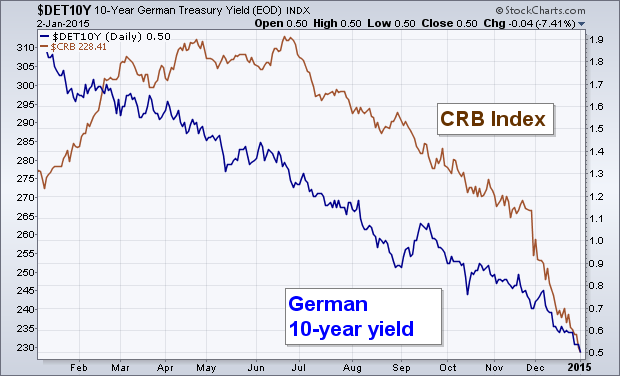

One of the biggest concerns for 2015 is the prospect for higher interest rates in the U.S. While it's true that the Fed may start to hike rates later in the year, that doesn't mean that bond yields will rise very much. The Fed controls short-term rates, while bond yields are determined by economic strength, inflation expectations, and foreign markets. The chart below shows two deflationary forces that should keep U.S. bond yields under control this year. The plunge in the CRB Index during 2014 suggests that any threat from commodity inflation is nowhere in sight. [The fact that the U.S. Dollar Index is nearing a ten-year high should also keep commodity prices from rising much this year]. The second factor weighing on Treasury yields is the plunge in foreign yields. The blue line in Chart 4 shows the German 10-year yield falling to 0.50% which is the lowest in history. [The five-year German yield has turned negative for the first time ever]. The spread between the 10-Year U.S. and German yields has reached the widest level in 15 years. Foreign money moving into higher-yielding Treasuries (also attracted by a stronger dollar) should keep Treasury prices from falling too far and yields from moving too high. All of which suggests that fears of rising rates this year may be somewhat overblown.