Market Recap for Thursday, February 14, 2019

Real estate (XLRE, +0.38%) and communications services (XLC, +0.37%) were the leaders yesterday as Wall Street staged a rally attempt after dealing with an early blow - a very weak December retail sales report. There's one thing everyone should keep in mind though - the stock market looks ahead and not in the rear view mirror and that was on full display yesterday. The headline news created a stir at the open, but buyers returned quickly as the U.S. stock market has been sending a signal that the second half of 2019 will be better than the first half. Our major indices finished the day in bifurcated fashion with leadership from the NASDAQ (+0.09%) and Russell 2000 (+0.14%).

Most retailers were down on Thursday, but the best retail area of late has been specialty retail ($DJUSRS, +1.07%) and that was evident once again. The truly poor areas on Thursday were the financials sector (XLF, -1.22%) and consumer staples (XLP, -1.12%). The former saw selling as a result of a rapidly declining 10 year treasury yield ($TNX), which fell 5 basis points to 2.66% and was down even further early in Thursday's session. The bond market reacted much more negatively to the poor December retail sales report. The falling TNX remains the stock market's biggest worry in my opinion as treasury yields tend to fall in anticipation of a weakening economy.

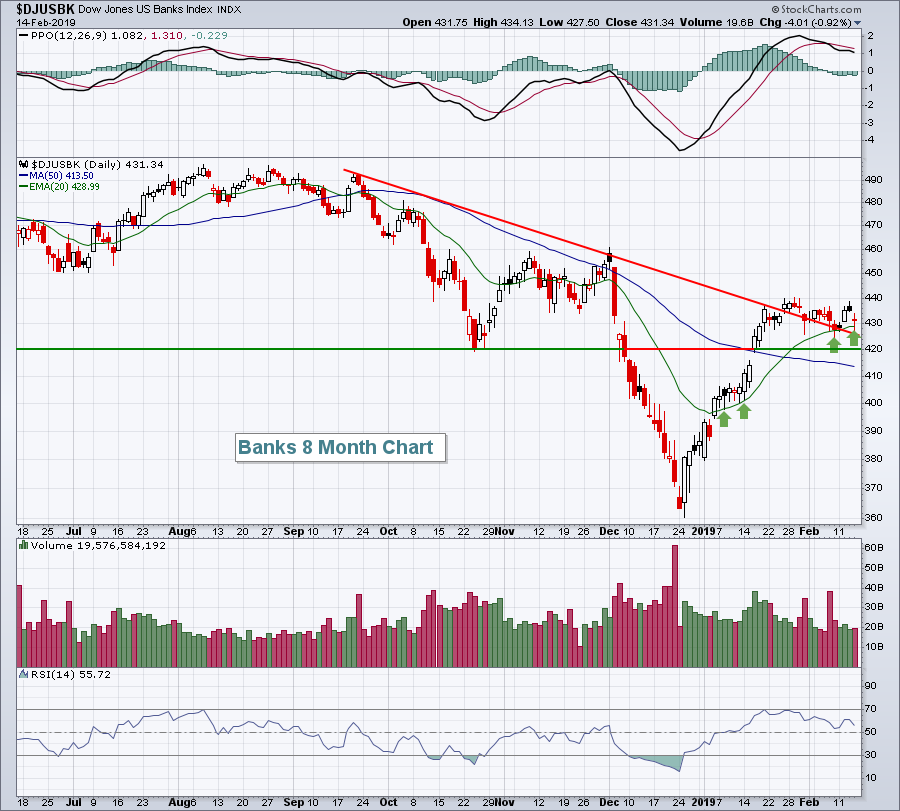

Banks ($DJUSBK, -0.92%) typically struggle with declining treasury yields as that can result in narrowing interest margins, a key component obviously to a bank's earnings. While the DJUSBK was in decline yesterday, it's not a problem technically:

The downtrend line has been broken, a technical positive, and the rising 20 day EMA continues to provide key technical support, another bullish development. I wouldn't worry too much about banks unless the 420 area is lost. At that point, the bears would begin to regain the technical advantage in the near-term.

The downtrend line has been broken, a technical positive, and the rising 20 day EMA continues to provide key technical support, another bullish development. I wouldn't worry too much about banks unless the 420 area is lost. At that point, the bears would begin to regain the technical advantage in the near-term.

Pre-Market Action

The 10 year treasury yield ($TNX) is up two basis points to 2.68% this morning. Crude oil ($WTIC) is up just under 1% to approach $55 per barrel.

U.S. futures are on the rise once gain, this time with Dow Jones futures up 72 points with roughly 30 minutes left to the opening bell.

Current Outlook

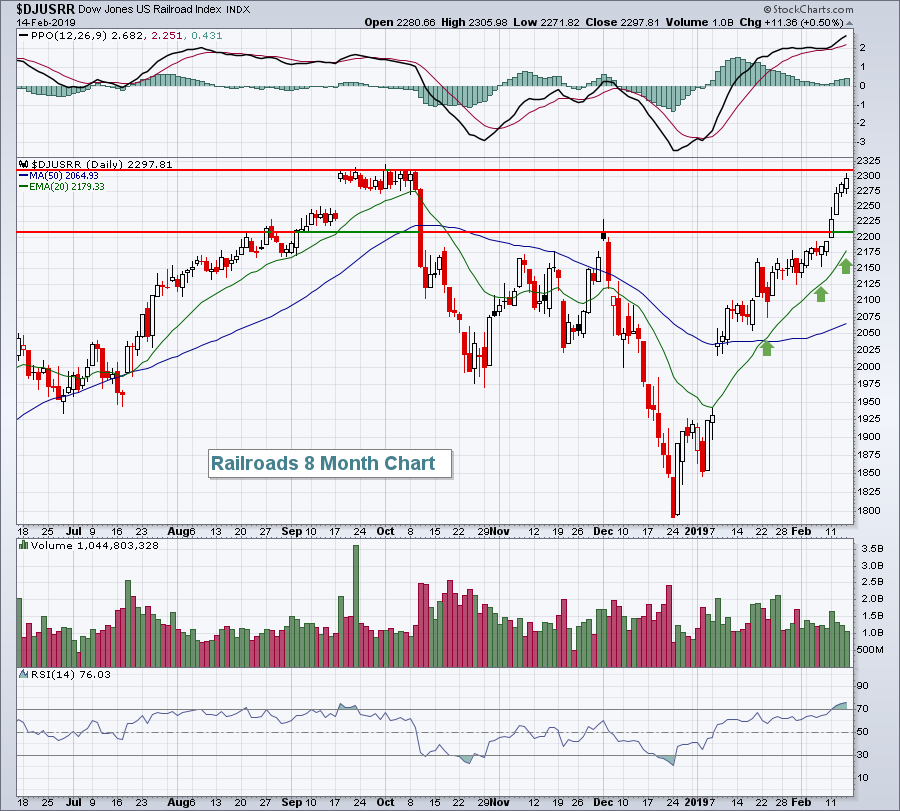

Railroads ($DJUSRR, +0.50%) are a proxy for the U.S. economy and they are on the verge of a significant breakout. Check it out:

It wouldn't be a bad thing to pause at overhead resistance. If the DJUSRR does take a break, look to price support just above 2200, along with rising 20 day EMA support (green arrows), as key support levels.

It wouldn't be a bad thing to pause at overhead resistance. If the DJUSRR does take a break, look to price support just above 2200, along with rising 20 day EMA support (green arrows), as key support levels.

Sector/Industry Watch

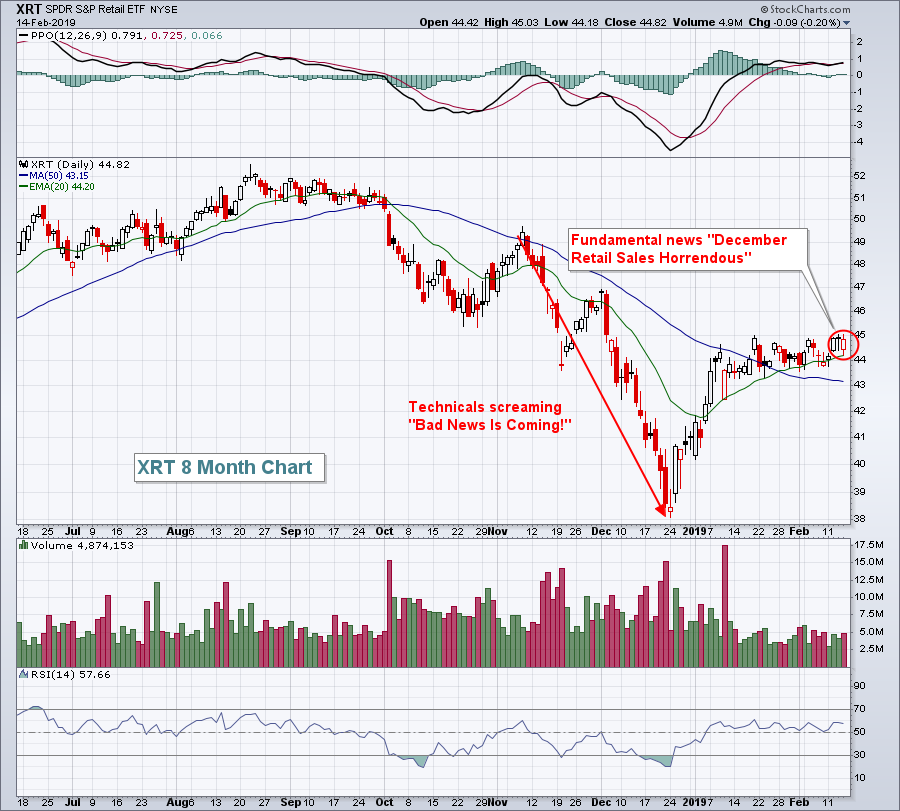

Retail stocks (XRT, -0.09%) held up quite well despite the horrid December retail sales report that was released Thursday morning. The message being sent is that the bad news had already been priced in during the Q4 selloff. Technicals precede fundamentals and the following chart illustrates this concept perfectly:

The headline news most definitely had an impact on U.S. futures Thursday morning and created a bit of early selling, but there were plenty of buyers to scoop up retail stocks. The rising 20 day EMA held beautifully as technical conditions here strengthen despite the awful fundamental report.

The headline news most definitely had an impact on U.S. futures Thursday morning and created a bit of early selling, but there were plenty of buyers to scoop up retail stocks. The rising 20 day EMA held beautifully as technical conditions here strengthen despite the awful fundamental report.

If you were bewildered by the huge miss in December retail sales (-1.2% actual vs +0.1% estimate) and the ho-hum response, I'd encourage you to turn CNBC off and turn StockCharts TV on. Seriously, CNBC is interested in ratings, saying whatever sells with little regard for your overall financial future. StockCharts TV will help you effectively manage your investments/trading to build a better retirement/future. Join me at noon EST every day the market is open for MarketWatchers LIVE - 90 minutes of the best technical analysis information available FOR FREE! CLICK HERE for MarketWatchers LIVE and be sure to tune in at noon.

Special Event

I'm really excited about joining John Hopkins, President of EarningsBeats.com on Tuesday, February 19th at 4:30pm EST for my "Top 10 Picks" webinar. These picks will be coming from my Strong Earnings ChartList. I did a similar webinar on November 19, 2018 and the 10 picks averaged gaining 17% through last Friday. The benchmark S&P 500 gained less than 1% over that same period.

Many of you asked and received a free copy of my Strong Earnings ChartList last September to sample the types of companies I trade. Well, there's even better news! I've asked John and he's agreed to share EarningsBeats.com's Strong Earnings and Weak Earnings ChartLists for an entire quarter of ChartLists for a nominal price! This is the first time that EarningsBeats.com has provided ChartLists for 90 days for a trial price. If you trade individual stocks and would like to experience these ChartLists for a full 90 days, I'd highly recommend you checking out this offer. The ChartLists are updated every 2-3 weeks. Each time it's updated during your 90 day trial, you'll receive a fresh copy of annotated charts of Wall Street's best (and worst for those who like to short) fundamental companies. It includes a seat to the Tuesday event as well where I'll unveil my latest 10 picks for the next 90 days. :-)

CLICK HERE to register.

Historical Tendencies

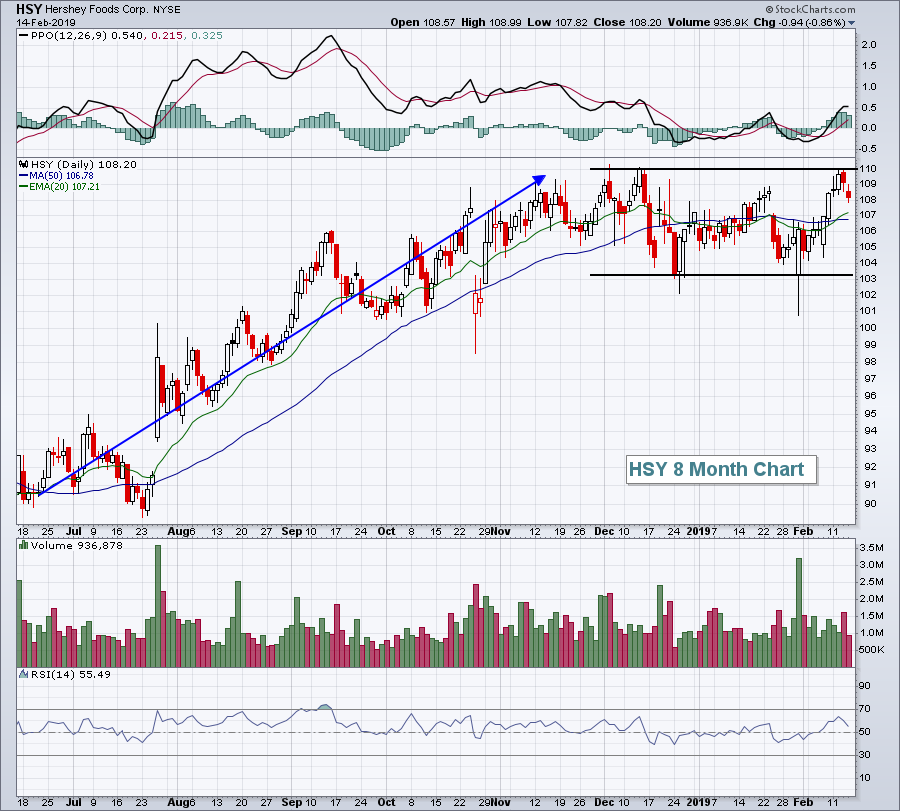

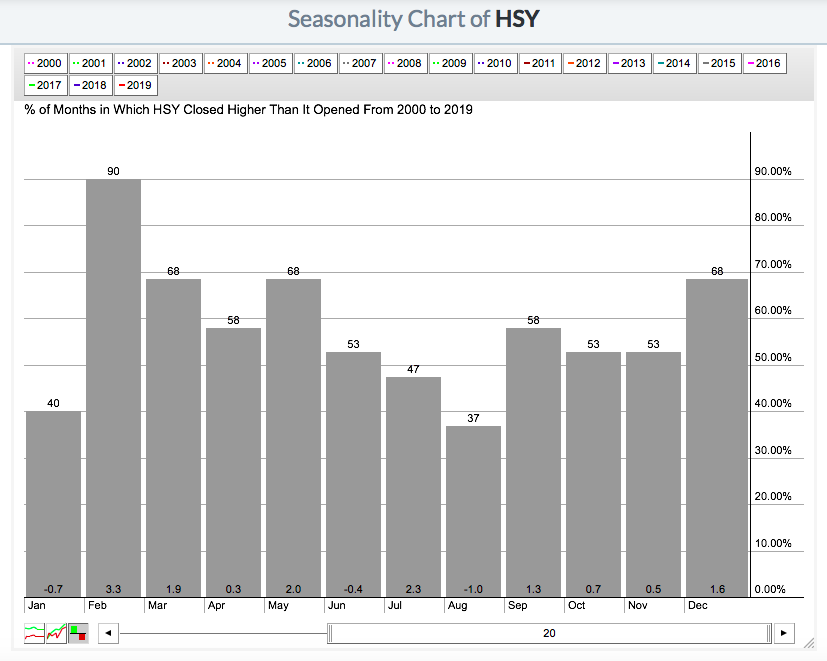

February is home to Valentine's Day....and apparently chocolate. Check out the rally attempt in Hershey's (HSY) thus far in February:

The February strength in 2019 doesn't appear to be a coincidence. Here's the HSY seasonality chart:

The February strength in 2019 doesn't appear to be a coincidence. Here's the HSY seasonality chart:

HSY has moved higher 18 of the last 20 Februarys (90%) and has averaged gaining 3.3% during the month over that span. February is definitely the season for chocolate lovers.

HSY has moved higher 18 of the last 20 Februarys (90%) and has averaged gaining 3.3% during the month over that span. February is definitely the season for chocolate lovers.

Key Earnings Reports

(actual vs. estimate):

DE: 1.54 vs 1.80

ENB: .45 - estimate, awaiting results

FTS: .42 vs .46

MCO: 1.63 vs 1.71

NWL: .71 vs .41

PEP: .49 vs .49

RBS: .06 vs .15

WBC: 2.13 vs 1.99

YNDX: .30 vs .32

Key Economic Reports

February empire state manufacturing survey released at 8:30am EST: 8.8 (actual) vs. 7.6 (estimate)

January industrial production to be released at 9:15am EST: +0.1% (estimate)

January capacity utilization to be released at 9:15am EST: 78.8% (estimate)

February consumer sentiment to be released at 10:00am EST: 93.0 (estimate)

Happy trading!

Tom