Another insightful issue of the ChartWachers Newsletter has arrived!

October 20, 2018

Hello Fellow ChartWatchers!

Welcome to Sector Week! That's right, folks - this week's newsletter has a theme. You'll see the topic of the S&P sectors running throughout each article, with the authors sharing unique insights into the role that the SPDR funds play in their investing/trading routines.

Why? Well, as you may have heard, the markets recently underwent a major reclassification process, which included the addition of two new sectors – Communication Services (XLC) and Real Estate (XLRE). As a result, a large number of stocks were shuffled around to fit with the new 11-sector organization. The ripple effects of this have been extensive and the industry continues to adapt to the new state of things.

To help you better understand exactly what has changed and how the new landscape looks, Julius de Kempenaer and Arthur Hill have put together a helpful article that explains all of these recent changes and data adjustments. Here at StockCharts, the sector and industry classifications are an important aspect of our site organization and market analysis tools, so I want to encourage you to take a minute and read that article below. Finally, to give you an idea of what we've updated so far, here's a quick synopsis:

- The Market, Sector and Industry Summary pages have been updated with all 11 S&P sectors.

- Our PerfChart tool now supports up to 12 symbols, allowing you to chart all 11 sectors against the S&P 500 on one PerfChart.

- The predefined S&P 500 Sectors group now includes XLC and XLRE. This group can be charted as a PerfChart, CandleGlance, MarketCarpet or RRG.

The StockCharts data team still has a few things left to add, including new bullish percent and breadth indexes for the Communication Services and Real Estate sectors, but we'll be sure to keep you informed as these final updates are released on the site. Until then, let's get Sector Week rolling with some great articles from our newsletter contributors!

You may have noticed that in September, a lot was written about the changes in sector classifications that were implemented after the close on the 21st by S&P Dow Jones Indices, the company that maintains and publishes the underlying indices for the popular range of SPDR sector ETFs (XLF, XLK, etc.).

Changes to indices are not uncommon and happen on a regular basis (quarterly). Depending on the guidelines and the index methodology "rule book", companies will be added to or deleted from an index to better reflect the characteristics of the index as described in the rule book. Market capitalization and company activities are the major factors that determine in which sector a stock is classified.

This time, however, the changes not only included adding stocks to or deleting them from various sector indexes, but also an overhaul of the classification structure to better reflect the "new world order, which emerged over the last twenty years. Many of these "new world order" stocks did not exist during the dot com bubble of 2000, but they have gone on to become dominant mega-caps. Think Google, Facebook, Netflix and Twitter.

Bottom-Up Classification

The GICS classification system consists of four levels:

11 - SECTORS

24 - INDUSTRY GROUPS

69 - INDUSTRIES

158 - SUB-INDUSTRIES

The methodology for classification is bottom-up. This means each stock gets classified to a "sub-industry" based on its principal business activity. Revenues are the key factor determining the principal business activity.

From the sub-industry level, a stock will eventually end up in a sector. The 158 sub-industries are rolled up into 69 industries. These 69 industries are then rolled up into 24 industry groups and these are ultimately be rolled up into the 11 sectors at the top of the pyramid.

Hence, once a stock is assigned to a sub-industry you will know immediately to which industry, industry group and sector it belongs.

For every classification level, index-values are calculated and published, and historical data is available since the inception of the GICS system.

Now be careful, these indexes are NOT INVESTABLE or TRADABLE products.

For example, XLK, the "Technology Select Sector SPDR® Fund" is not the same as $IXT, the "Technology Select Sector Index". XLK, an ETF, is an investable product that closely tracks an underlying index, which in this case is $IXT. They are close, but they are not exactly the same.

Numerous asset managers have created investable products based on (GICS) indices. The higher up in the classification pyramid the more products are available. The 11 SPDR Sector ETFs have become so popular and widely traded that they are now often seen as "the sectors", which they are but then they are not. Based on the management fee alone an ETF will always, marginally, underperform its underlying index.

Creating Historical Data

For the SPDR family of sector ETFs, there is plenty of data available for analysis as the ETF and the underlying index were launched at the same time or nearly the same time. This is not always the case. When a provider launches a new product based on an index that exists for many years already, there will be very little data available for the tradable product.

The changes in sector indexes and ETFs for Real-Estate in 2015 and now Communication Services in 2018 required attention because there was very little historical data.

Lack of data does not have to be a show-stopper as we can use the underlying index data for analysis and trade the newly launched product. Ideally, you want to analyze like for like so either you analyze investable products like ETFs or you analyze indexes. Mixing them could cause unexpected problems. For example, one of the two could be a total return series and the other not.

But what if a completely new index is launched together with a tracking ETF? Neither will have data and this makes historical comparisons impossible. And historical comparisons are exactly what we as technical analysts live by.

S&P, some math, and pragmatic (creative?) thinking to the rescue!

Real Estate

Let's start with the "easy" one. In 2015, S&P and MSCI decided to split the GICS financial sector into two new sectors – Financials and Real Estate. At the same time, a sector SPDR for the new Real Estate sector (XLRE) was launched by State Street.

Because Real Estate was an industry group under Financials, this new sector was essentially carved out from the Financials Sector and promoted one level higher in the GICS hierarchy. The historical data for the "new" sector was therefore already available.

At the index level, the historical data for the Real Estate Industry Group is the same as the data for the Real Estate Sector, the split was made at the third GICS level. The Real Estate Industry Group consisted of three industries; (Equity) REITs, Real Estate Management and Development, and Mortgage REITs.

The new Real Estate Industry Group holds only Equity REITs and Real Estate Management and Development. Mortgage REITs stayed with Financials Sector under the industry group Diversified Financials.

In the StockCharts database, we have copied the level-2 index data for Real Estate over to level-1, the Real Estate Sector Index. This now makes it possible to use the Real Estate Sector data in historical comparisons at the index level.

In order to be able to use the investable XLRE ETF in historical comparisons, we have taken the performance data for the Real Estate Index and simulated the performance of XLRE as if it was trading before October 2015 and back-filled the history of XLRE prior to introduction, assuming a 100% correlation.

Chartists can now use XLRE in longer-term charts, compare historical sector performance and use XLRE in tools like PerfCharts.

Note: the back-filled data prior to the start of the real estate as a sector includes mortgage REITs. As real estate used to be part of financials, there is an overlap between financials and real estate prior to the launch as a real sector. The history for XLF nor the underlying index has been adjusted.

Communication Services

From a historical data perspective, the introduction of the new Communication Services sector is a bit more complex. It is a completely new sector and also a dissemination of the old telecom sector. Unlike the Real Estate Sector, there is no historical data whatsoever for the Communication Services Sector.

Here, you can read a good piece on the "why and how" behind the introduction of this new sector as well as the impact on the other sectors. Some big names are changing from one sector to another.

In order to facilitate the financial markets and enable analysts to use historical data for this new sector, S&P Dow Jones Indices calculated the historical performance for the Communication Services Sector based on the current index methodology for the sector. This means they went back in time with a rule-book and created the index-composition at each review date, and then calculated the historical values of the new index.

In order to facilitate the use of XLC in long-term charts and other tools on the website, we have taken a similar route as described for XLRE. We have calculated the performance of the new sector index $IXC, based on the data provided by S&P, and used this performance data to backfill the historical prices for XLC, assuming a 100% correlation with the underlying index.

Chartists can now use XLC and XLRE in longer-term charts, compare historical sector performance and use these tickers in tools like PerfCharts and Relative Rotation Graphs.

Ticker Symbols Affected

Real Estate

XLRE (history already added)

$IXRE (history will be added soon)

Communication Services

XLC (history already added)

$IXC (history will be added soon)

Thanks for reading our explanation of these recent changes and how the sector additions have been handled on StockCharts. Remember, the SPDR sectors are an important component of our site organization and market analysis tools. Be sure to check out the following pages to view the sector and industry classifications.

The Three Dow Averages Are Giving Bearish Messages

by John Murphy

Editor's Note: This article was originally published in John Murphy's Market Message on Thursday, October 18th at 5:00pm ET.

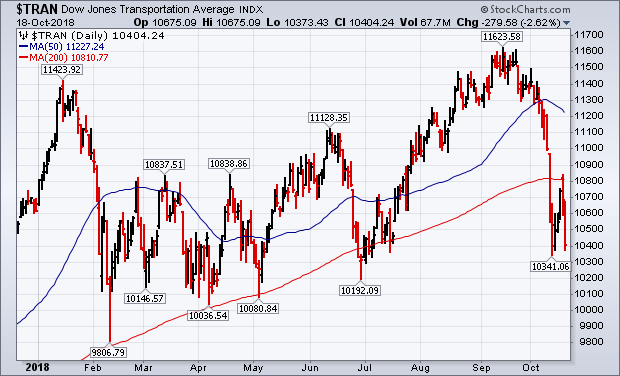

My last two messages spelled out a lot of technical reasons that are bearish for the stock market, and increase the odds that the nine-year bull run is ending. Besides the heavy selling that's taken place during October, my weekend message showed a number of serious negative divergences showing up on the market's weekly and monthly charts. Yesterday's message included the Sector Rotation Model which showed that rotation into consumer staples, utilities, and healthcare stocks usually occur near the end of major bull markets. And money is rotating there. While money is flowing out of economically-sensitive groups like consumer discretionary and industrial stocks, as well as growth-oriented technology. And those are the very groups leading this month's stock retreat. We can also see that negative rotation taking place within the three Dow Averages. Chart 1 shows the Dow Jones Industrial Average continuing to threaten its 200-day average. That's a very important test. The bigger problem lies with the Dow Transports which have already fallen below their 200-day line (see Chart 2).

Big Sectors Weigh as Defensive Sectors Buck the Selling Pressure

by Arthur Hill

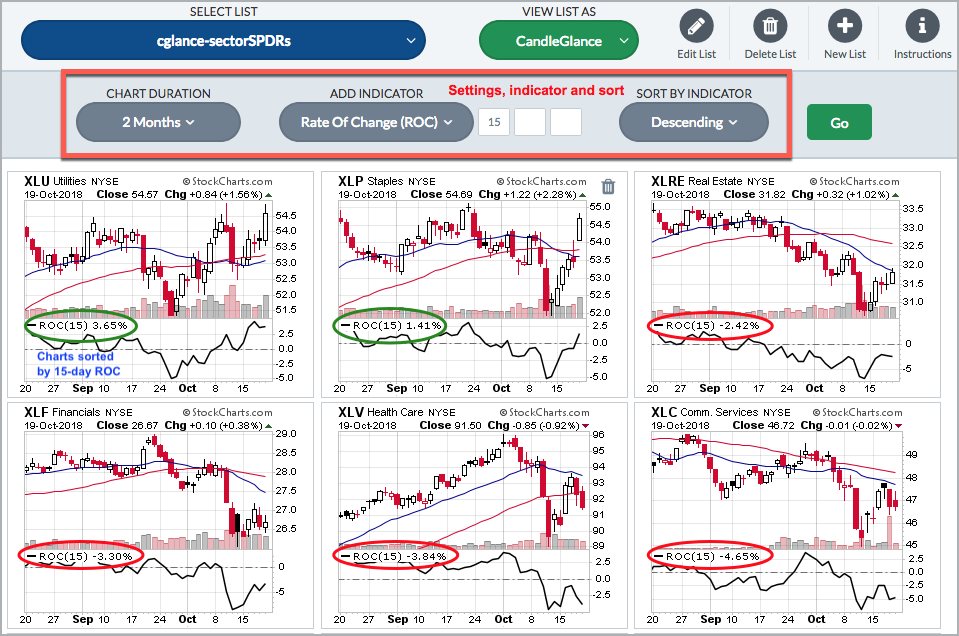

One of my favorite methods for analyzing the sector SPDRs is with CandleGlance charts sorted by the Rate-of-Change indicator to rank performance. This is a great way to quickly separate the leaders from the laggards and analyze short-term price action.

The charts below show the 11 sector SPDRs and the S&P 500 SPDR (SPY) with the 15-day Rate-of-Change, which covers the month of October. The first group shows six sectors, two are up this month and four are down. The Utilities SPDR and the Consumer Staples SPDR, two defensive sectors, are the only two showing gains in October (positive Rate-of-Change). These two sectors represent 9.9% of the S&P 500 and they are the only two holding up. The other four sectors are down less than SPY, but they are still down and weighing on the market. Note that these four account for 41.47% of SPY.

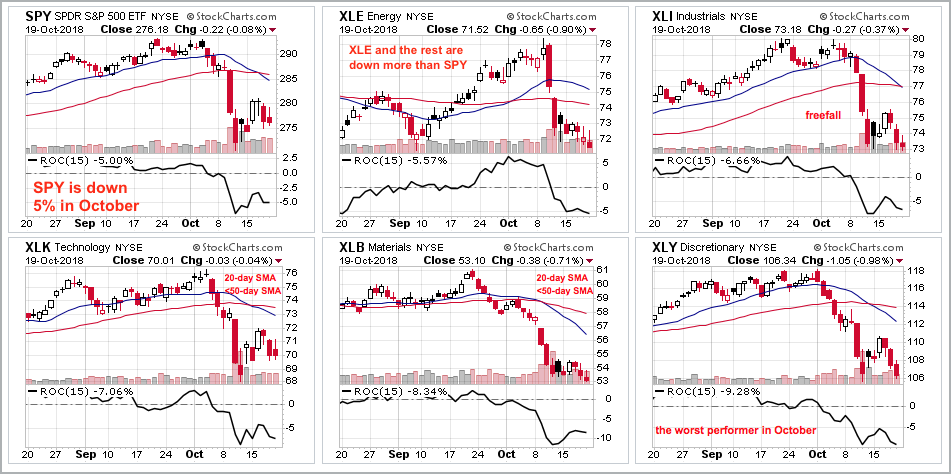

The second group of charts shows the S&P 500 SPDR (SPY) with a 5% decline over the last 15 days. The other five sectors are the real drags on the market because they are down 5% or more, and leading the way lower. These include the Energy SPDR, Industrials SPDR, Technology SPDR, Materials SPDR and Consumer Discretionary SPDR. These five sectors account for 48.63% of the S&P 500. All told, nine of the eleven sectors are down this month and these nine account for around 90% of the market. This is extremely broad selling pressure. You can find the sector weightings on the SPDR website.

On Trend on Youtube

Available to everyone, On Trend with Arthur Hill airs Tuesdays at 10:30AM ET on StockCharts TV and repeats throughout the week at the same time. Each show is then archived on our Youtube channel.

Topics for Tuesday, October 16th:

Volatility Increases when Below 200-day (Risk On/Off)

Don't Estimate Depth or Duration (Dow Theory)

Scanning for Above/Below 200-day (Weight of Evidence)

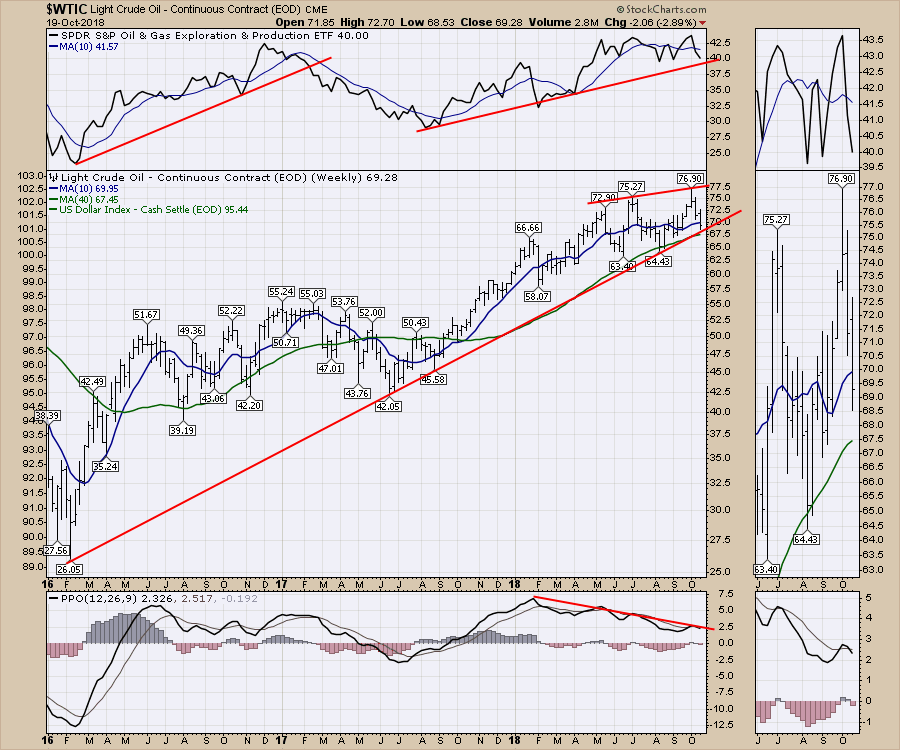

The setting couldn't be more climactic. Oil, seems to be generating attention from the world through Saudi Arabia, Iran, Russia, pipelines, global slowdown, trade pressures with China, EU issues in Germany and Italy, Brexit, Steel tariffs and the list goes on. The world's awareness is always high. This week, the chart arrives at a critical point again.

Oil closed the week testing the 3 year uptrend line off the 2016 low. Both the Exploration and Production ETF (XOP) as well as crude oil closed below the 10 week moving average. But more importantly, as oil has gone higher, the momentum has been slowing, shown on the PPO. Notice in the zoom panel that the PPO momentum indicator flipped to a sell signal again. Ignore the news. Watch the price action for investing in the energy sector.

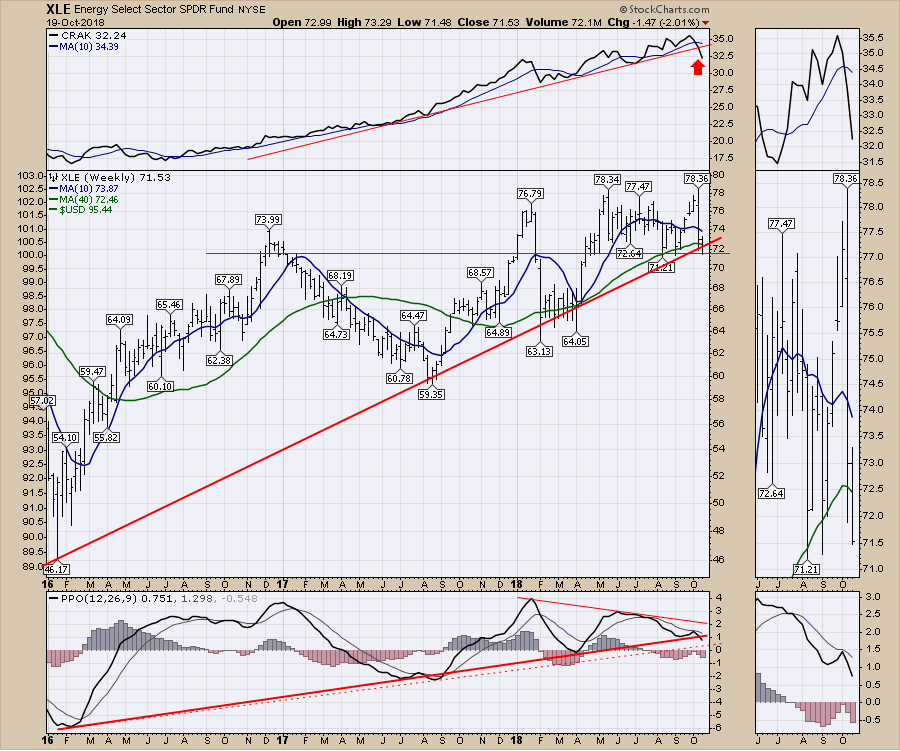

The refiners have been outperforming as the refining margin has increased over the last few months. The CRAK ETF for refiners suggests that is coming to an end after breaking a two year uptrend and the XLE sector ETF suggests weakness as well. Using weekly closes rather than intra-week lows, this is the first week where the ETF closed below the 18 month trend line. I extended the trend line back and it meets up with the absolute low in 2016 but not the weekly close for that week.

Staying with the chart above, I would suggest the up move in Energy is over as the PPO is also breaking down. There are lots of variables coming with Iranian sanctions November 1 as an example. But the second lower high on the PPO and the break of the uptrend on the PPO suggests caution is warranted. With all of these charts and indicators cracking, its important to remember commodity related stocks move fast both ways!

The bottom line, don't go surging into energy related stocks here unless you have tight stops below.

Bottom line = Protect your Energy related portfolio until the charts improve.

Lastly, it might be time to start looking for some short term bounce stocks here. Both the NYSE and the NASDAQ summation indexes are getting near levels that usually mark annual lows. If we are heading into the bear market these bounces will be short, fast and convincing that the bull is alive and well. But the moves can be swift enough to make a years returns in a few weeks.

I will be describing these setups on this weekends edition of the Commodities Countdown video. Lots of indicators are stretched to the downside. Check the StockCharts Youtube channel or my Canadian Technician blog where all my work is posted. Below is the October 13th Commodity Countdown Video.

If you haven't seen my article on Is A Major Top In Place? I would encourage you to look through the article and decide if the charts provide enough evidence for you to consider the possibility.

I would encourage you to watch the three videos below this week to see if you agree. We can choose to differ, I would just like more facts suggesting why I am wrong.

The Canadian Technician video shows the massive breakdown on almost every sector chart in Canada. This week the Canadian market started what appears to be a major breakdown. Financials also fell outside their channel and below the 40 WMA. For Canadian investors, huge caution here.

Gold is perking up, a few of the agriculture commodities are perking up and Natural Gas has been behaving well. However, the stocks around those areas are still struggling with the overall market sentiment. Lots of information in here on the indexes, currencies, bonds and commodities.

This is a short look at the broad market setup and some of the indicators that told us the market was fragile ahead of the drop.

If you are missing intermarket signals in the market, follow me on Twitter and check out my Vimeo Channel often. Bookmark it for easy access!

Good trading, Greg Schnell, CMT, MFTA

Senior Technical Analyst, StockCharts.com

Author, Stock Charts for Dummies

Want to read more from Greg? Be sure to follow his StockCharts blog: The Canadian Technician

Sector Relative Performance Suggesting Caution, Not Bear Market

by Tom Bowley

There are plenty of reasons why we should be cautious given the current market environment, but I'm not in the camp that believes we've entered a bear market. It's simply too early to make that call, in my opinion. Most corrections and bear markets begin similarly, with expanding volatility and fear, short-term price breakdowns and rotation from aggressive areas of the market to more defensive areas. As I look back at the past month, check, check and check.

The January 2018 top and subsequent breakout look very similar to the what we saw back in Q3 2014. Here's a chart to show the similarities in terms of price action:

The green arrows in 2013 and 2014 highlighted a rising 20 week EMA that provided great support and the green shaded area on the Volatility Index ($VIX) shows that there was little fear throughout this uptrend. In October 2014, price action moved swiftly beneath the 50 week SMA and a surge in the VIX above 30 marked a very significant price bottom (red arrows). After the market rallied and higher highs printed, we saw more market weakness with rising VIX levels and retracements toward earlier price support (black arrows).

I am definitely short-term cautious. It makes a lot of sense to allow the market time to settle down. The VIX is currently near 20 and elevated VIX readings (those above 15-16) can lead to very swift, impulsive selling. Furthermore, next week is the worst historical period of the year. Since 1950, the S&P 500 has produced annualized returns of -41.24% from October 22nd through October 27th. That spans all of next week. The 2532 low in February is very significant because buyers finally showed up at that level after panicked selling. It also was retested two months later and held.

But here's the real problem I have with this being the start of a bear market. Aggressive sectors have been rising on a relative basis all year. Check out this chart:

Wall Street normally sees bear markets coming before they're here. We typically see plenty of rotation to defensive areas as we're making the final highs. Over the past quarter, we've seen significant outperformance by technology, consumer discretionary and the newly-created communication services. That generally does not precede a bear market.

So I'll simply remain cautiously bullish for now. I do believe there's a better than 50-50 chance we're heading back to those February 2018 lows and that could be a scary ride similar to what the stock market experienced in late-2015 and early-2016.

Can Strong Earnings Provide a Safe Haven into Year End?

by John Hopkins

The market has been under fire for the past two weeks. Volatility has spiked. Traders have bailed as they've sold on rallies. Bad news is bad news. Good news is bad news. No one wants to touch stocks!

We can take a look at Netflix as a great example of the mindset of traders at the moment as it reported strong earnings, gapped up sharply on strong volume then a day later gave all those gains back.

We can ask ourselves - if the overall market environment was bullish, would Netflix's gains have held? Possibly, though there's no way of telling. But we may well find that the pullback in the stock presents a very nice buying opportunity once things settle down; it just might take a lot of patience because we have found time and again that companies that report strong numbers get the attention of traders since they like to gravitate to those stocks that beat expectations.

I bring this up since thousands of companies will be reporting earnings over the next 3-4 weeks and there could be some great opportunities once the market puts in a near term bottom. This could be especially true as we move into November and December, two months that have historically been quite bullish. In fact, here is the performance from late October until December 31 of each of the past 4 years with the jury still out for 2018:

Even if the market ends up with negative performance between now and year end, traders who focus on the "best of the best" - those companies that beat earnings expectations - have a better chance of out-performing the overall market. In fact, we will be conducting one of our quarterly earnings webinars this Monday, October 22, titled "Preparing for a Profitable Year End," where we will discuss which sectors/stocks are likely to lead the way into year end. We'll also discuss what stocks might rally substantially based on history and strong earnings. And we'll share with webinar participants how we develop our Strong Earnings Chart List, a powerful tool in any market environment. If you want to join Tom Bowley and me for this FREE and highly educational event, just click here.

When the market is down and out, it becomes more difficult to make successful, profitable trades. But if you turn your attention to those companies that out-perform, you'll increase the odds of making some nice scores.

Major New S&P Sectors and Realignments: Biggest ChartPack Update Ever (Q3, 2018)

by Gatis Roze

Ladies and Gentlemen: the most significant shakeup in sector classifications within the past decade has just occurred. Two of the world’s biggest index providers — Standard & Poor’s (S&P) and MSCI, Inc. — have reorganized critical sector indexes.

It’s a good time to take stock of what you really own so you know which team to cheer for. Some of your favorite teams have traded away a number of “Hall of Fame” players. No worries, this updated ChartPack (our most significant since 2013) will help you make all the necessary adjustments.

We’ve added the new SPDR Communications Services Sector Fund (XLC) and realigned those sector funds that ripped Facebook and Google (Alphabet) from their ranks. For example, Technology (XLK) has lost some of its biggest stars!

The importance of this cannot be overstated. In our books, Grayson and I always preached that getting the sector selection right provided the foundation for the majority of your profitable investments. Getting it wrong could be painful.

For example, over the past 10 years, if you were in Consumer Discretionary (XLY) or Technology (XLK), you should have made a lot of money. On the other hand, if you were in Financials (XLF) or Energy (XLE), chances are you did not make much money. Our point is that you need to stay on top of what is happening in the market sectors where the institutional money is flowing.

There has been a significant shift in sector weightings relative to the S&P 500. For example, Technology (XLK) previously accounted for 25.6% of the S&P 500. Now, the new weight is down to 20.1%. Similarly, Consumer Discretionary was 12.7% and is now 10.0%. Of course, the new Communication Services Sector ETF (XLC) has gone from 0.0% to 10.2% overnight. Here are just a few of the updates in the ChartPack:

THIS QUARTER’S ENHANCEMENTS

ChartList #400 Sectors / Master List:

This ChartList has added the new Communication Services Sector SPDR (XLC) which includes heavyweights such as Facebook, Alphabet, Disney, Netflix, Charter Communications, Activision, Electronic Arts, AT&T, and Verizon. Clearly, an important sector of the market of which you need to keep abreast.

#401 Consumer Discretionary SPDR:

I’ll use Consumer Discretionary SPDR (XLY) as a model example for all the other sector ChartLists. You will note that the largest holdings have been updated and are reflected in both the PerfChart as well as individual equities (the top holdings) which each have their own charts. In the ChartList notes, you’ll see specific percentages. For example, Amazon (23%), Home Depot (10%), McDonald’s (6%), etc. These reflect both the impact and the allocation that these equities have upon this Consumer Discretionary Sector SPDR (XLY). Don’t overlook the fact that this ChartList also has four sister sector ETFs included in the ChartList.

Vanguard Consumer Discretionary Sector Fund (VCR)

Blackrock Consumer Discretionary Sector Fund (IYC)

Invesco Equal Weight Consumer Discretionary Sector Fund (RCD)

iShares Global Consumer Discretionary Sector Fund (RXI)

Similarly, the same additions and adjustments have been made to ChartLists #402 (XLI), #403 (XLU), #404 (XLB), #405 (XLP), #406 (XLK), #407 (XLE), #408 (XLV), #409 (XLF), #411 (XLRE), and #413 (XLC).

NEW! #413 Communication Services Sector SPDR (XLC)

This is the new creation. The Sector Fund has pulled key equities from other sectors and given them a new home here. The composition is as follows:

Facebook (17.2%)

Alphabet C (11.7%)

Alphabet A (11.5%)

Charter Communications (4.5%)

Disney (4.7%)

Netflix (4.5%)

Electronic Arts (4.5%)

Activision (4.5%)

This ChartList also includes two sister ETFs. Vanguard Communication Services Sector ETF (VOX), as well as iShares Global Communications Services Sector ETF (IXP). For those of you unfamiliar with our “sisters Strategy”, you should either refer to our book (Tensile Trading) or, at the very least, some of our past “Traders Journal” blogs.

#450 US Dow Industry Groups

Understanding how all these massive changes in indexes and industry groupings will affect your investments is something that will take some effort. A powerful routine that Grayson and I use is to sort this ChartList of all 152 Dow Industries by one-month performance. Presently, it will highlight strength in aerospace and telecommunications, along with weakness in home construction and real estate which — surprise, surprise — does not jive with all the bullish press about real estate. In any event, make this ChartList part of your routines. You’ll be pleased you did!

LESSON: It’s fine to be a fundamentalist investor, but you still need a modicum of charting acumen; otherwise, when the market speaks, you’ll be deaf. — Gatis Roze

Request for ChartPack Users: We would like to solicit your opinions and thoughts as to how and why you use the ChartPack. The user community now numbers in the thousands, and we believe your fellow investors would like to hear from other users. Please send your comments and thoughts to gatisr@stockcharts.com. We’ll assemble your input into a future Traders Journal blog and share it with the entire community.

#420-12 to 420-90 - Fidelity Sector Portfolios

Each quarter, we spend a significant amount of time pouring over the recently updated Fidelity listings for all 40 of their Select Portfolio funds, diligently comparing last quarter’s holdings to the new releases. We look to these funds as an interesting source of tradable ideas, a way to see where and how the big money on Wall Street – some of the largest and most well-researched managers – are deploying their capital. Each quarter, this painstaking analysis yields some remarkable insights, and each quarter, we walk away with a host of actionable ideas.

Sometimes, however, the takeaways can be found in what the funds are NOT doing.

Yes, you read that right. “…in what the funds are NOT doing”. The most notable observation from this quarter’s update was the shocking number of unchanged funds – Select Portfolios with no change in their top 10 holdings. We noticed more unchanged funds than in any quarter in the past five years.

Not only that, but we also noticed that this quarter saw more funds adding to previous positions than ever before. As you may know, we keep track of the stocks that were dropped from each fund’s top 10 holdings list in the latest quarter. When a stock was dropped last quarter but reappears this quarter, we note that down as an “added back” position. In our time tracking these Fidelity fund moves, we’ve never seen this high a number of “added back” positions.

This gives us a unique insight into the vibe of the “smart money” folks. With all of the sector reclassifications, the changing market tides, and a distinct shift in the investment landscape, this did not seem to be an aggressive quarter for the Fidelity teams. That observation was not only intriguing but also unusual.

That said, here are three interesting notes about a few specific moves:

The Materials fund added a BIG position in a large paint company. Be sure to check out that fund and take a look at the chart.

The Technology fund reduced its total position number by a very significant percentage, but it also saw a major shakeup in its top 10 holdings list. Among the changes were big new positions in two FAANG members, while EA and TSLA got the boot.

One stock that popped up as a new holding across quite a few funds was PG&E (PCG). When you see a company with widespread support like this, it can be an interesting sign and a nice boost for the stock. If you like the chart, this one might be worth watching.

Already have the ChartPack? Here's how to upgrade:

Log in to your account, then visit the "Manage ChartPacks" page (accessible from the bottom of the Members Dashboard or from the "Your Account" page).

In the table that appears, find the entry for the "Tensile Trading ChartPack"(if you don't see the Tensile Trading ChartPack listed, that means that you haven't purchased it. Click Here to do so now).

Click the "Re-Install" button next to the Tensile Trading ChartPack to start the update process

The download should take about 15 seconds, after which you can explore the new ChartLists and other updates!

New to the ChartPack? Here's how to install it:

If you'd like to add the Tensile Trading ChartPack to your StockCharts account, Click Here.

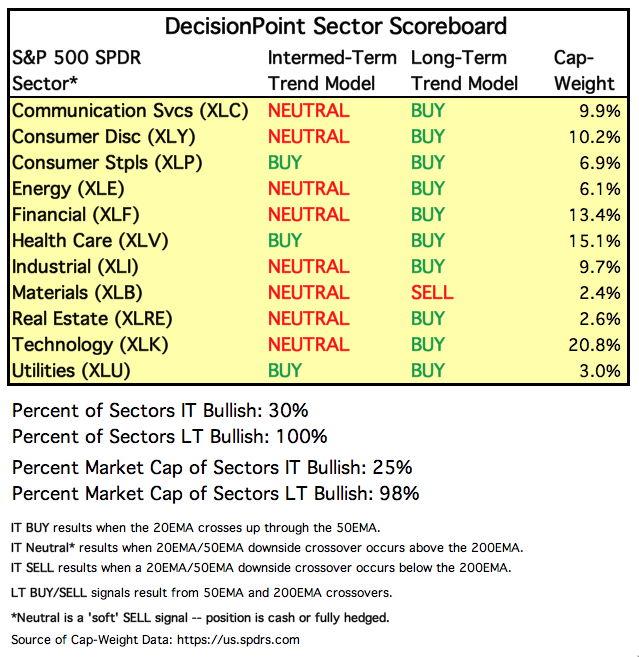

If you've explored the member dashboard, read a DP Alert or checked into the DecisionPoint Chart Gallery, you are likely familiar with our DecisionPoint Scoreboards for the SPX, OEX, INDU and NDX. What you may not have uncovered was our DecisionPoint Sector Scoreboard. Carl assembled a table that not only shows you intermediate-term and long-term buy/sell signals, but also includes the sector weightings. You'll find the DecisionPoint Sector Scoreboard in the DecisionPoint blog on Wednesdays (DP Alert) and Fridays (Weekly Wrap).

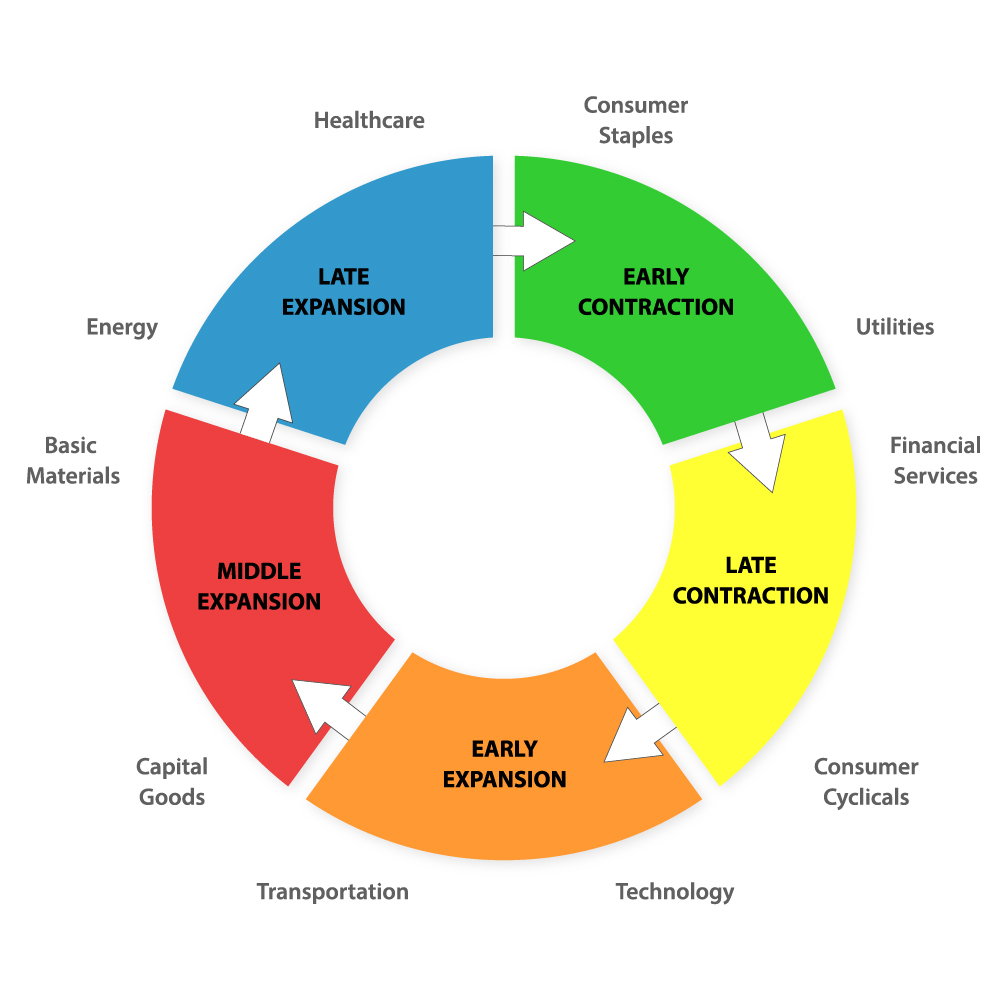

A quick glance at the DP Sector Scoreboard and the deterioration of the many of the major sectors. Since October began, this Scoreboard was completely green at the beginning of October. The remaining Intermediate-Term Trend Model BUY signals are in the "defensive" sectors. As many of our authors have written in this edition of ChartWatchers, understanding which sectors are leading, we can determine the health of the market, as well as the sentiment of participants. Below is an illustration of the rotation cycle.

The area we want to see begin to improve is Financials. Below is the daily chart of XLF. It is sitting on longer-term support right now. It has been consolidating sideways in a wide trading range starting in Mar/Apr. The IT Trend Model Neutral signal suggests we could see more of it. The PMO does make me somewhat optimistic. Yes, it is still declining, but it is very oversold. A bottom and BUY signal on the PMO might mark the beginning of a healthy rally to at least overhead resistance. I'll need to see the consolidation channel broken and at least a rising trend before I'd consider it a sign of another rotation in the market.

Conclusion: With strong leadership in defensive sectors of the market, it will be hard to build an intermediate-term upside reversal. Watch for Financials to perk up next.

Technical Analysis is a windsock, not a crystal ball.

As a StockCharts Member, you unlock all of our most powerful tools and features, including saved charts and settings, custom scans, technical alerts and much more. Discover all that StockCharts can do with our free 1-month trial and start charting like a true market pro.

One of my favorite methods for analyzing the sector SPDRs is with CandleGlance charts sorted by the Rate-of-Change indicator to rank performance. This is a great way to quickly separate the leaders from the laggards and analyze short-term price action.

One of my favorite methods for analyzing the sector SPDRs is with CandleGlance charts sorted by the Rate-of-Change indicator to rank performance. This is a great way to quickly separate the leaders from the laggards and analyze short-term price action.

We can ask ourselves - if the overall market environment was bullish, would Netflix's gains have held? Possibly, though there's no way of telling. But we may well find that the pullback in the stock presents a very nice buying opportunity once things settle down; it just might take a lot of patience because we have found time and again that companies that report strong numbers get the attention of traders since they like to gravitate to those stocks that beat expectations.

We can ask ourselves - if the overall market environment was bullish, would Netflix's gains have held? Possibly, though there's no way of telling. But we may well find that the pullback in the stock presents a very nice buying opportunity once things settle down; it just might take a lot of patience because we have found time and again that companies that report strong numbers get the attention of traders since they like to gravitate to those stocks that beat expectations. Ladies and Gentlemen: the most significant shakeup in sector classifications within the past decade has just occurred. Two of the world’s biggest index providers — Standard & Poor’s (S&P) and MSCI, Inc. — have reorganized critical sector indexes.

Ladies and Gentlemen: the most significant shakeup in sector classifications within the past decade has just occurred. Two of the world’s biggest index providers — Standard & Poor’s (S&P) and MSCI, Inc. — have reorganized critical sector indexes.

The area we want to see begin to improve is Financials. Below is the daily chart of XLF. It is sitting on longer-term support right now. It has been consolidating sideways in a wide trading range starting in Mar/Apr. The IT Trend Model Neutral signal suggests we could see more of it. The PMO does make me somewhat optimistic. Yes, it is still declining, but it is very oversold. A bottom and BUY signal on the PMO might mark the beginning of a healthy rally to at least overhead resistance. I'll need to see the consolidation channel broken and at least a rising trend before I'd consider it a sign of another rotation in the market.

The area we want to see begin to improve is Financials. Below is the daily chart of XLF. It is sitting on longer-term support right now. It has been consolidating sideways in a wide trading range starting in Mar/Apr. The IT Trend Model Neutral signal suggests we could see more of it. The PMO does make me somewhat optimistic. Yes, it is still declining, but it is very oversold. A bottom and BUY signal on the PMO might mark the beginning of a healthy rally to at least overhead resistance. I'll need to see the consolidation channel broken and at least a rising trend before I'd consider it a sign of another rotation in the market.