Market Recap for May 1, 2018

The Dow Jones led the early selling on Tuesday as traders were not impressed with quarterly earnings results from two pharma giants, Pfizer (PFE, -3.31%) and Merck (MRK, -1.51%). Both were down considerably more in the morning session, but rebounded to make their respective losses a bit more palatable. But despite the early weakness and the 6% spike in the Volatility Index ($VIX), the bulls were able to regain control of the action in the afternoon session, leading to gains across the S&P 500, NASDAQ and Russell 2000. The Dow Jones finished in negative territory, dropping 64 points, but nearly 300 points off its intraday low.

The reversal was felt most in technology (XLK, +1.25%) as computer hardware ($DJUSCR, +2.08%) and semiconductors ($DJUSSC, +1.88%) led this aggressive sector. The former no doubt was anticipating strong quarterly results from Apple (AAPL) after the bell and the tech giant did not disappoint. AAPL is up 4.7% in pre-market action at last check.

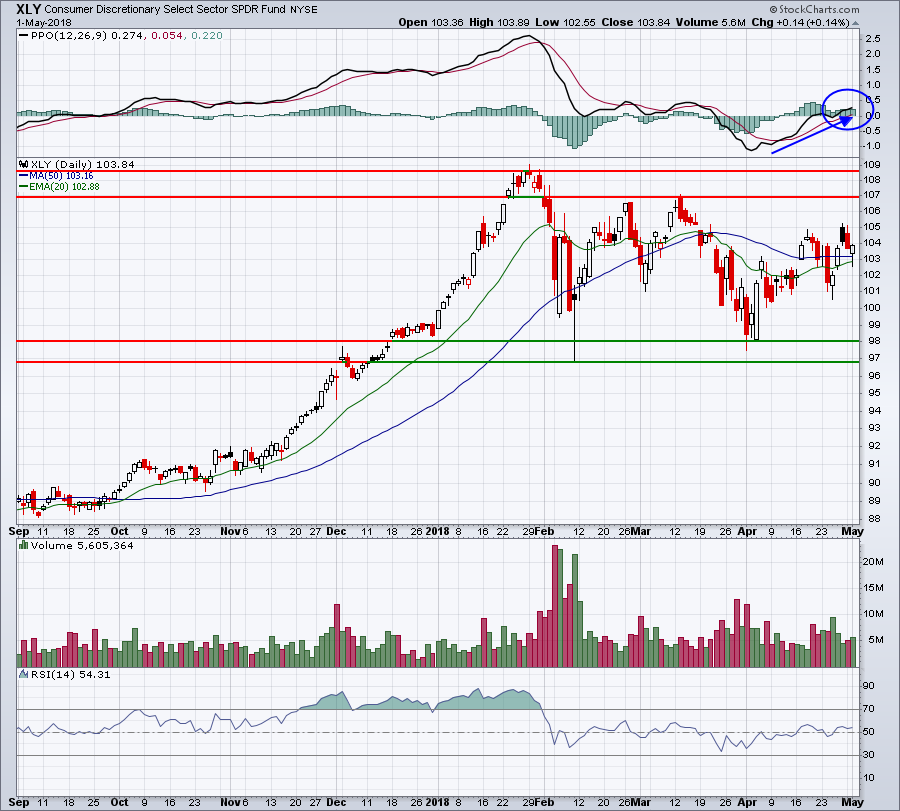

Consumer discretionary (XLY, +0.14%) was a distant second place on the sector leaderboard, held back by a very weak clothing & accessories industry ($DJUSCF, -2.88%). Tapestry (TPR) reported solid quarterly results in terms of revenues and earnings, but dropped an unsuspecting guidance bomb on traders, suggesting an earnings miss in its upcoming quarter. That was felt throughout much of the industry, notably Michael Kors (KORS, -2.95%), which had been trading near 3 year highs. There's been a ton of consolidation and rotation throughout most parts of the U.S. stock market the past three months and that's perfectly depicted in the XLY chart below:

The PPO is strengthening and we've seen a break above PPO centerline resistance so it'll be interesting to see if this can carry the XLY above recent price resistance. The 107-109 zone figures to be difficult overhead resistance.

The PPO is strengthening and we've seen a break above PPO centerline resistance so it'll be interesting to see if this can carry the XLY above recent price resistance. The 107-109 zone figures to be difficult overhead resistance.

Pre-Market Action

Apple (AAPL) reported solid quarterly earnings after the bell on Tuesday. In addition, the April ADP employment report hit the wires at 8:15am EST and was stronger than expected. Nonetheless, futures are showing that traders are not overly impressed with Dow Jones futures (-33) pointing to a lower open. The NASDAQ is likely to fare much better from the AAPL report.

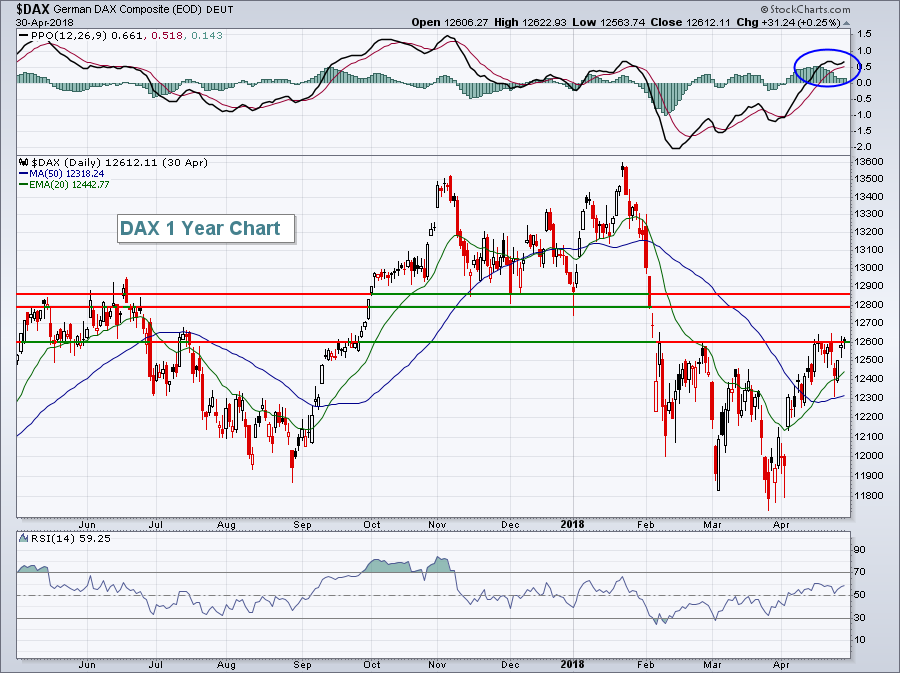

Overnight, Asian markets were mostly lower, but in an important development, the German DAX ($DAX) is higher by 160 points, or +1.26%, at last check and that's clearly above its recent reaction highs:

The above chart does not reflect the big gain from this morning. Instead, it only reflects price action through yesterday's close. Still, that PPO has been strengthening and will only be bolstered by the strong action today. There remain significant overhead resistance levels for the DAX, but one big one appears to be eliminated today, unless the DAX weakens significantly during the second half of its session.

The above chart does not reflect the big gain from this morning. Instead, it only reflects price action through yesterday's close. Still, that PPO has been strengthening and will only be bolstered by the strong action today. There remain significant overhead resistance levels for the DAX, but one big one appears to be eliminated today, unless the DAX weakens significantly during the second half of its session.

Current Outlook

Consolidation in the market has definitely been felt in transportation stocks ($TRAN). One signal of health in the stock market is to look at the Dow Jones Transports vs. the Dow Jones Utilities ($TRAN:$UTIL). A rising ratio to accompany a strengthening S&P 500 is generally a very bullish sign and suggests the rally is sustainable. During periods of consolidation and rotation, however, we often see this ratio consolidate as well. That's exactly what we've seen since mid-January:

One signal that the prior uptrend is likely resuming would be a breakout of the descending triangle on the S&P 500 accompanied by a breakout in the TRAN:UTIL relative downtrend line. Currently, this relative ratio is set up in what could be a relative double bottom, making a relative breakout more significant in my view.

One signal that the prior uptrend is likely resuming would be a breakout of the descending triangle on the S&P 500 accompanied by a breakout in the TRAN:UTIL relative downtrend line. Currently, this relative ratio is set up in what could be a relative double bottom, making a relative breakout more significant in my view.

Sector/Industry Watch

Yesterday, I discussed truckers ($DJUSTK). Above in the Current Outlook section I discussed transports as they relate to utilities. Let's keep that transports theme intact and check out the railroads ($DJUSRR):

As railroads topped in January, they did so with an ugly negative divergence in play. That resulted in a steep drop - all the way down to test its breakout level of 1675. But the more intermediate-term uptrend held and continues to hold, a very good sign for this group. Keep in mind that performance of railroads should be tied fairly closely to U.S. economic expectations. I still see no breakdown here and so I will continue to maintain a very bullish stance, despite the ongoing consolidation. A breakout above 1900 on a closing basis would be quite welcome for the bulls. The green arrow above shows that the 20 day EMA is holding for now on a short-term basis and, as long as that continues, a breakout should be the expectation.

As railroads topped in January, they did so with an ugly negative divergence in play. That resulted in a steep drop - all the way down to test its breakout level of 1675. But the more intermediate-term uptrend held and continues to hold, a very good sign for this group. Keep in mind that performance of railroads should be tied fairly closely to U.S. economic expectations. I still see no breakdown here and so I will continue to maintain a very bullish stance, despite the ongoing consolidation. A breakout above 1900 on a closing basis would be quite welcome for the bulls. The green arrow above shows that the 20 day EMA is holding for now on a short-term basis and, as long as that continues, a breakout should be the expectation.

Historical Tendencies

I ran a poll during a recent MarketWatchers LIVE show, asking the audience to vote on which day of the week has been the most bullish on the S&P 500 since 1950. The winner, according to the poll, was Tuesday. Unfortunately, Tuesday was not the right choice. Wednesdays have produced annualized returns that more than double the S&P 500's average annual return of 9%. Mondays have been, by far, the worst day of the week, posting annualized losses of approximately 15% over the same period. That's 24 percentage points beneath that 9% average rate, something to keep in mind. In particular, the Mondays that follow monthly options expiration have very bearish tendencies.

Key Earnings Reports

(actual vs. estimate):

ADP: 1.52 vs 1.44

APTV: 1.29 vs 1.20

CVS: 1.48 vs 1.39

EL: 1.17 vs 1.07

EXC: .96 vs .93

HRS: 1.67 vs 1.62

HUM: 3.36 vs 3.21

MA: 1.50 vs 1.26

SO: .88 vs .82

YUM: .90 vs .68

ZTS: .75 vs .70

(reports after close, estimate provided):

AIG: 1.24

CLR: .60

EQIX: 4.94

ESRX: 1.76

MET: 1.17

MFC: .49

NXPI: 1.71

PRU: 2.99

PXD: 1.51

S: (.06)

SPOT: (.33)

SQ: .05

TSLA: (3.37)

WPZ: .41

Key Economic Reports

April ADP employment report released at 8:15am EST: 204,000 (actual) vs. 190,000 (estimate)

FOMC policy announcement to be released at 2:00pm EST

Happy trading!

Tom