Investors may have the blues right now because we find ourselves in another bear market just 17 months after recovering from the prior one. The last bear market started on 2/19/2020 and ended on 8/18/2020 and was the 6th worst bear market since 1927 (of the S&P 500 Index and predecessor indices), dropping over 33.9% at its lowest point. It was however the quickest bear market by far, taking less than 6 months from when the selling started before the S&P 500 attained a new all-time high.

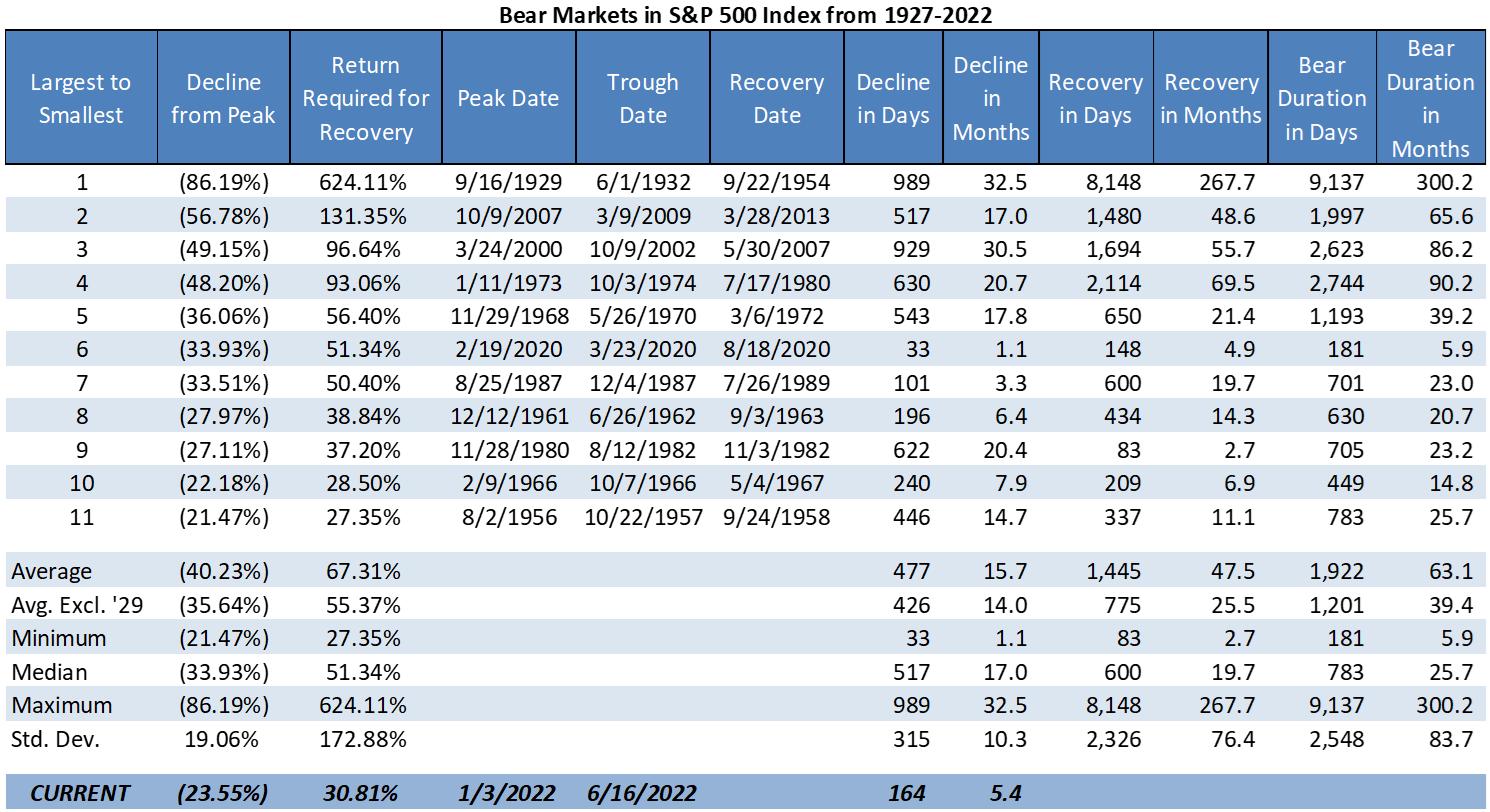

Below is our updated bear markets table showing the prior 11 bear markets ranked by the magnitude of their decline from largest to smallest. The bear market that we currently find ourselves in is tracked in the bottom row "CURRENT" and shows that we've dropped over 23.5% so far over the last 5.4 months; January 3rd being the prior peak in the S&P500.

We've mentioned in previous articles (Trend and Trend Plus – Drawdown | Dancing with the Trend) and will reiterate here – the magnitude of the drop during bear markets isn't the only factor that destroys the wealth of investors – it is also the duration of the bear market; the length of time it takes the market to fully recover from being in a bear market. If you are in a mild bear market that lasts a few years and must make monthly withdrawals from your account to pay for retirement living expenses, the long duration of the bear market can do more to destroy your wealth than would a higher magnitude bear market that recovers much more quickly. The amount of withdrawals made during the bear market greatly exacerbates the impact to your portfolio; this impact was also discussed in a prior article (Old Bear, New Trick | Dancing with the Trend).

If we exclude the crash of 1929 for being an extreme outlier in the data, the average bear market drops 35.6% (magnitude) and lasts 39.4 months (duration) – that's more than 3 years and 3 months! The bear market of 2020 had close to average magnitude but its duration was so short you could blink and miss it. If you didn't keep up with the financial news during that time and only reviewed quarterly account statements, you had only one quarter where things looked bad (1Q20), by the next quarter you were down less than 10% (2Q20), and during the third quarter you went back to all-time highs (3Q20). That is not a normal bear market by any stretch and investors should not look at that as an example of what we're going through today.

The current bear market already has duration about as long as the one from 2020 and it looks as though we are still heading down. Nobody knows where the bottom will be and how long it will take to get there, and nobody knows how long it will take to recover from the low point either! If someone tells you that they "know" how this bear market will play out, you should ask for their verified track record on all their other market guesses – they likely have made hundreds of market calls in an effort to be correct on just a few! Not the type of person that should be trusted with investments. We would also not make a bet with investment capital that the Fed can orchestrate a soft landing for the economy, i.e., bringing inflation into normal ranges without stifling the economy. Their track-record on this is abysmal.

Since we feel strongly that nobody can reliably predict when bear markets will occur, how far down they'll go, how long they'll last, or what will cause the next one (or much of anything else regarding financial markets), we use rules-based trend following to avoid the constant need to make guesses about the future. We don't have to guess and hope to be correct about the market, economy, Fed policy, inflation, corporate earnings, government policy, or anything else. We agree that these things likely matter to stock market performance, but not that you can "solve" the riddle of the markets based on these forecasts to make sound investment decisions. Additionally, the behavioral aspects of investing and that humans are notoriously poor decision makers when faced with uncertainty also supports the folly of trying to invest based on forecasts, predictions, or guesses about the future.

Instead, we follow rules that react to what the market is actually doing – that's it. If the market is moving up, we try to participate, but when we detect breaks in the uptrend and the market moves through our stop level, we sell out of equity positions and stay defensive to protect clients' capital. The mere existence of bear markets (not what causes them or how bad they will be) is one of the reasons we prefer rules-based trend following to other forms of money management. The fact that bear markets exist and that trend following does a good job of avoiding them, along with our expectation that bear markets will continue to occur in the future, is what makes trend following a very useful approach to managing serious money. Over full market cycles we've found trend following can deliver significant returns while suffering much lower volatility and drawdowns than the broad market, ultimately compounding capital at a higher rate for investors – that should be "good news" for trend followers.

Buy and hold approaches to investing (either active or passive forms) that maintain fairly constant equity exposure during bear markets don't employ any real risk management techniques. The only way one attempts to lower the risk of these strategic asset allocation portfolios is by mixing in larger allocations to bonds to hopefully de-risk the equity allocation. Sometimes this works and sometimes it doesn't, ultimately the bond exposure is usually a drag on returns while providing very limited downside protection. In 2022 the bond allocation in most strategic asset allocation portfolios is suffering almost as much as the equity portion. In a rising rate environment this is likely to continue.

Instead of using bonds to de-risk, our trend following approach is fully tactical in that it can move from being 100% invested in the stock market to being 100% defensive with no exposure to the stock market; and our defensive holdings can vary from cash to gold to short and intermediate Treasuries – assets that often perform very well during equity bear markets and market environments that see panic selling. We believe that this form of risk management, being tactical and using stops to get out of the way of bear markets, is much better for investors as large drawdowns are far too difficult for most investors to tolerate. Investors always think they can hold their positions thorough any level of downturn and make it out the other side. Bear markets prove time and time again that investors abandon their investment plans at various levels of drawdown and then have no plan on how to re-allocate once the bear market is over. Remember, buy & hold only works if you can accomplish the "hold" part.

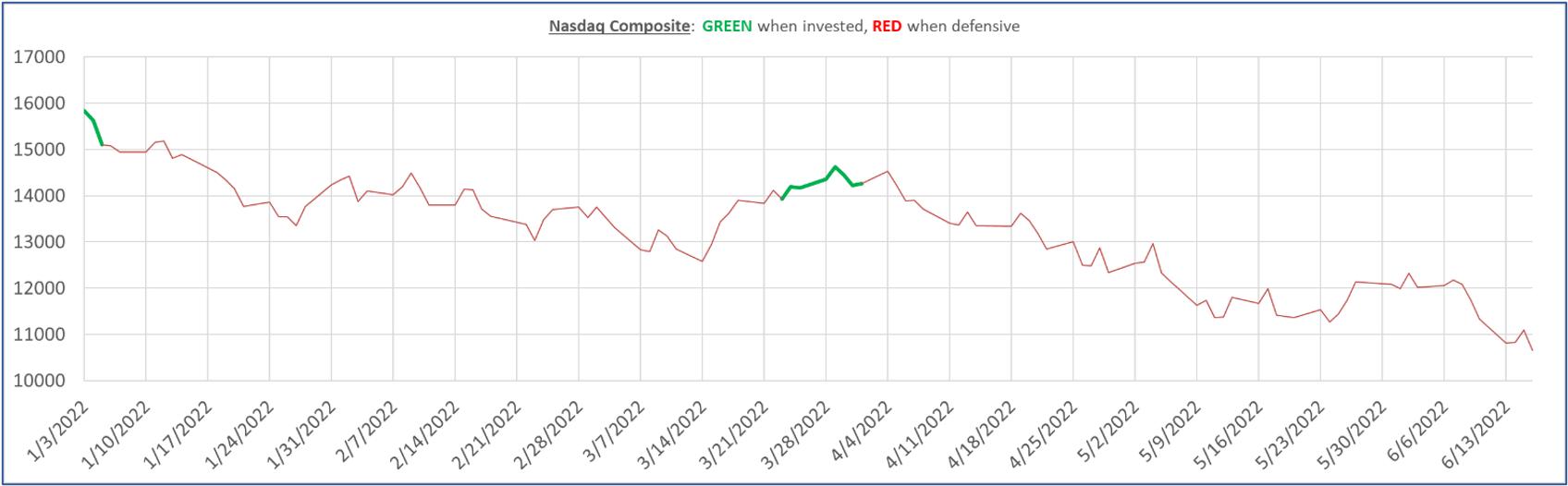

Below is the 2022 view of the Nasdaq Composite chart we've shown often that illustrates the times that our trend model has us invested (green) and the times that it has us defensive (red). Previous articles show the same chart for 2021, 2020, and older periods. You can see from this chart that our model got us defensive very early in the year, and other than a quick trade at the end of March, has been defensive all year – avoiding the devastation to wealth that comes with bear markets.

The defensive positions have had mixed results so far this year, but avoiding the market this year with the move into defensive positions has provided a significant amount of outperformance for investors.

Making the same comparison since 2020 when we had the last bear market, and even though 2020 and 2021 provided strong returns in the benchmarks, the power of not losing in the bad times keeps trend following ahead, and all along investors experienced much lower levels of drawdown during the two bear markets.

Admittedly, 2021 results were not great on their own and the large underperformance to the market was difficult to tolerate for many investors; however, we are not investing with a focus on any single year or specific timeframe. Many investors get impatient with the results during the ho-hum years like 2021 when trend following is underperforming the market. We've discussed this in many prior articles. Losing sight of the long-term results that trend following can provide, and of their long-term goals for investing, causes investors to chase performance and abandon trend following to move into the group of funds or strategies that just had the best recent performance – selling what they owned and don't like anymore to buy what they wish they had owned – in essence, selling low and buying high. Last I checked that was a fairly poor investment plan, and sadly professional advisors are guilty of doing this for their client portfolios, too.

We think it is better to understand what market environments will cause underperformance in trend following and accept that "bad" as a tradeoff for the "good" that it provides at other times, i.e., don't give up on trend following in times of underperformance to assure you receive the benefit it provides in times of outperformance, namely during painful bear markets when other strategies and investment approaches are doing so poorly.

We strongly believe that all clients should have an allocation to trend following and other tactical strategies for the good news they deliver to investors during bear markets.

Dance with the Trend,

Greg Morris