I spent a good portion of my Wednesday webinar, DecisionPoint LIVE! discussing "Bear Market Rules". Given the Dow has now officially entered a bear market (50-EMA cross below the 200-EMA) and other indexes preparing to follow, I thought it would be an excellent time for a refresher for DecisionPoint faithful and a teachable moment for novices. We have been living by "Bull Market Rules" for years, I'll talk about them as we go along. More than rules, these are a 'frame of mind' that every investor and especially technical analyst should understand.

I spent a good portion of my Wednesday webinar, DecisionPoint LIVE! discussing "Bear Market Rules". Given the Dow has now officially entered a bear market (50-EMA cross below the 200-EMA) and other indexes preparing to follow, I thought it would be an excellent time for a refresher for DecisionPoint faithful and a teachable moment for novices. We have been living by "Bull Market Rules" for years, I'll talk about them as we go along. More than rules, these are a 'frame of mind' that every investor and especially technical analyst should understand.

As I stated above, DecisionPoint uses the relationship of the 50-EMA and 200-EMA to define bull and bear markets. When the 50-EMA is above the 200-EMA, we consider the market to be in a long-term bull phase, and vice versa. This is an important definition because we will want to bias our medium-term analysis in favor of the long-term trend. As a reminder, we will often state that, "Bull (or Bear) market rules apply." In the general sense, this means that ambiguous medium-term situations will most likely resolve in the direction of the bull or bear phase, so we should perform our analysis and draw our conclusions with that in mind. In the Dow Industrials ($INDU) chart below, you can see some of the most recent 50/200-EMA crossovers. Each arrow represents new bull and bear market phases.

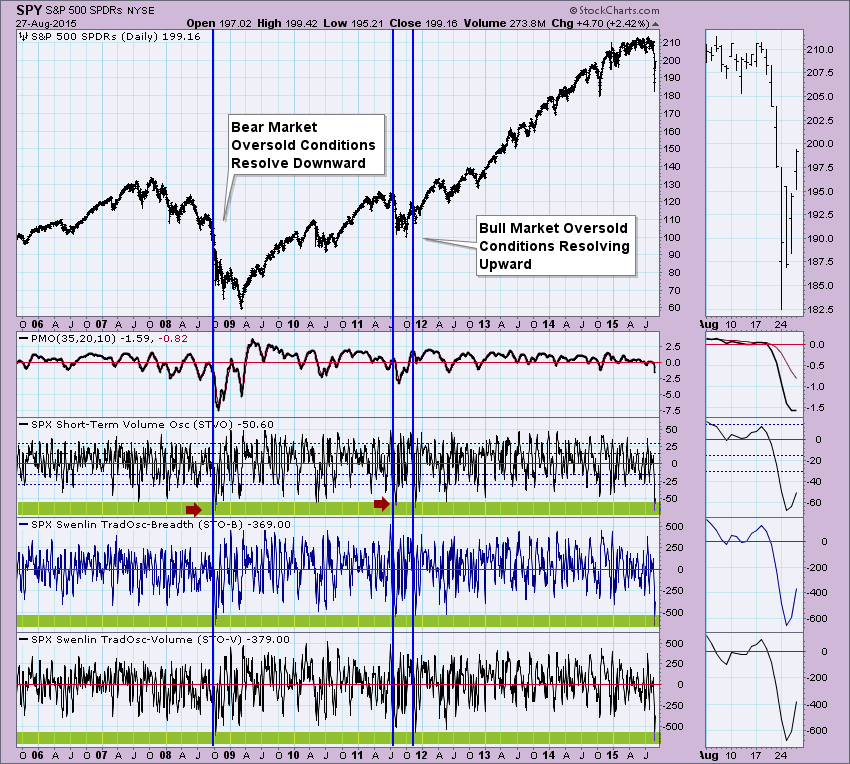

More specifically, let's look at the common occasion when the market is overbought or oversold. In a bull market oversold conditions are seen as a buying opportunity and will usually result in a rally to relieve the condition. When a bull market becomes overbought, it is not usually cause for concern, because corrections from these conditions are often small, and sometimes the market will continue to rally, while the overbought conditions are relieved internally. The opposite is true with bear markets. Overbought conditions are most often a setup for a new down leg, while oversold conditions should be considered as being "thin ice," not a solid base of compression from which a rally will emerge. For example, buying into bear market declines is a dangerous practice. This is where the phrase "catching a falling knife" comes in.

I've been watching the oversold conditions on some of our short-term indicators. In general, these have been profitable to buy into, but notice when the market switches from bull to bear, the last bear market extremely oversold readings preceded a small rally in 2008 but still resolved downward.

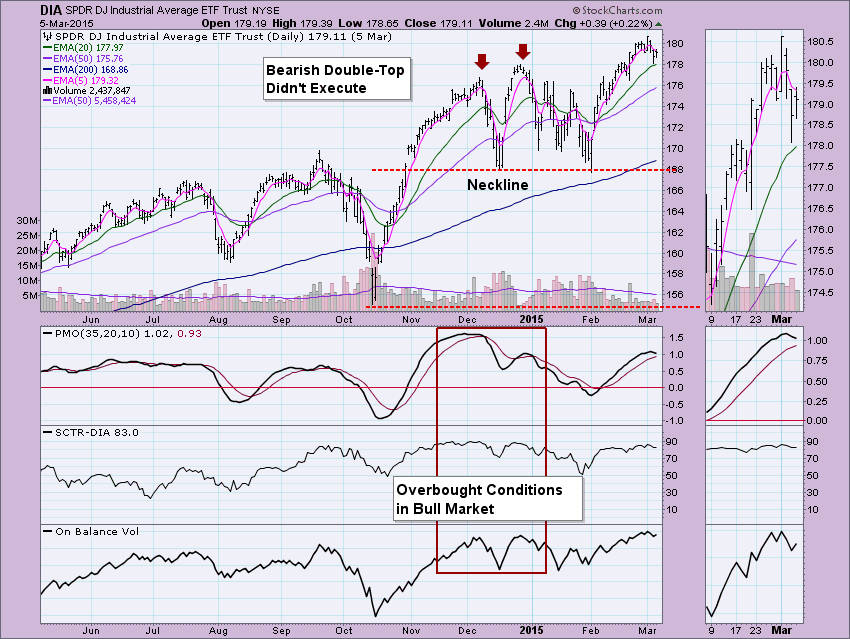

Chart formations are another area where the long-term market bias should be considered. For example, a bearish head and shoulders pattern in a bull market is less likely to execute by violating the neckline, or, if it does execute, the decline may abort into an upside reversal before price reaches the minimum downside target. The same would be true of a bullish reverse head and shoulders in a bear market. Below is an example of a bearish double-top on the Dow Industrials ETF (DIA) that didn't properly execute within a bull market. In addition you can see that the overbought conditions turned out to not be much of an issue.

Further, the amount of confidence we have in the long-term bull/bear signal should be influenced by whether the 50/200-EMAs are converging or diverging. When the EMAs are diverging, it means that price is in front of both EMAs and they are confirming the strength of the move. When the EMAs are converging, it means that price is either between the EMAs or is running behind them. In either case, converging EMAs are a sign that price is performing in a direction opposite of the crossover signal. This is exactly the situation we are currently in on the SPY. We are technically in a "Bull Market" because the 50/200-EMAs have not had a negative crossover; however, these EMAs are converging meaning that price has a long-term bearish bias.

Conclusion: We should temper our expectations of technical information based upon the long-term trend of the market. In a bull market, expect bullish outcomes. In a bear market, expect bearish outcomes!

Technical Analysis is a windsock, not a crystal ball.

Happy Charting!

- Erin