Last Friday (August 13), the University of Michigan released the initial August response to their consumer sentiment survey. A sharp 13.5% retreat was recorded. The Expectations Index fared even worse, with a 17.5% drop. According to the summary report, only six of these monthly surveys since the late 1970s have seen a more substantial deterioration. The question naturally arises: What does this mean for the stock market?

Consumer Sentiment vs. Equities

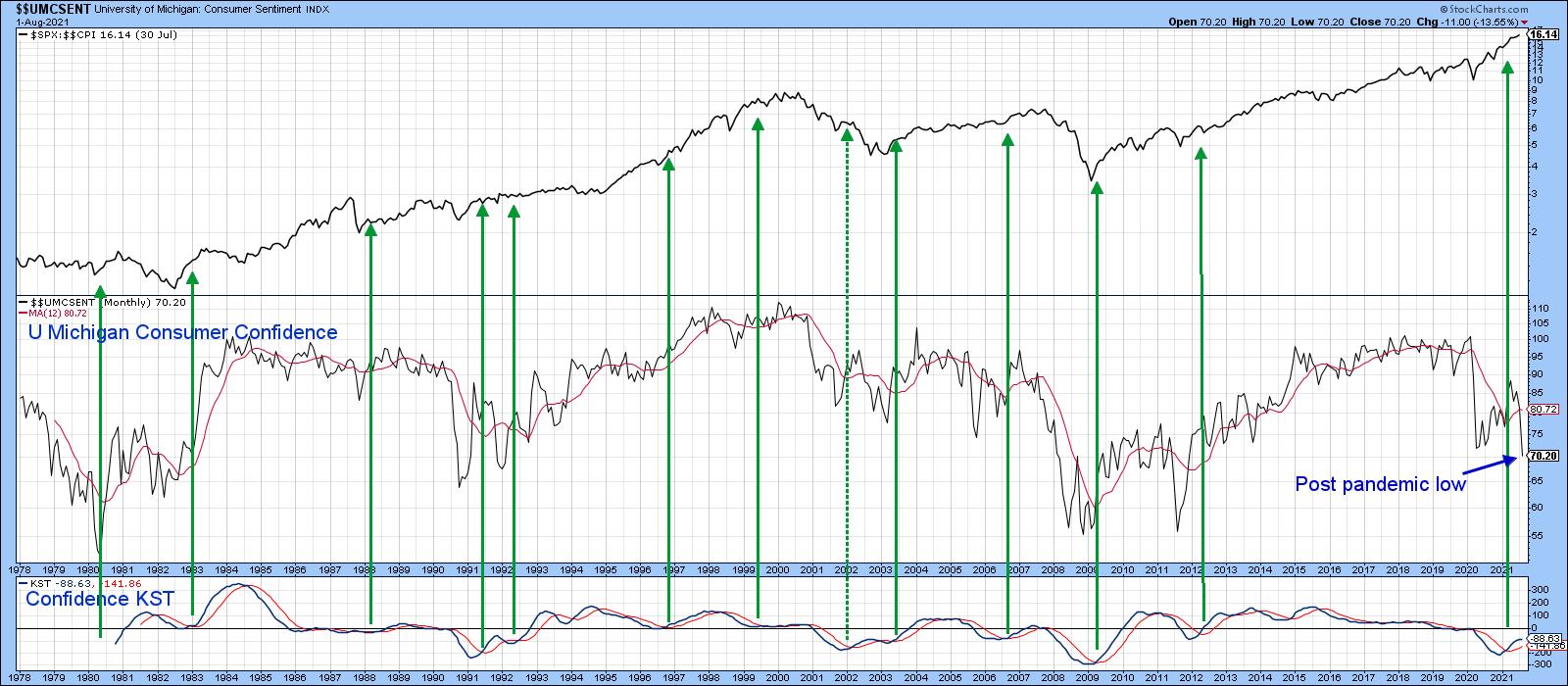

Chart 1 compares the survey to the inflation-adjusted S&P Composite. Given the huge recent jump in the CPI, it seems more appropriate now for long-term charts to express stocks in purchasing value terms than nominal ones. While the chart shows that there is an obvious connection between stocks and sentiment, the sentiment numbers are really too volatile to be of any consistent value in forecasting equity prices. However, if we run a smoothed momentum (KST) through the data, some reasonably timely buy signals are returned. In this respect, sub-zero upside KST reversals have been flagged by the green arrows. The KST is still bullish. However, the weak August data has thrown the latest signal into question, as it has caused the indicator to stabilize.

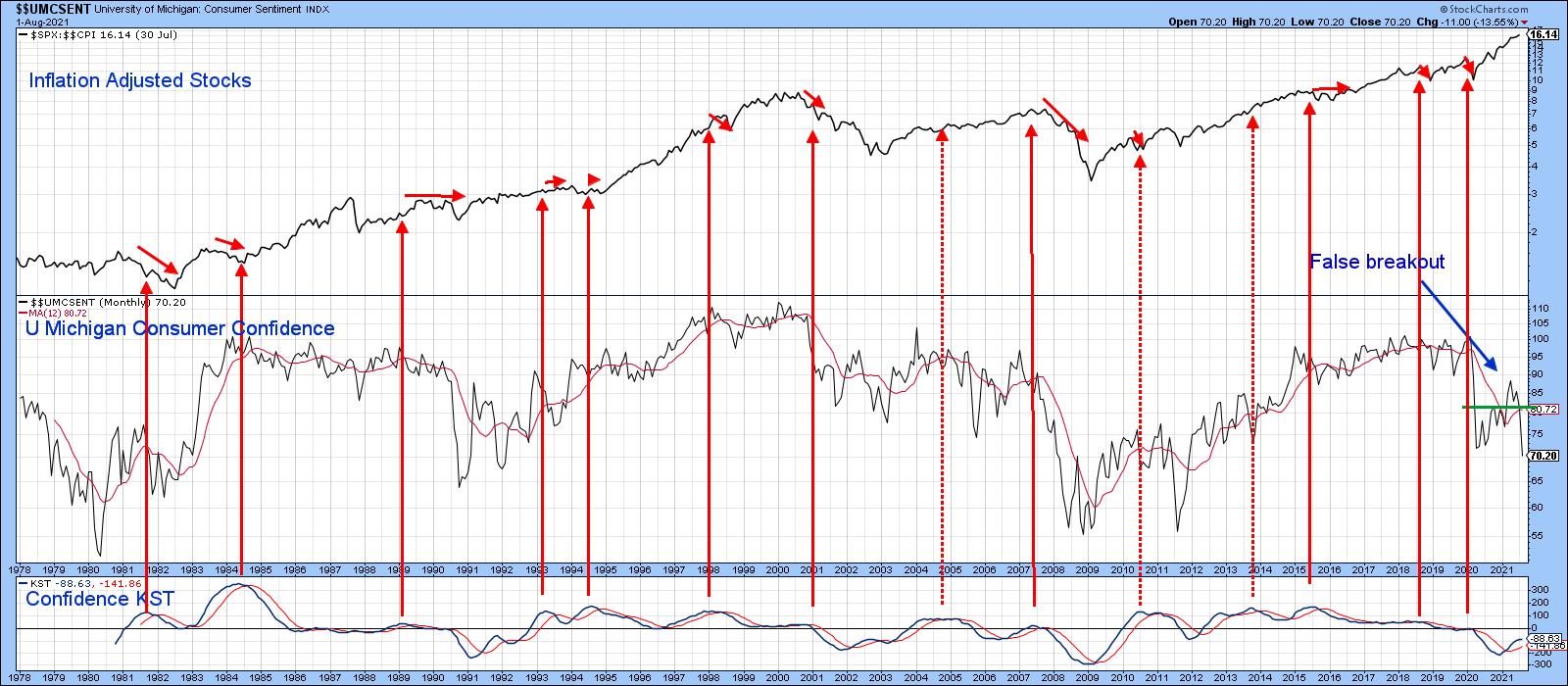

Chart 1Chart 2 features the same exercise but from a bearish point of view. My conclusion is that that these signals definitely have a bearish bias, but are not quite as reliable as the buy ones. It's important to note that the KST has not yet given a sell signal, so to conclude otherwise is jumping the gun a bit. However, if we get much more deterioration, the implication would be negative for stocks.

Chart 1Chart 2 features the same exercise but from a bearish point of view. My conclusion is that that these signals definitely have a bearish bias, but are not quite as reliable as the buy ones. It's important to note that the KST has not yet given a sell signal, so to conclude otherwise is jumping the gun a bit. However, if we get much more deterioration, the implication would be negative for stocks.

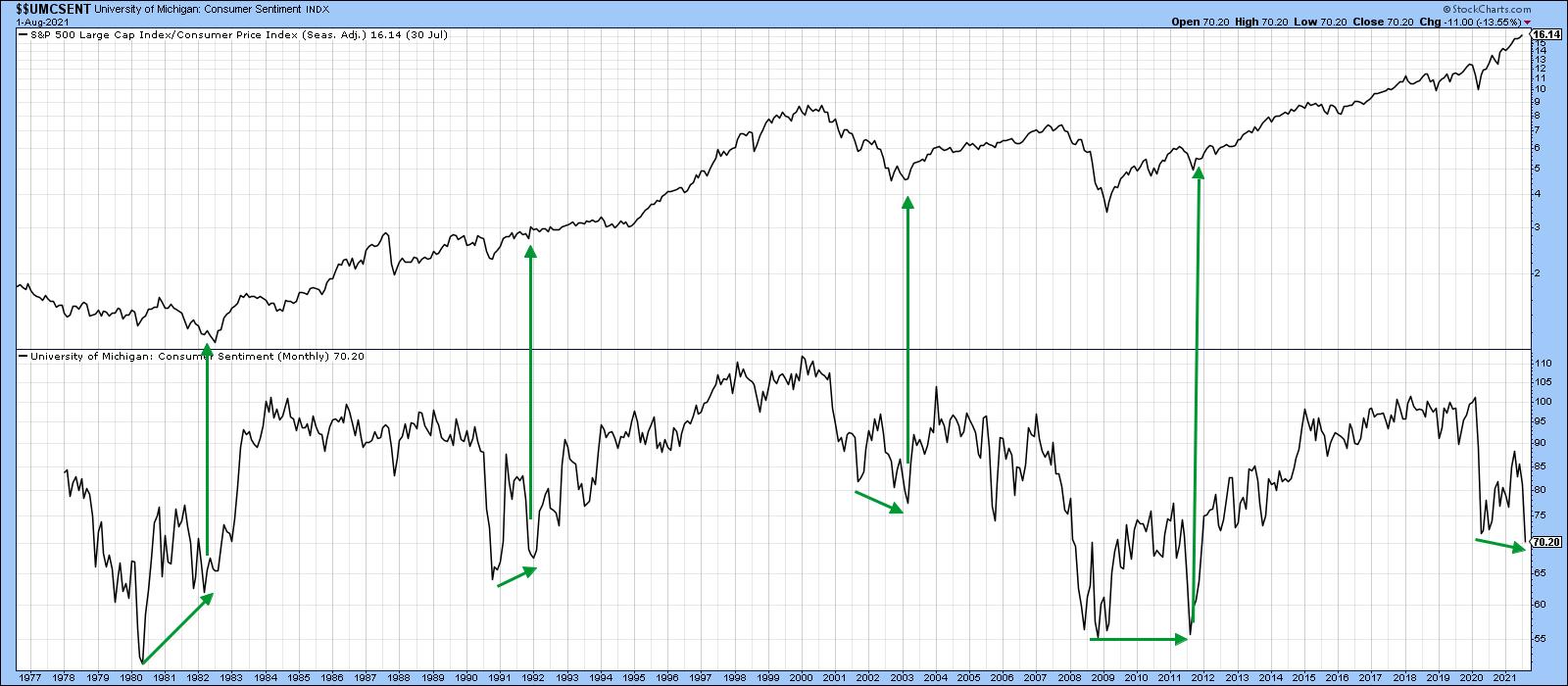

Chart 2Chart 3 offers more hope as it points up that most cyclic lows in sentiment are followed a year or so later by a test; hence the green arrows. There have been four such setups since the 1970s -- each was followed by a very nice long-term rally in inflation-adjusted stocks. In their August consumer sentiment report, the authors state that a huge contributor to weakening sentiment was the unexpected resurgence of the pandemic, just when it appeared that things were returning to normal. The seven-day average of some European countries has started to look better than that for the US. If that proves to be a leading indicator of better things to come, perhaps it would relieve downward pressure on the sentiment numbers, thereby triggering a fifth buy signal for stocks. That's something worth thinking about.

Chart 2Chart 3 offers more hope as it points up that most cyclic lows in sentiment are followed a year or so later by a test; hence the green arrows. There have been four such setups since the 1970s -- each was followed by a very nice long-term rally in inflation-adjusted stocks. In their August consumer sentiment report, the authors state that a huge contributor to weakening sentiment was the unexpected resurgence of the pandemic, just when it appeared that things were returning to normal. The seven-day average of some European countries has started to look better than that for the US. If that proves to be a leading indicator of better things to come, perhaps it would relieve downward pressure on the sentiment numbers, thereby triggering a fifth buy signal for stocks. That's something worth thinking about.

Also worth noting is the fact that the market had a perfect excuse to sell off sharply last week, given the chaotic exodus from Afghanistan. That ability to shrug off good news is usually a sign of strength.

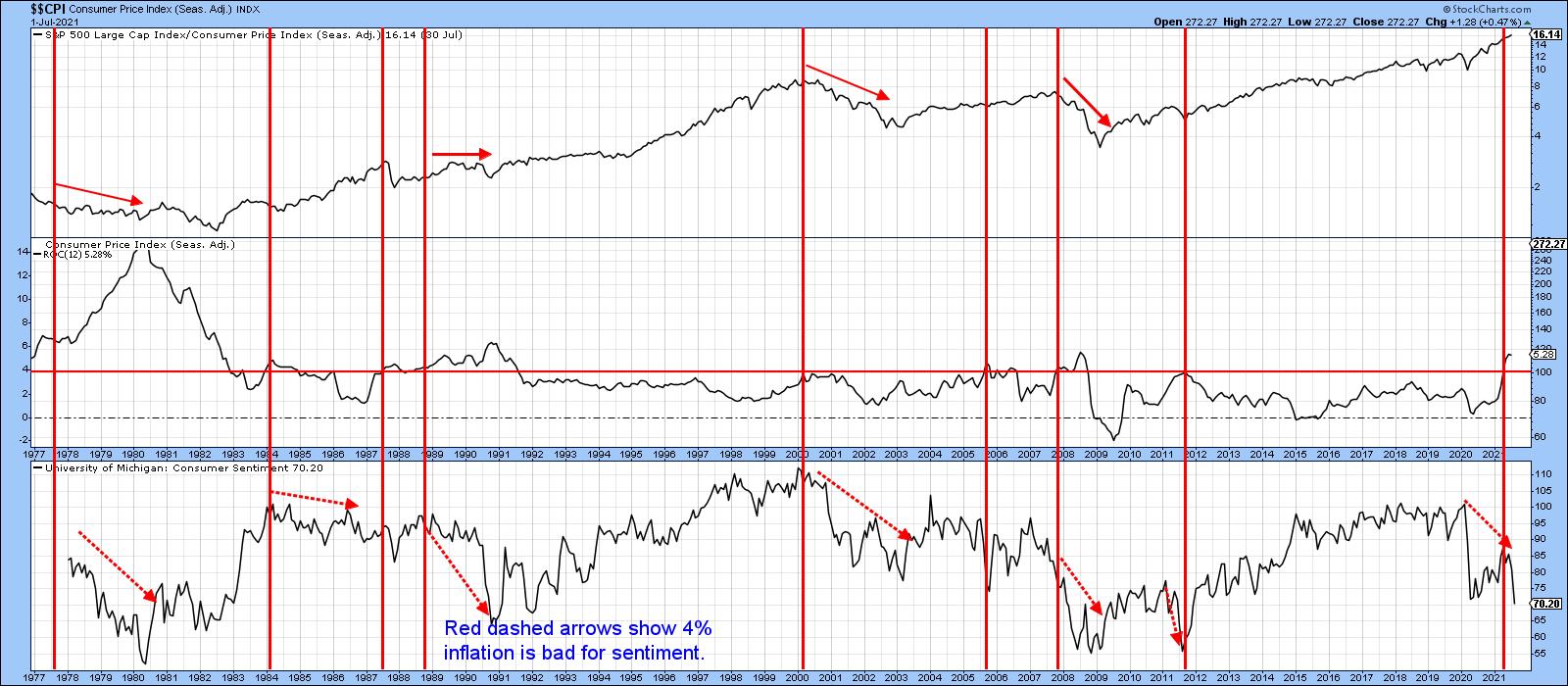

Chart 3That said, there may be another factor adversely affecting sentiment. That factor is inflation. This is shown in the bottom two windows of Chart 4, comparing the 12-month ROC of the CPI to consumer sentiment. The red horizontal line in the center window flags what appears to be the CPI warning level at 4%. The vertical lines flag those points where the ROC initially touches 4%. Note the red-dashed arrows plotted against the Consumer Sentiment Indicator. Every situation since the late 1970s has been associated with an extended deterioration in sentiment. There was one exception, which took place in 2012; in that instance, sentiment again deteriorated, but it did so prior to the CPI reaching the 4% level. When it did, a quick reversal followed and the stock market, in the top window, rallied.

Chart 3That said, there may be another factor adversely affecting sentiment. That factor is inflation. This is shown in the bottom two windows of Chart 4, comparing the 12-month ROC of the CPI to consumer sentiment. The red horizontal line in the center window flags what appears to be the CPI warning level at 4%. The vertical lines flag those points where the ROC initially touches 4%. Note the red-dashed arrows plotted against the Consumer Sentiment Indicator. Every situation since the late 1970s has been associated with an extended deterioration in sentiment. There was one exception, which took place in 2012; in that instance, sentiment again deteriorated, but it did so prior to the CPI reaching the 4% level. When it did, a quick reversal followed and the stock market, in the top window, rallied.

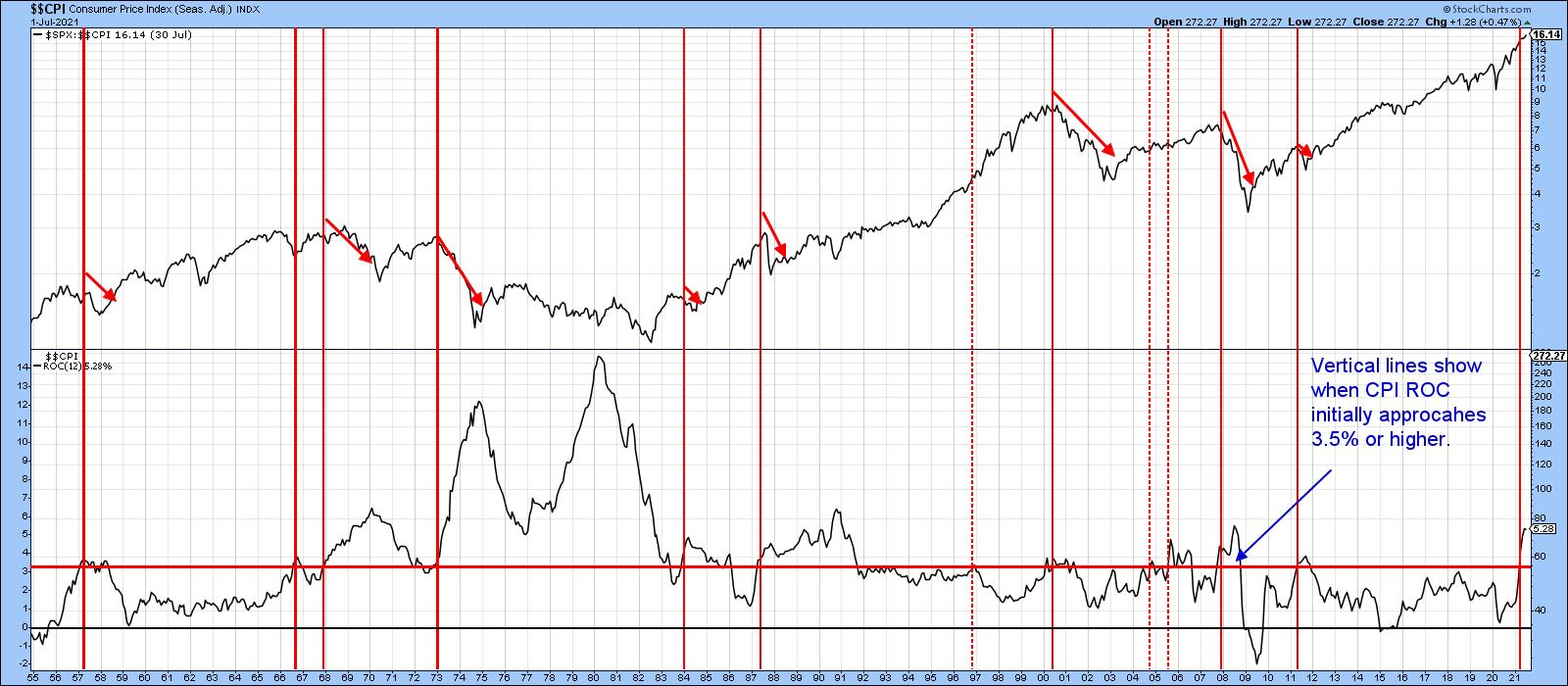

Chart 4Finally, Chart 5 compares the inflation-adjusted stock series to a longer history of the CPI 12-month ROC. This time, the bar has been set a little lower at approximately 3.5%. Once again, the vertical lines flag the initial achievement of 3.5%. The three dashed ones indicate that inflation does not always have a negative impact on inflation-adjusted prices. On the other hand, the solid lines remind us that virtually every bear market in real prices has been associated with an inflation rate that has touched or significantly exceeded 3.5%.

Chart 4Finally, Chart 5 compares the inflation-adjusted stock series to a longer history of the CPI 12-month ROC. This time, the bar has been set a little lower at approximately 3.5%. Once again, the vertical lines flag the initial achievement of 3.5%. The three dashed ones indicate that inflation does not always have a negative impact on inflation-adjusted prices. On the other hand, the solid lines remind us that virtually every bear market in real prices has been associated with an inflation rate that has touched or significantly exceeded 3.5%.

Chart 5The latest reading is 5.8%, so it is well above the 3.5% threshold. Based on this historic relationship between consumer sentiment, stock prices and inflation, it's pretty important for the inflation rate to soon begin its downward trajectory. If it fails to do so, equities and sentiment are likely to suffer the consequences.

Chart 5The latest reading is 5.8%, so it is well above the 3.5% threshold. Based on this historic relationship between consumer sentiment, stock prices and inflation, it's pretty important for the inflation rate to soon begin its downward trajectory. If it fails to do so, equities and sentiment are likely to suffer the consequences.

Good luck and good charting,

Martin J. Pring

This article is an updated portion of an article previously published on Monday, August 16th at 7:53pm ET in the member-exclusive blog Martin Pring's Market Roundup.

The views expressed in this article are those of the author and do not necessarily reflect the position or opinion of Pring Turner Capital Group of Walnut Creek or its affiliates.