Market Recap for Wednesday, December 5, 2018

The U.S. stock market was closed.

Pre-Market Action

U.S. futures look set to continue Tuesday's rout. The 10 year treasury yield ($TNX) is lower by 3 basis points to 2.89% as money seeks out safety in the defensive bond market. Crude oil ($WTIC) is down 2.76% at last check as it looks poised to retest the $50 per barrel level.

Asian markets were clobbered overnight, with Hong Kong's Hang Seng Index ($HSI, -2.47%) leading the charge to the downside. There's no escaping the selling as European indices are all down more than 2%. That's led to further selling here in the U.S. in pre-market action as the Dow Jones futures are currently down 369 points with an hour left to the opening bell.

Current Outlook

The line separating this correction from a bear market, in my opinion, is at the S&P 500's February closing support at 2582. There's an intraday price support at 2532 worth watching as well. Transports ($TRAN) is a key area to watch as well as the TRAN can provide us significant clues about economic expectations. Here's what I'd keep an eye on with further stock market weakness:

On the S&P 500, we may challenge the October/November price low today, but the bigger support level was established at the February/April low.

On the S&P 500, we may challenge the October/November price low today, but the bigger support level was established at the February/April low.

Sector/Industry Watch

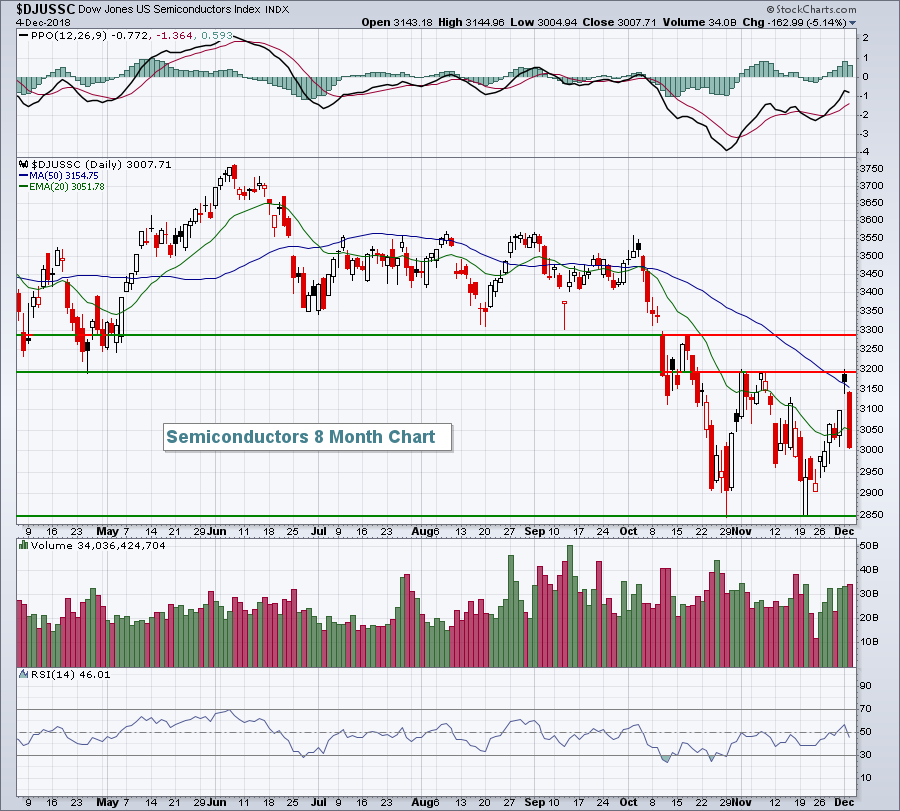

On Tuesday, I suggested that semiconductors ($DJUSSC) would be a group worth watching as they had reached a key area of overhead resistance. I reasoned that their direction would have a big impact on not only technology stocks, but also on the NASDAQ. Here's a reprint of that chart with Tuesday's bearish action quite obvious:

The bears made a bold statement at this resistance level. The DJUSSC is trying to absorb two big blows. The first is what appears to be a global economic slowdown and the second is the U.S.-China trade war. We could see a key test of price support close to 2850 as soon as today given the weak futures.

The bears made a bold statement at this resistance level. The DJUSSC is trying to absorb two big blows. The first is what appears to be a global economic slowdown and the second is the U.S.-China trade war. We could see a key test of price support close to 2850 as soon as today given the weak futures.

Historical Tendencies

The strongest part of December historically is during the final 10 days or so. From December 21st through December 31st, the NASDAQ has produced annualized returns of +62.82% since 1971.

Key Earnings Reports

(actual vs. estimate):

KR: .48 vs .43

(reports after close, estimate provided):

AVGO: 5.58

COO: 2.96

DOCU: (.02)

LULU: .69

ULTA: 2.16

Key Economic Reports

November ADP employment report released at 8:15am EST: 179,000 (actual) vs. 175,000 (estimate)

Initial jobless claims released at 8:30am EST: 231,000 (actual) vs. 225,000 (estimate)

Q3 productivity released at 8:30am EST: 2.3% (actual) vs. 2.3% (estimate)

November PMI services index to be released at 9:45am EST: 54.4 (estimate)

October factory orders to be released at 10:00am EST: -2.0% (estimate)

ISM non-manufacturing index to be released at 10:00am EST: 59.0 (estimate)

Happy trading!

Tom