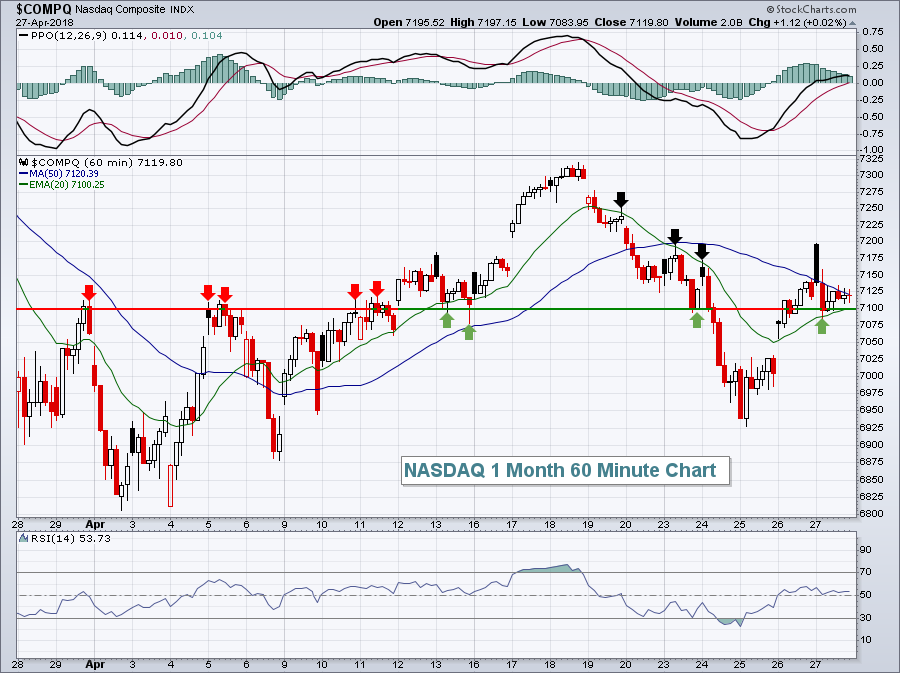

So what do we take away from this solid fundamental news, but tepid reaction? Well, the obvious answer is the U.S. stock market is continuing to consolidate on its daily charts. The S&P 500 has established very strong support at the 2581 double bottom and the late-January all-time high close of 2873 is the clear resistance level, although there are a few notable resistance areas to negotiate prior to reaching that 2873 peak. If you tend to watch rallies or declines unfold for confirmation and then chase, that strategy has most likely proven unsuccessful in this environment. I believe a better strategy is to follow the intraday charts for tradable trends. Currently, the NASDAQ appears to be trending higher, even though many were likely disappointed by Friday's action:

The red and green arrows mark resistance and support, respectively, near the 7100 area. So that's a key number to follow on an intraday basis. Also, the 20 hour EMA is now rising and was successfully defended by the bulls on Friday even though the action might initially be seen as disappointing. During the most recent downtrend, black arrows mark the 20 hour EMA as key resistance. Now that the trend has reversed, I'd look for the opposite - for the rising 20 hour EMA to hold as support. Failure to do so would be a short-term technical issue for the bulls.

The red and green arrows mark resistance and support, respectively, near the 7100 area. So that's a key number to follow on an intraday basis. Also, the 20 hour EMA is now rising and was successfully defended by the bulls on Friday even though the action might initially be seen as disappointing. During the most recent downtrend, black arrows mark the 20 hour EMA as key resistance. Now that the trend has reversed, I'd look for the opposite - for the rising 20 hour EMA to hold as support. Failure to do so would be a short-term technical issue for the bulls.

Overall, the Friday action was bifurcated with the S&P 500 and NASDAQ clinging to tiny gains at the close, while both the Dow Jones and Russell 2000 finished the session slightly into negative territory. Utilities (XLU, +1.02%) bounced as the 10 year treasury yield ($TNX) paused and fell back beneath the psychological 3.00% level, closing at 2.96%. Both areas of consumer stocks - staples (XLP, +0.53%) and discretionary (XLY, +0.45%) - performed well, most likely the result of the stronger-than-expected GDP number.

Energy (XLE, -1.02%) was easily the weakest sector as Exxon Mobil Corp (XOM) disappointed with its latest quarterly results, missing estimates. XOM is the largest holding of the XLE. Clearly, XOM's 3.80% decline on Friday weighed on the group.

Pre-Market Action

McDonalds (MCD) is set to challenge 3 month highs after posting quarterly results that were well in excess of Wall Street estimates. That strength, along with a couple merger announcements, is helping to lift U.S. futures this morning. With a little more than 30 minutes left to the opening bell, Dow Jones futures are higher by 124 points.

Gold ($GOLD) is continuing its recent decline, down another $9 to $1314 per ounce. $1300-$1310 is a key support zone to watch closely. The U.S. Dollar ($USD) is trading higher this morning and the recent climb in the greenback has put significant pressure on gold and other commodities.

Current Outlook

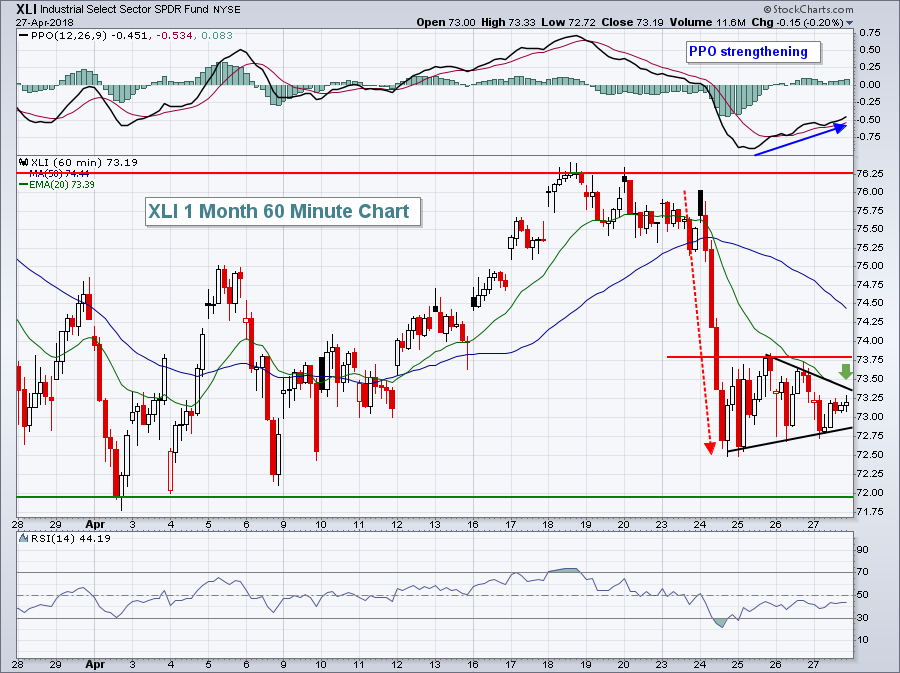

One area of the market that needs to turn around is industrials (XLI, -0.20%). Transports ($TRAN) were hit particularly hard on Tuesday of last week and that's kept some pressure on the group. The first step to strengthen the XLI technically is to reclaim its 20 hour EMA:

A move back above 73.80 would be a solid start to repairing the technical damage on the XLI's intraday chart.

A move back above 73.80 would be a solid start to repairing the technical damage on the XLI's intraday chart.

Sector/Industry Watch

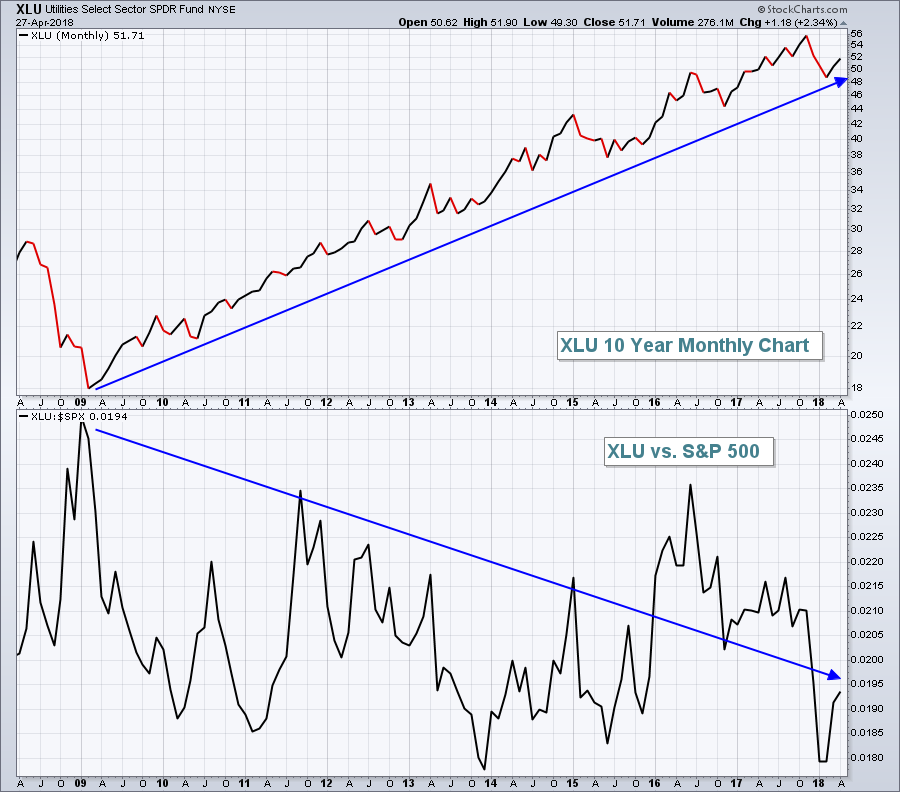

Wide participation is what I look for during bull markets. While I prefer to see leadership from aggressive groups as the S&P 500 marches to new highs, I also want to see participation from most areas of the stock market. Utilities (XLU) saw strength on Friday, which is fine. It's ok from defensive groups to have solid days and, in fact, I would expect the XLU to have a solid day when the 10 year treasury yield ($TNX) is declining, as it was on Friday. But from a big picture perspective, I want to see the XLU rising on an absolute basis, but declining relative to the S&P 500. Take a look at this longer-term chart of the XLU as an example:

Utilities moving higher isn't a concern. Utilities outperforming the benchmark S&P 500 during bull market advances can be. This is just one signal to be aware of and currently there are no issues whatsoever.

Utilities moving higher isn't a concern. Utilities outperforming the benchmark S&P 500 during bull market advances can be. This is just one signal to be aware of and currently there are no issues whatsoever.

Monday Setups

This is going to a very aggressive pick this week, but I'm willing to take a flier with Nektar Therapeutics (NKTR). NKTR ran from 25 in November to a high of 111 in March. It has since fallen back to 83.66 and I believe could see significant support in the low 80s. Just bear in mind that failure to hold 80 could result in another swift move lower. Here's the chart:

Perhaps the run to the upside on NKTR has ended. But NKTR is in the biotech ($DJUSBT) space and this group overall has been extremely weak. We finally began to see a bit of outperformance from biotechs late last week and, if that continues, NKTR could certainly benefit. A move higher to test the declining 20 day EMA is all I'd look for initially.

Perhaps the run to the upside on NKTR has ended. But NKTR is in the biotech ($DJUSBT) space and this group overall has been extremely weak. We finally began to see a bit of outperformance from biotechs late last week and, if that continues, NKTR could certainly benefit. A move higher to test the declining 20 day EMA is all I'd look for initially.

Historical Tendencies

This week is a solid week for U.S. equities historically. For instance, here are the annualized returns on the NASDAQ (since 1971) each day this week:

April 30 (today): +9.60%

May 1 (tomorrow): +102.43%

May 2 (Wednesday): +62.91%

May 3 (Thursday): -37.93%

May 4 (Friday): +37.20%

While May 5th falls on a Saturday this year, that day also has been very bullish over the years, rising at an annualized clip of +79.36%.

Key Earnings Reports

(actual vs. estimate):

AGN: 3.74 vs 3.36

CNA: 1.03 vs .90

EPD: .39 vs .38

FDC: .29 vs .26

L: .89 vs .78

MCD: 1.79 vs 1.67

PEG: .97 vs .98

(reports after close, estimate provided):

AKAM: .70

SBAC: .21

VNO: .88

Key Economic Reports

March personal income released at 8:30am EST: +0.3% (actual) vs. +0.4% (estimate)

March personal spending released at 8:30am EST: +0.4% (actual) vs. +0.4% (estimate)

April Chicago PMI to be released at 9:45am EST: 57.8 (estimate)

March pending home sales to be released at 10:00am EST: +1.0% (estimate)

Happy trading!

Tom