Market Recap for Tuesday, May 28, 2019

U.S. stocks jumped at the open, but then ran into sellers throughout the session. After gapping down at the open on Thursday, it's been difficult for the S&P 500 to clear the low 2840s and yesterday's selling began as soon as we touched that level:

There was clearly a stream of afternoon sellers with the closing result another test of important price support at 2800:

There was clearly a stream of afternoon sellers with the closing result another test of important price support at 2800:

The daily PPO is below centerline support and accelerating low, volume is increasing, and the RSI is now at 37. The RSI typically holds 40 support during uptrends. So the cards here appear to be stacked against the bulls. But we don't want to lose sight of the weekly chart because a rally by Friday's close could print a successful test of the longer-term rising 20 week EMA:

The daily PPO is below centerline support and accelerating low, volume is increasing, and the RSI is now at 37. The RSI typically holds 40 support during uptrends. So the cards here appear to be stacked against the bulls. But we don't want to lose sight of the weekly chart because a rally by Friday's close could print a successful test of the longer-term rising 20 week EMA:

I showed these charts yesterday, but it won't hurt to repeat them. If we print an intraweek low well beneath the 20 week EMA and manage to close back above it by Friday, that would be a very bullish development in my opinion. Failure to do so, however, opens up more possibilities to the downside. This will be a very important weekly candle.

I showed these charts yesterday, but it won't hurt to repeat them. If we print an intraweek low well beneath the 20 week EMA and manage to close back above it by Friday, that would be a very bullish development in my opinion. Failure to do so, however, opens up more possibilities to the downside. This will be a very important weekly candle.

Communication services (XLC, +0.44%) was the only sector to finish yesterday in positive territory as internet stocks ($DJUSNS, +0.61%) led on a relative basis. If there was a silver lining to Tuesday's selling, it was that three defensive sectors - utilities (XLU, -1.64%), consumer staples (XLP, -1.63%) and healthcare (XLV, -1.43%) - led the onslaught of sellers.

Pre-Market Action

It's going to be a rough start for U.S. equities as Dow Jones futures are lower by nearly 200 points with 30 minutes left to the opening bell. The treasury market is no doubt spooking equity traders as the 10 year treasury yield ($TNX) is down another four basis points to 2.23%. The flight to safety continues in the bond market.

Crude oil prices ($WTIC) are tumbling again, down 1.82 per barrel (-3.08%) this morning and just above $57 per barrel.

Asian markets were mixed overnight, but European markets are clearly sliding. The German DAX ($DAX) has fallen below 12000 again, down 1.48% at last check. The selling pressure in Europe is spilling over to the U.S. this morning. Bulls will be pressured at the open and the Volatility Index ($VIX) will be on the rise. We're going to find out if the bulls are up to the challenge this morning.

Current Outlook

Transportation stocks ($TRAN, -1.30%) fell on Tuesday to close on key short-term price support. While railroads ($DJUSRR, -0.96%) have held up relatively well, airlines ($DJUSAR, -1.18%) have struggled despite falling crude oil prices ($WTIC), and truckers ($DJUSTK, -1.78%) have been decimated over the past week. This combination has left the TRAN teetering with a potential breakdown at hand:

I think the above chart clearly reflects what's going on with transports. Railroads are doing their best to hold the group up, while airlines and truckers are sinking fast. The 9900-10000 level appears to have been a solid area of support/resistance over the past 8 months. If the TRAN loses 9900 support, there's a chance we'll see the selling escalate.

I think the above chart clearly reflects what's going on with transports. Railroads are doing their best to hold the group up, while airlines and truckers are sinking fast. The 9900-10000 level appears to have been a solid area of support/resistance over the past 8 months. If the TRAN loses 9900 support, there's a chance we'll see the selling escalate.

Sector/Industry Watch

The Dow Jones U.S. Software Index ($DJUSSW, -0.07%) reversed yesterday on big volume, but still outperformed the benchmark S&P 500 by a wide margin. Traders have grown used to this outperformance as you can see from the following chart:

This chart really says about all you need to know. Software has been a relative leader throughout the current five month rally. If you've tried to outperform the S&P 500 in 2019, you've likely needed to be in software stocks from time to time because of their overwhelming strength. In order to continue their relative dominance, they'll need to do two things. The first is somewhat obvious. Price support at 2550 needs to hold. We've already seen multiple successful tests there. Seeing a leader lose a key short-term support would not only be bad for this industry, but it'd also be bad for the overall market. Secondly, the relative channel needs to remain intact. Thus far, we've seen zero deterioration in software's relative position. That tells me that when the buying resumes, traders will once again focus on what's been working - and one of those areas is unquestionably software.

This chart really says about all you need to know. Software has been a relative leader throughout the current five month rally. If you've tried to outperform the S&P 500 in 2019, you've likely needed to be in software stocks from time to time because of their overwhelming strength. In order to continue their relative dominance, they'll need to do two things. The first is somewhat obvious. Price support at 2550 needs to hold. We've already seen multiple successful tests there. Seeing a leader lose a key short-term support would not only be bad for this industry, but it'd also be bad for the overall market. Secondly, the relative channel needs to remain intact. Thus far, we've seen zero deterioration in software's relative position. That tells me that when the buying resumes, traders will once again focus on what's been working - and one of those areas is unquestionably software.

Historical Tendencies

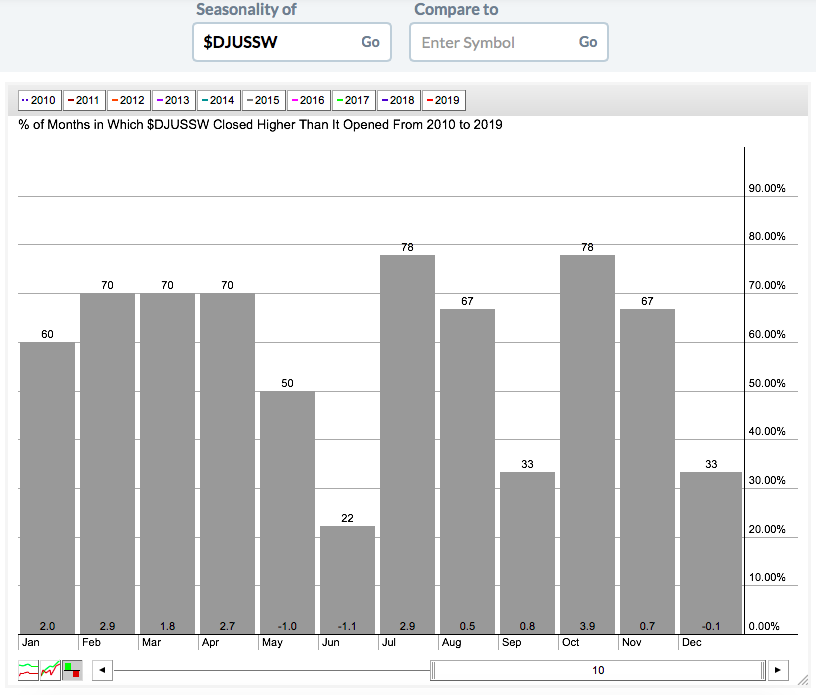

Since the 2009 stock market bottom, software ($DJUSSW) has no doubt been one of the bull market leaders. But one look at the seasonality chart for this past decade suggests caution as we head into June:

The odds of software stocks rising during June has been less than any other month and the average return of -1.1% is lower than any other month. Of course, this isn't to say that the DJUSSW will decline in June 2019. It's simply to point out the seasonal weakness that lies ahead.

The odds of software stocks rising during June has been less than any other month and the average return of -1.1% is lower than any other month. Of course, this isn't to say that the DJUSSW will decline in June 2019. It's simply to point out the seasonal weakness that lies ahead.

Key Earnings Reports

(actual vs. estimate):

BMO: 1.72 vs 1.69

CPRI: .63 vs .61

GOOS: .07 vs .02

(reports after close, estimate provided):

KEYS: .98

PANW: 1.25

PVH: 2.44

UHAL: (.84)

VEEV: .45

VRNT: .62

Key Economic Reports

None

Happy trading!

Tom