The title of this article might make you believe that we are bearish on the market. If you have read some of the last 200+ articles in this blog, you know that we do not make forecasts or guess about the direction of the market; we follow our rules-based trend following model...period. While we are not necessarily bearish on the market, it does seem like nearly everyone expects a bear market to occur in the not too distant future, even if they don't explicitly state that. Let us explain.

All over the financial media we see articles and stories about the future returns expected from the S&P 500 over the next 5 to 10 years. These articles usually discuss stock market valuations based on long-term average P/E ratios or the cyclically adjusted price earnings (CAPE) ratio, and note that when valuations are high, as they are currently, expected future returns from stocks are low. Most analysts are estimating the future returns of U.S. stocks to average only about 2% a year for the next 10 years, and possibly even have negative returns on a real basis, after considering inflation.

What these articles imply, but never address explicitly, is that in order to average only 2% a year for 10 years, you must have a bear market crash during that period. Why? Because the S&P 500 rarely returns 2% in a year, and definitely isn't going to start having low returns each year for 10 years. Instead, the way it will average down to 2% a year for 10 years, is it will have "normal" returns (5%-30%?) for most of the 10 years, with maybe 1 or 2 large negative years – this is the bear market that everyone's analysis bakes in, but they don't address.

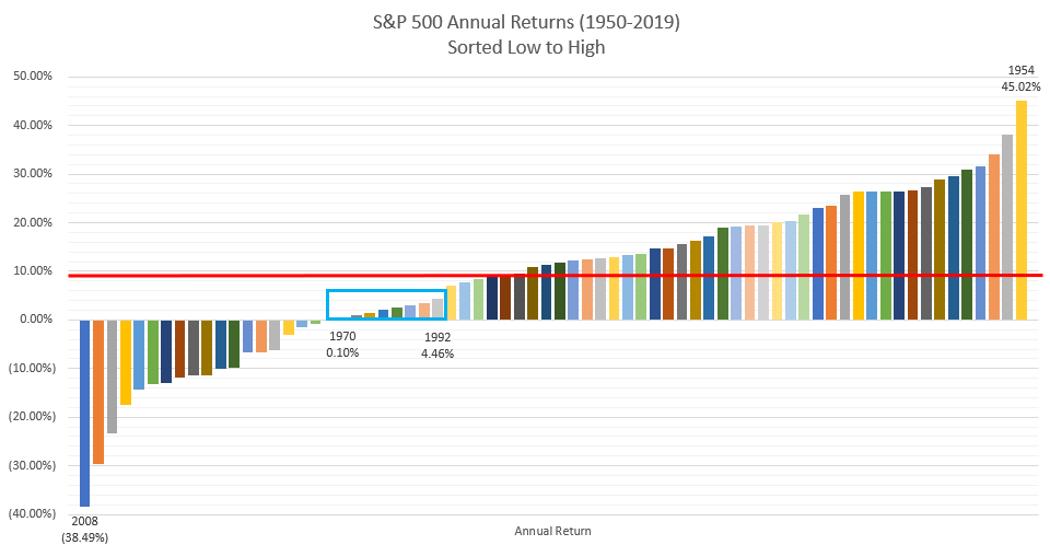

Chart A shows the annual returns of the S&P 500 since 1950 (70 years of data) sorted from the lowest return year (2008, -38.49%) to the highest (1954, +45.02%).

Chart A

The blue box near the middle are the years where the S&P 500 returned between 0% and 5%, which is about what most people are forecasting for the next 10 years. There were only 8 years out of 70 where the S&P 500 had low returns in that range, and none of them were consecutive years. Doubtful the next 10 years are all going to fall in that range. The red horizontal line is at 9.14%, which is the simple average over these 70 years. 38 of the years were above the average, 13 years were below that average but still above 0%, and 19 years saw negative returns.

There are any number of ways that the next 10 years could average 2%. For example, there could be 9 years that return the average of 9.14% and then 1 year that loses 44.5%. If the 9 years of positive returns are above average, then the bear market year will need to be lower than -44.5%. You get the picture.

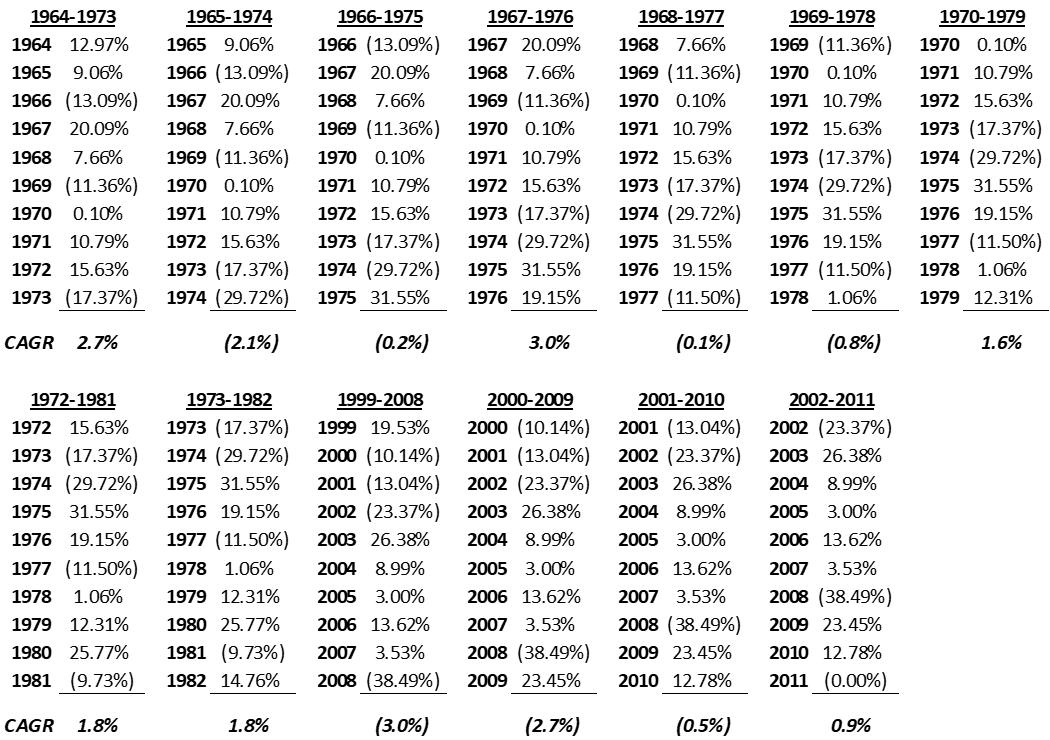

How has it looked when these low returns have happened in the past? Table A shows all of the 10-year periods in this 70-year history that saw a compounded growth rate of less than 3%.

Table A

All of these periods in history saw at least 1 or 2 large negative years and all periods covered at least 1 bear market (1973-74, 2000-02, 2008). I guess it's always possible that the U.S. equity markets just meander sideways for the next 10 years earning between 0% and 5%, but I think that is pretty unlikely given it has never done anything close to that in its history. The more likely outcome, if the analysis of P/E and CAPE ratios is to be believed, is there will be at least 1 bear market in the next 10 years, and I think the authors who publish this type of analysis would agree – and should probably at least acknowledge that their analysis implies a bear market is coming.

If you agree that a bear market will probably occur within the next 10 years, and that is the driver of these low expected returns – how should you invest for this future?

If you choose to be a buy & hold investor (could be active or passive), then you are accepting a 10-year period with very little investment growth, and maybe none at all, after inflation. You'll get all the upside as the bull market continues, but will get all of the downside too. Hopefully you'll actually be able to "hold" through the downturn to get the benefit of an eventual recovery (most end up selling on the way down) ...and that your time horizon is sufficiently long enough to withstand those lost years. Most passive investors are probably hoping that the next bear market is still many years away, but eventually it will have to be dealt with, and of course what you hope for has nothing to do with what will actually happen – hope is a lousy investment plan!

If you are an active value investor and choose to remain on the sidelines as long as the market remains overvalued – you could be waiting for a very long time. Valuation metrics are a terrible timing indicator as they can stay elevated for long periods, and the market can easily become even more overvalued. Most value investors are probably hoping for the bear market to happen soon, as this presents the buying opportunity they're waiting for. Again, hope is a bad plan. No one knows if the next bear market is going to start this year or in nine years. Can you imagine being under allocated to U.S. equity markets if we don't end up having a bear market for another three or five years, or longer? Everyone around you will be touting their stock market gains while you are labeled a perma-bear who missed participating in what could end up being one of the great bull markets. If you manage money for clients, they'll be the ones missing out on the upside and you'll probably be fired before too long.

Tactical strategies, like trend following, that are willing to move to defensive positions in bear markets can provide the best solution. Trend following is the one approach we know of that can be deployed at any time during a market cycle and still achieve good results. If the bull market continues for one, or two, or five more years, trend following will allow for continued participation in some market upside. All the while, a rules-based trend following approach, with defined stop levels, provides protection against the downside of an eventual bear market. There is no silver bullet investment approach though – as we've discussed in these articles before, trend following is of course subject to whipsaws, and struggles in sideways choppy markets (Feb-Apr 2018 is a recent example). Those times can be frustrating; however, bear markets can be devastating.

Maybe you don't think the P/E or CAPE levels matter or that they are not predictive of low future returns. How about the business/economic cycle, or the debt cycle? Does any of it matter anymore? Sitting today near the end of the 11th year of a bull market, I don't see many arguments that this can continue for another 10 years...at some point, I think you have to expect that this bull market will come to an end. If you think there will be another bear market in your investing future, we think trend following is the single best approach to navigate that bear market, especially since the timing of it is unknown to everyone.

Dance with the Trend,

Greg Morris