Market Recap for Wednesday, September 5, 2018

There were a couple things that stood out to me regarding Wednesday's action. First, the recovery off the intraday low wasn't insignificant. However, the stocks driving most of the recovery were in defensive areas. Utilities (XLU, +1.40%) and consumer staples (XLP, +1.15%) were the only two sectors to gain more than 1% and both are defensive groups. Second, while the rebound in our major indices was fairly strong after heavy first hour selling, the NASDAQ's rebound was not strong at all and the reason was clear. Technology (XLK, -1.25%) and consumer discretionary (XLY, -1.08%) were the only sectors to see much selling at all and both were down more than 1%. So there seemed to be quite a bit of rotation from aggressive areas to defensive areas. Keep in mind that both the XLK and XLY recently spiked into all-time record high territory so profit taking is to be expected. I wouldn't jump off the nearest bridge because these two groups underperformed for a day, but continuation of this trend during the bearish month of September is worth monitoring.

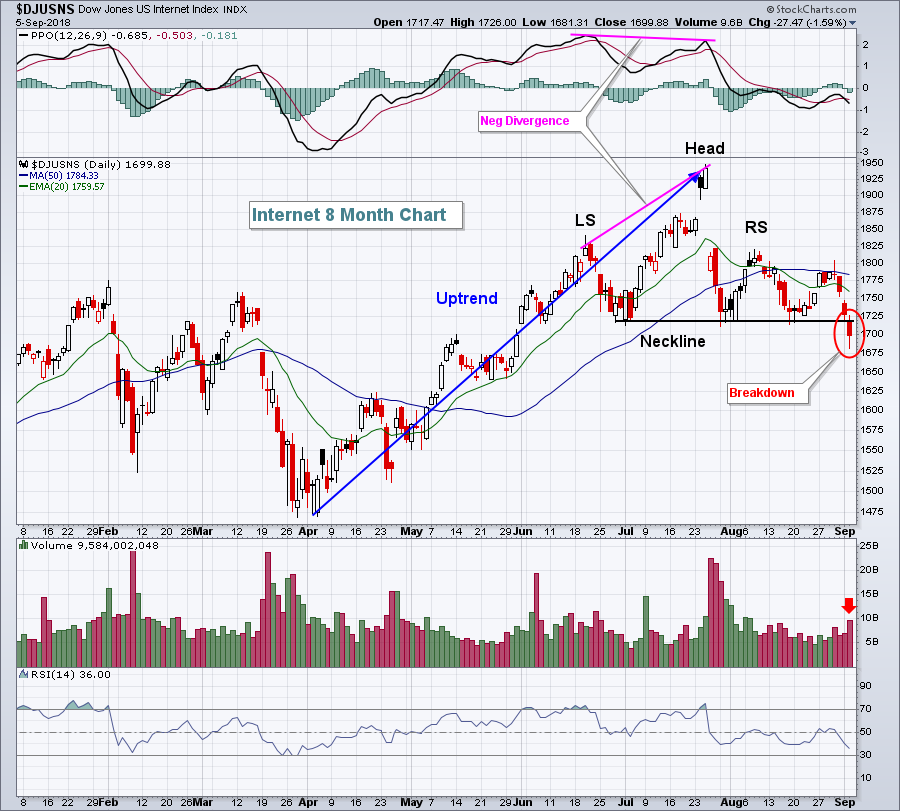

Software ($DJUSSW) and internet ($DJUSNS) were the primary reasons that technology was so weak. And there are reasons to fear further selling in both industry groups. Let's start with the DJUSNS:

Those who are bearish will no doubt point to this confirmed topping structure in a key area of technology. While I am not a believer that internet weakness will bring the entire market down (because other areas like semiconductors could step up - see Sector/Industry Watch below), I do share the bearish sentiment on this group currently. In fact, I'd be extremely careful owning any internet stock right now. (Disclosure: I do own GOOGL currently and will sell if Wednesday's intraday low is violated).

Those who are bearish will no doubt point to this confirmed topping structure in a key area of technology. While I am not a believer that internet weakness will bring the entire market down (because other areas like semiconductors could step up - see Sector/Industry Watch below), I do share the bearish sentiment on this group currently. In fact, I'd be extremely careful owning any internet stock right now. (Disclosure: I do own GOOGL currently and will sell if Wednesday's intraday low is violated).

Facebook (FB) broke down beneath its post-earnings low and will likely move short-term to test gap support at 160, but eventually I see FB testing 150 to establish the right side of a bearish long-term head & shoulders neckline. FB is one of my least favorite stocks in the market right now as market participants scramble to figure out what the company's true valuation should be after a substantial lowering of their future operating margins. I know this might sound crazy, but I will not be surprised if FB is a $100 stock sometime in 2019. Personally, I believe it's an isolated occurrence in technology and many other very solid companies will hold up the NASDAQ. Anyhow, we'll see.

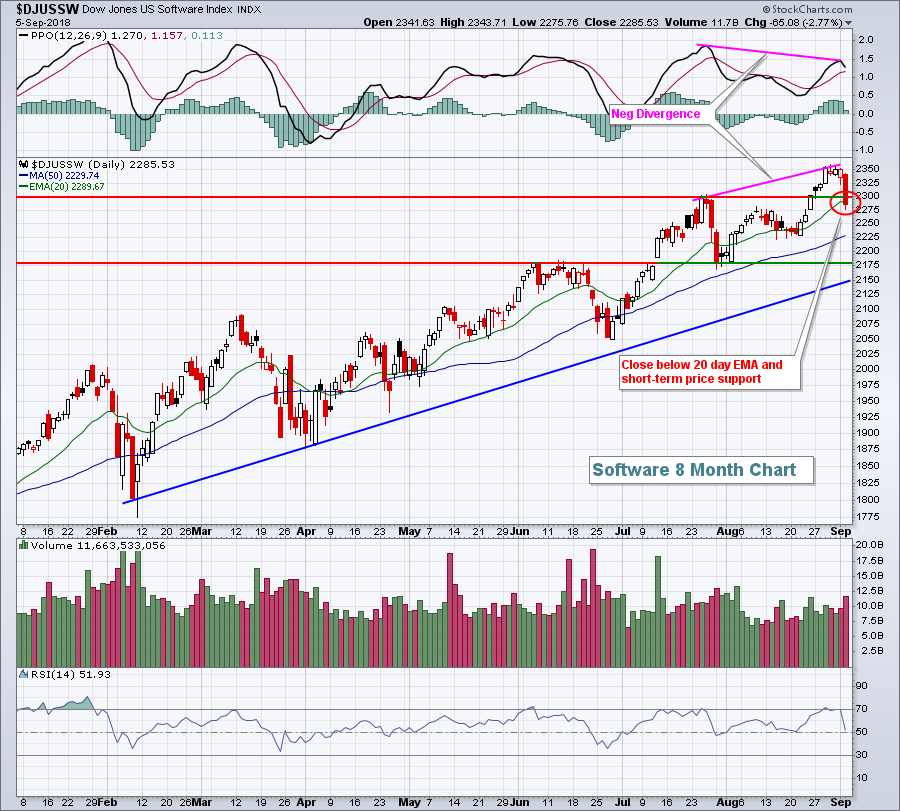

Then there was software yesterday, which lost rising 20 day EMA and price support with a negative divergence in play:

There's likely to be more short-term weakness in software, but if the group approaches its 50 day SMA or possibly moves beneath it, I expect the reward to risk to be extremely bullish for this group as we head into the fourth quarter. This is a group to watch for sure.

There's likely to be more short-term weakness in software, but if the group approaches its 50 day SMA or possibly moves beneath it, I expect the reward to risk to be extremely bullish for this group as we head into the fourth quarter. This is a group to watch for sure.

Pre-Market Action

Asian markets were weak overnight, but Europe appears to have weathered the short-term storm with mixed action. Thus far, the German DAX ($DAX) is holding onto psychological support at the 12000 level. Despite a weaker-than-expected ADP employment report this morning, Dow Jones futures are up 31 points with 30 minutes left to the opening bell.

Current Outlook

There is no disputing that technology (XLK) has been a primary driver behind the almost decade-long bull market. So when the sector begins to show any weakness whatsoever, it can cause short-term technical damage to the overall market. While the weakness in the XLK has been limited thus far to a 20 day EMA test on its daily chart, we should respect the near-term support on the 60 minute chart:

Trendline support is very clear and intersects somewhere near the 74.25 level. Price and gap support also reside at that 74.25 level. On the daily chart, the 20 day EMA is currently at 74.14. A break below this area wouldn't be long-term cause for concern, but knowing that September is historically bearish, the last thing the bulls want to see is a leader like the XLK failing to hold a short-term support zone. In my opinion, that 74.00 (where we bounced yesterday) to 74.25 support zone is big from a short-term trading perspective.

Trendline support is very clear and intersects somewhere near the 74.25 level. Price and gap support also reside at that 74.25 level. On the daily chart, the 20 day EMA is currently at 74.14. A break below this area wouldn't be long-term cause for concern, but knowing that September is historically bearish, the last thing the bulls want to see is a leader like the XLK failing to hold a short-term support zone. In my opinion, that 74.00 (where we bounced yesterday) to 74.25 support zone is big from a short-term trading perspective.

Sector/Industry Watch

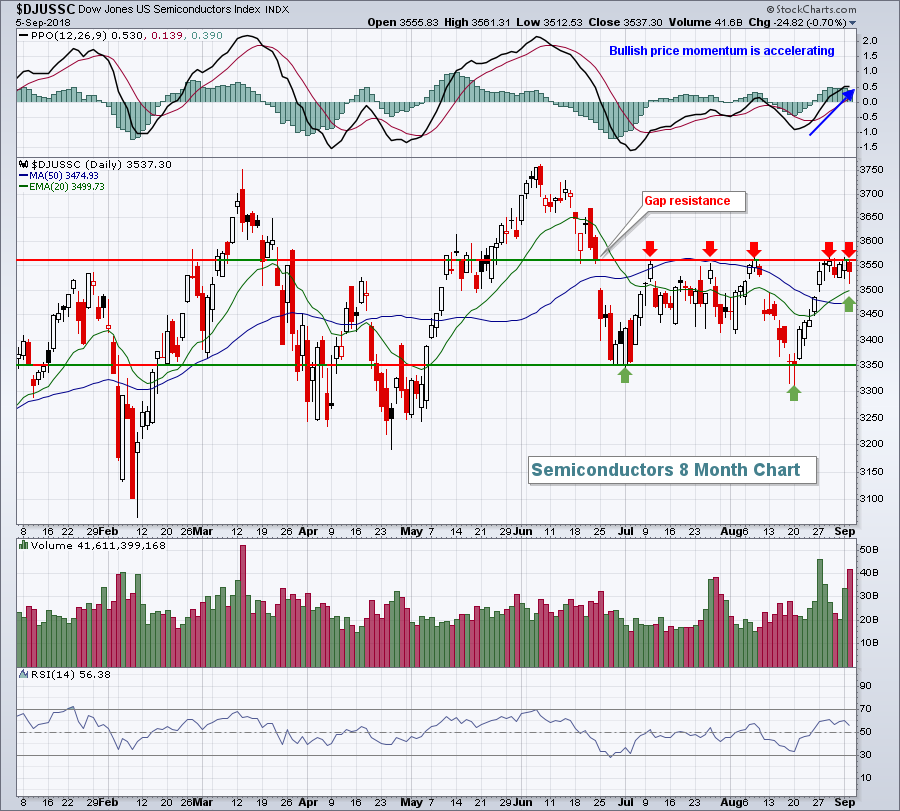

Semiconductors ($DJUSSC) remain a very interesting industry to watch. Yesterday, technology took it on the chin, but semiconductors performed quite well on a relative basis. Recently, the opposite has been true. Technology has been a leader and the DJUSSC has struggled on a relative basis, failing to break above multi-month price resistance. If the internet and software groups continue to struggle, it'll be important to see some of that technology money rotate into semis. Here's where the group currently stands technically:

The battle lines have been drawn. Gap resistance is now quite formidable with 5 attempts and 5 failures to clear the this hurdle. We are looking for a confirmed heavy volume breakout above 3562. The PPO is rising and looks as strong as at any point over the past 2-3 months, so holding onto support at the rising 20 day EMA, currently at 3500 is paramount in the short-term. Failure to do so would likely result in yet another test of price support near 3350, not a very good scenario for technology bulls.

The battle lines have been drawn. Gap resistance is now quite formidable with 5 attempts and 5 failures to clear the this hurdle. We are looking for a confirmed heavy volume breakout above 3562. The PPO is rising and looks as strong as at any point over the past 2-3 months, so holding onto support at the rising 20 day EMA, currently at 3500 is paramount in the short-term. Failure to do so would likely result in yet another test of price support near 3350, not a very good scenario for technology bulls.

Historical Tendencies

I'd be hard-pressed to find a better performing stock than Advanced Micro Devices (AMD). It's fresh off a parabolic-type rise, doubling in price in just the past two months. But there's reason for caution as we trade throughout September. First, AMD is very overbought with a daily RSI of 87 and a weekly RSI of 88. So a pullback is warranted and deserved. Second, history is not on the side of AMD bulls. Over the past two decades, AMD has fallen during the month of September roughly two out of every three years and its average September return over this span has been -4.8%. Only July's -5.3% average return has been worse.

Key Earnings Reports

(actual vs. estimate):

DCI: .58 vs .58

NAV: 1.19 vs .93

(reports after close, estimate provided):

AVGO: 4.83

FIVE: .38

MRVL: .34

OKTA: (.20)

PANW: 1.17

Key Economic Reports

August ADP employment report released at 8:15am EST: 163,000 (actual) vs. 182,000 (estimate)

Initial jobless claims released at 8:30am EST: 203,000 (actual) vs. 213,000 (estimate)

Q2 productivity released at 8:30am EST: +2.9% (actual) vs. +3.0% (estimate)

August PMI services to be released at 9:45am EST: 55.2 (estimate)

July factory orders to be released at 10:00am EST: -0.7% (estimate)

August ISM non-manufacturing index to be released at 10:00am EST: 56.8 (estimate)

Happy trading!

Tom