A 'transition phase' - from a market rising on the back of a presumption of a series of Fed rate cuts, this would indeed would seem to be what's underway. Both a rapid decline and partial rebound yesterday, followed by today's smart rally as the Fed Chairman further clarified the possibility of a mini-rate cut series as ongoing, certainly were embraced as contributing to the expected rebound. As we also suggested, there was a subsequent 'fade' last night (after the rebound); it really is impossible to say how extensive it would have been absent that tweet on China regarding additional tariffs to be imposed effective September 1. But, in any event, all of this is within the context of our ongoing summer forecast (for new members that was from late May: up into early-mid-July, then rotational corrections with a defensive bias for some weeks if not months, barring for-sure successful breakthroughs on the trade-front; more so than the Fed).

Now, whether the morning rebound was just a "grinding higher" move based on better backdrops to a muddled message the Fed Chairman "sort of" gave Wednesday, or appreciation of better times ahead (it's not that), the parsing of every word was telling us that the Fed has engaged in the dreaded race to the bottom, as much as, of course (we think), they'd prefer not to, and the market clearly telegraphed its affection for the addiction of low rates. This of course takes a different slant as we envision greater trade-based impacts from higher tariffs (forcing the Fed to actually cut more than they'd like, definitely is more bearish for the U.S. economy if fully carried out). Play it? Well, do realize any morning (or tweet) indicating a trade deal and it's off to the races again, at least temporarily. Hence, remain nimble, even if defensive.

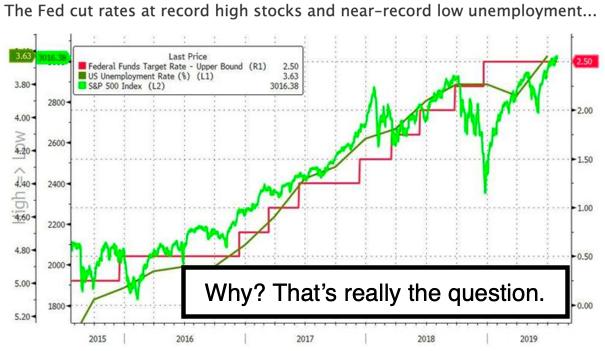

The economy is in decent shape, but not to justify higher price levels on its own; thus, the response by Wall Street (including today's expected rebound back over S&P 3000 before la deluge) tells you that this market is addicted to low rates and, in fact, is increasingly dependent upon that trend. Be cautious, as history is replete with serious consequences if that prevails too long.

Hence it's a dangerous game. Our idea was that, if a market breaks, one should fade *not* the decline, but the ensuing rebound as it begins fading. A couple trading fades reflected that on Thursday, as one downside move got lots of traction, but, knowing it was associated with tweets on China, tends to reinforces hesitation to actually short the market (especially *after* news).

Conditions are not what they should be for normal investing, and they've for sure been distorted by the craving for low-rate based justification for buying. Normal should be: if the economy does well, the market does well. But that isn't a realistic view of the market here; even if we're mid-cycle with respect to the economic cycle. We're not, however, on the eve of recession, whether we're actually facing that, or (more likely, in my opinion) we've been in it for a year-plus and readying to exit a sluggish economic environment assessed for over a year now, regardless of a series of S&P moves in both directions. Of course, a doubling-down on trade conflict can prolong the agony though.

That matters, because this is one of the moments where you have markets excessively dependent on monetary ease and less focused on actual results in business, and thus 'hooked' on low rates and easy money. Generally, we're retaining our view of United States as more attractive than other regions of the world, and we would be very careful about excessively tying our policy on rates to what's going on globally. However, that's what the Fed's doing.

In-sum: Chairman Powell would be more accurate if he embraced Boston's Rosengren's belief that no cut was appropriate, although after Thursday as the President doubled-down on trade war, the cut looks insufficient (they're really not correlated; it just looks that way to the casual observer, I guess).

Or, the Chairman could have said the United States can't offset the supply-chain competitive challenges a slew of foreign countries present, especially China, and that, regardless how low we took rates, even if the Fed cut a full point and the market rocketed to a higher level, it would NOT have anything to do with improving revenue for the nation or profits for most businesses.

It's a fiscal policy concern that cannot offset the efforts by the monetary (the Fed) authority. That would be candid, but would not please Wall Street. But not pleasing Wall Street (or the President) may be the lesser-risk to bending in the direction of politics or counter-forces that press the Fed (hence, that's a debate as to whether the Fed was influenced by those influences).

If one has to focus on addiction and trying to get the S&P higher regardless of what happens further out, well, that's what those arguing for lower rates in a sense are saying: move the market higher regardless of financial damage or even chaos that may ultimately be enhanced by virtue of such policies. "A little pain now, or more pain later" might be a simple way to summarize this. Perhaps Mr. Market, with its forecast Summer corrections, will judge.

Bottom-line: Besides the pattern conforming to the idea of a rebound to S&P 3000+ and then a fade, it's really more involved and was hanging tough until the President's tweet, which (importantly) was composed with all the major advisors in the room (Mnuchin, Kudlow, Navarro and Mulvaney). That says it's really policy, not simply one of Trump's often-spurious tweets.

What's hard to define is whether the playbook is fundamentally different, as trade tensions are more likely to escalate than not. Whether the market, which focused primarily on central bank liquidity, might find that a President willing to "tank" trade more significantly, might see a silver lining, in that Fed pressures to cut rates even lower would be hard to resist if the US ventures more deeply into recessionary conditions that predate for well over a year; a condition I've indicated since March of 2018 irrespective of S&P swings.

For the moment, these movements pound any budding "green shoots" solidly back below the surface; but that too can change *if* President Xi comes back to the table. That could be exactly what the tweets today are mostly about; if the President really believes China might be waiting for results from a new election. He probably senses a double-benefit; lower stocks but forcing Fed rate cuts (historically not smart, but I'm not his advisor; and Kudlow agrees, in my opinion, with my views, but I don't think he's able to prevail presently and goes along because this is his dream job and to a degree he'll conform); all as it gives China an incentive to stop horsing around and make a real deal.

Conclusion: It matters that the Chinese believe the U.S. will persist just as long or as far (in terms of tariff increases) as needed; whether or not the Fed has to cut further. It emphasizes a bias toward ease, because the economic mix (just ask retailers) actually changes going forward in a negative way. It's not the 1930s, but it's the global economic magnitude of the United States that matters now, and the implication is that it would be tougher for us years from now, so it's time to bite the bullet and deal with this, whether or not it forces the world into a more bipolar economic set of spheres of influences.

We got our S&P rallies into early-mid July as anticipated and, with more drama, and as expected regardless, we've entered a roller-coaster period of correction and news-sensitive moves with a negative bias until such time as backdrops change. That includes getting the USMCA deal done, containing North Korea and avoiding war with Iran, while bringing China to a worthwhile deal that too many proponents (including the Apparel & Footwear group that very much was 'stunned' by my warning to them as keynote speaker in 1977 of what was coming) now those same groups bemoan loosing China for the cheap manufacturing (not corrupt, but done so long that they became dependent and sacrificed the genuine care for American workers by virtue of focusing a bit too long and definitely too broadly on offshore production).

A deal with China would both result in lifting tariffs and taking pressure off of the Fed regarding further cuts this Fall. The S&P would instantly soar, a bit more so if the S&P can significantly correct in the interim period.

Daily action - confirms the trade war with China is more elongated than the optimistic hopes, but the vocalization of trade negotiations, as well as FOMC pressures, combine as a disincentive to invest at high S&P levels.

If it is a systemic competitive environment with China, you'll see enduring as well as difficult adversarial competition compels broader diversification, which actually benefits many countries as they court U.S. firms seeking both new outlets and locations to diversify their manufacturing bases or sources.

I'm aware some think a trade conflict may last for decades. Well of course, if this isn't settled in an amicable way, it then becomes a situation transcending President Trump's initiatives. If so, then, several years from now, investors might actually look back and realize he (as odd as his style is) tried to undo the preceding awful trade policies (as he claims - and we called for - starting 40 years ago) but did so too late to do it in a smooth way that didn't cause lots of global disruptions.

I think the U.S. has given Beijing several opportunities to undo their policies somewhat, and they haven't responded other than their typical way, which is to promise a lot and deliver as little as possible. Now, what hits the markets next *might* be China disrupting Tesla's efforts in China (selling US-built EV cars pending their uncompleted factory) or trying to curtail Boeing orders (that latter is very tough for China, as they have their home-grown jetliner of intermediate range coming, but cannot "safely" rush it into service yet).

(Of course most of China's orders - bunched for purchasing power by their central government- were for 737 Max aircraft, for which availability there is non-existent for now; so perhaps Beijing will focus on that or try to push the orders into 787's. Airbus can't deliver more units either.)

Oh.. the Pentagon confirms it is reviewing the potential Contract Award to Amazon Web Services. That may be reopened to bids, as it is pending. The inference was that the White House asked the Pentagon to review it, but it's also the case that Amazon is one of the companies under-review by DOJ for possible antitrust action, whereas companies like AT&T and IBM, as well as Microsoft, are not.

The low interest rate environment has not delivered a "great economy" some have promised (or assessed as achieved), so you get a series of alternating positive and negative headlines. But all of this is at high levels, from which we have and continue to expect a rotating market of overpriced corrections interspersed by unsustainable revival rallies.

It depends on the '3-T's'

Now, yes, the pattern today was very close to what I spoke of last night with respect to the S&P, or even to the Semiconductors helping lead downside action. Now that Oil kicked in as well, that's not swell for any bullish hopes at the moment. Again, though all it takes is a reversal of stance by President Xi of China and a Trump tweet about a telephoned commitment and you for sure get a rally. But then they have to come through, such as what we heard about Soybeans last week that apparently didn't gel, and maybe that itself was something that (understandably) irritated the Trump trading team.

Prior highlights follow:

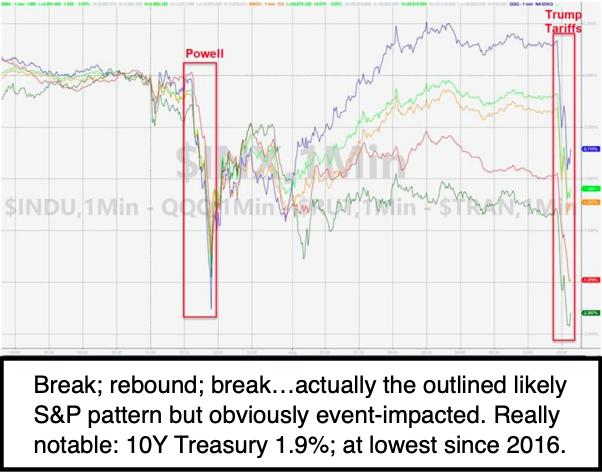

"This time IS different" - is a famous phrase that gets economists often into trouble (because it rarely actually is different) but, nevertheless, we actually heard that expression from the Fed Chairman regarding the nearly-universally-expected rate cut of 25 Basis Points today.

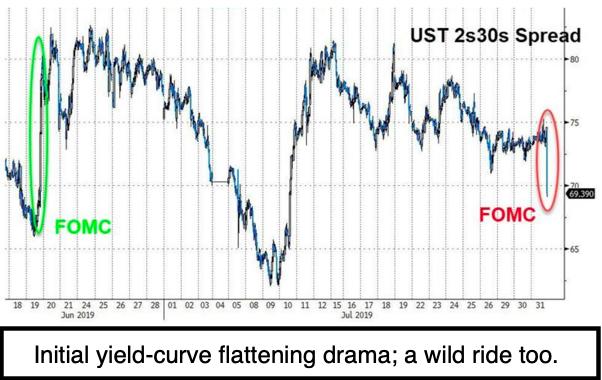

The Chairman simply indicated that today's 'cut' does not mean the Fed is committed to a series of cuts (hence the different take versus most history has shown), and the stock market freaked at that remark. That triggered a mid-conference 'clarification' that it depends on downside risks, which he's said are primarily coming from abroad and affecting manufacturing here, as well as fixed investments in the U.S.

*Why* the market would be spooked by the Chairman indicating objectives in a mid-cycle adjustment to policy really shouldn't ruffle everyone. That's why he took that as a "not necessarily one-and-done" cut by virtue of his ensuing remarks, and of course the S&P came off the lows - but still fairly heavy.

All these are issues I have already addressed about an "investment crowd," by any measure, as overly focused on monetary policy as the backstop for a very overpriced Senior Index stock market; one that doesn't have a benefit of a trade deal yet either. Wall Street thinks they want lower rates? Not if, in fact, they want profitable companies priced based on profits, not fiction like the buyback craze or liquidity movements. Low-rate countries for *too long* tend to be slow growth countries. That's fine (we enjoyed that in the 1950s) but the S&P now is priced for something better than slow growth. Also, the exodus of trading desks relates in-part to passive investing, but also to the inability to hedge against significant interest rate moves, as none really are. It is as if Wall Street wants a steady passive long-term horizon. Fine, but it really doesn't work that way - just look at the Emerging Market exchanges.

Anyway, all this contributed to an expected perfect formula for some sort of retrenching, but today it was algorithmic responses to "one-and-done / but maybe it's not" .. giving you down-and-then "better" but, at the same time, not great. The Fed Chair conveyed what he could do; totally rational discussion (regardless of what the President may say about how he should have cut a half rather than a quarter, which would have gendered a lot of opposition). Remember: two FOMC members dissented from any cut at all.

This Chairman wants to see what the economy is doing in the Fall, and that, by definition, becomes data-dependency. So the U.S. is not exactly evolving into the "Global Central Bank," but it is absolutely moving *relatively* by trailing those bankers in excessive ease. What's needed is the "Fiscal front," and it is tough because of the global developments weighing on the US economy.

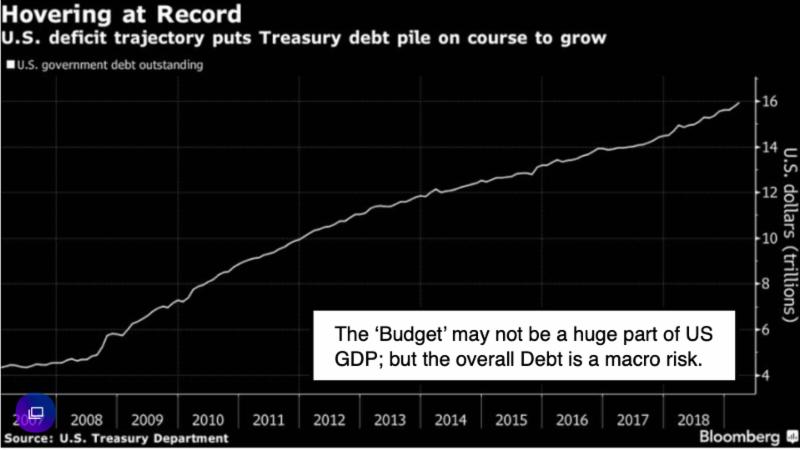

In-sum: The Chairman did not focus on the inflation undershoot (and their goal there is to further devalue our currencies, which none of us should in fact favor; although we know they need to articulate a way to keep rates on the low side, lest everyone start focusing on the big issue: Debt Service.)

Nobody on the FOMC favored a 50 basis point cut, incidentally. Powell said it might not be a series of cuts; hence, the Chairman had to walk back that comment. However, the market should not feel entitled to get what it wants. The reaction affirms that it's really monetary policy supporting the S&P extension, NOT anything truly related to valuations. In fact, just a little detail: the S&P valuation levels are a higher multiple of GDP than has historically been the case; in a sense, that's a component of blowing bubbles. That also is a reason a prudent approach would disdain urging an aggressive lowering of rates or other stimulus efforts by the Fed at this point.

Late today, the President tweeted notes that essentially support the idea of engaging in matching the race to the bottom embarked on by other Central Banks. On this topic, I have to support the Fed, not the President, as we do know what that kind of approach has done to the countries that embraced it. The Fed is not going to succumb totally to this trend toward NIRP (negative interest rate policies) and, in my humble opinion they need not do so. I'd like to believe the President knows better (and that his tweet was merely political), but I don't know that. As to Powell, he didn't (as one said) "stick the landing" as if this were gymnastics; hence, the Fed then miffed preparing for "what's the next act" and he sort of missed that opportunity. What's the metric that might require yet-another rate cut? (The answer might be lack of a trade deal).

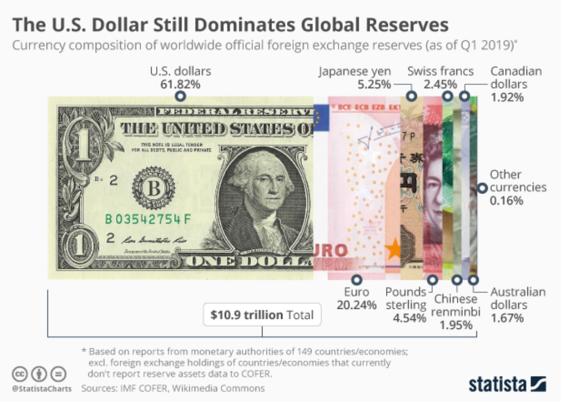

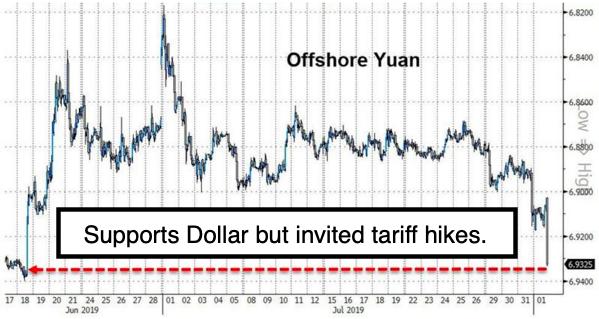

Besides, it is evident the United States was, and remains in, a better relative position. That matters. It's also why the Dollar is firm, and that, too, is a positive, not a negative. (Emerging Markets and currencies remain softer, at least until the Dollar softens; for now, the Dollar has yet to stall, but it certainly is entitled to do so soon.) Overall, as always, my view will be what seems logical, not what might be politically accommodative. I actually believe that's what the Fed expressed today as well. Uncertainty prevails with what the future brings in variable areas like trade, but, for now, stair-steps lower (markets not rate moves) is the ongoing expectation over the weeks ahead. That's not a surprise.

Bottom-line: The Fed can't deflect rising negative rates abroad; simmering trade difficulties (not as bad as previously he said, and that's what I've said incidentally; hence, not quite as much of an impact). The global deflation is a spongy global situation, so a slight rate cut doesn't really provide insurance, even though that's what markets would like to imagine.

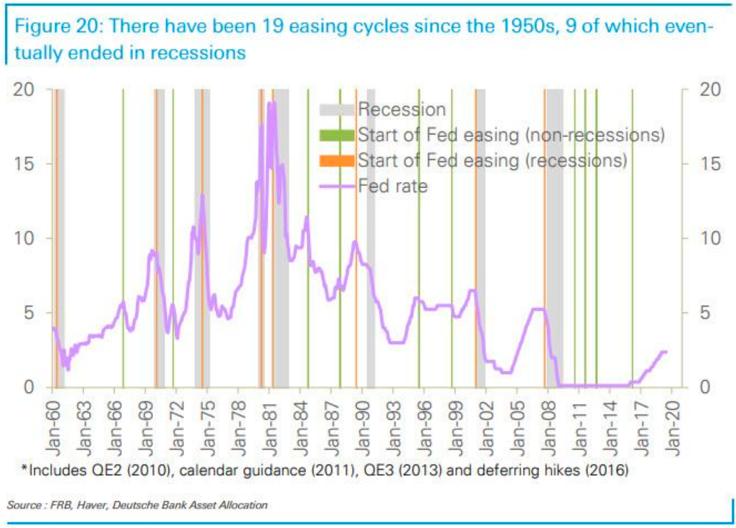

We all presumed a cut was coming, and I for one (saying it wasn't needed at all) leaned in favor of them taking just a quarter-point, which is what they did while traders were too ridiculously optimistic about expecting even more. It might be worthwhile nothing the Futures market still suggests as many as 2 more rate cuts before the end of this year (depends on conditions, with lack of clarity about criteria for the next decision by the Fed). There's no hint of inflation or anything else demanding dramatic Fed moves, and I concur with that.

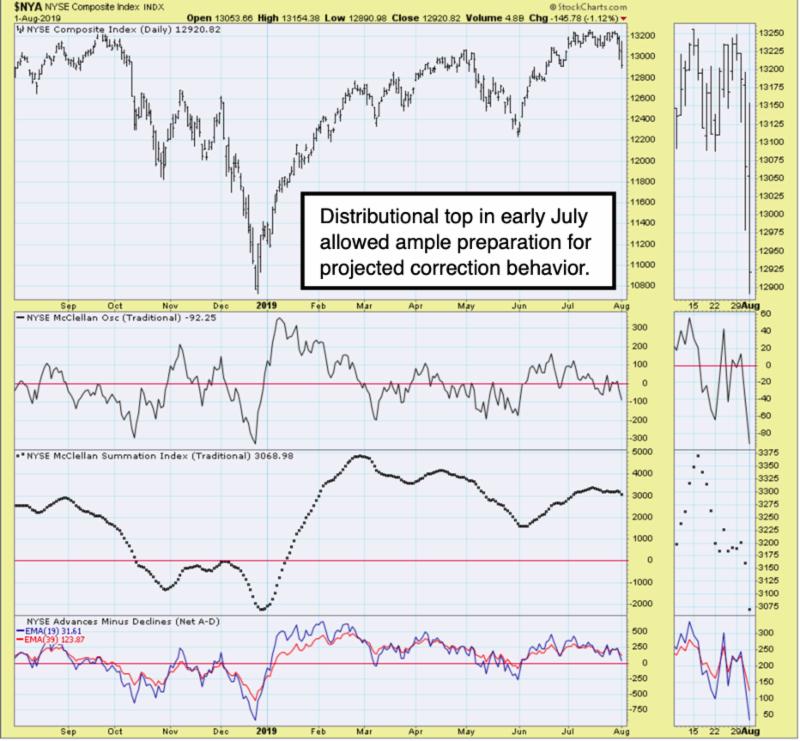

This leaves traders in a sort of ambiguous state of "watchful waiting" for now, both with respect to Fed policies and a trade deal with China. Everything is pending; it is as I've outlined, and therein lies the set-up for a rougher near-term S&P. The market "headline sensitivity" prevails, rotating corrections continue and upside for the S&P is almost nonexistent for the moment.

(Macro) action - was accommodative to expectations on two fronts. First, talks in Shanghai were "constructive" but didn't merit being described as "productive" with no clear statement drafted by both sides at the gathering's end. What was said was that they'll meet again in September, and that's essentially the can-kicking expected - cooperation, but no announced progress as of yet.

The Fed meeting notably has nobody (at least at the FOMC) calling for a 50 Basis Point cut, clearly indicating that the implied rationale for more cuts has to do with desires by certain analysts or politicians, not economics in terms of real needs. The Chairman was at some pains to clarify that there is no predetermined next move on the part of the Fed, nor should there be. In that realm, his emphasis on global slowing reinforces their stance.

Much of what you saw today (in a time-frame for which we're looking for the S&P to have topped anyway with the slight moves over 3000) was reactive, or even algo-driven trading. It all was exacerbated by the Fed commentary, but there I had suggested last night we might get a "one-and-done" summary by virtue of the Fed not committing to further cuts. The market traders that want more for now have been and remain entirely unrealistic.

The Chairman did not address the "term structure" or much about unwinding the Balance Sheet, other than saying it would end (for now) a couple months earlier than the Fed originally intended. The Chairman did suggest a slower job growth environment, but we've already evidenced that, and nobody with a lot of experience would expect a nominal cut here to change much at all.

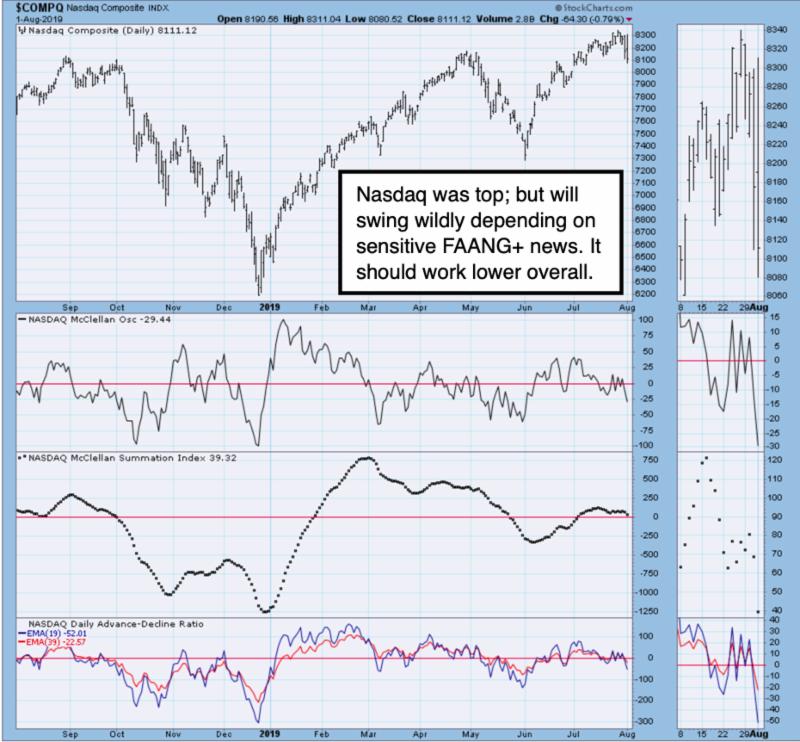

After the close, Qualcomm missed estimates and lowered guidance. That, too, conforms to the heaviness Semiconductors generally are experiencing, which is a normal characteristic for the sector after a huge run, given how much the trade sluggishness impedes their vaunted moves into new technology. A lot of that was already discounted by preceding advances in those big stock leaders, of course; after correction, a number of them will advance next year (ideally) and a larger number of already-heavy small-cap techs will do so as well.

Times are never different (or rarely so). Having a degree of fear about the Fed here probably restrains euphoria and, ironically, deflects the worst possibility, which would be a parabolic thrust to the upside.

Without conditions stimulating a new degree of euphoria (virtually assured by virtue of today's tempering by the Fed), you evolve in this anticipated or corrective phase looked-for to unfold in the post-early/mid-July timeframe. The Fed should not be implored to express foresight about future actions by the Board, especially based on their historical missteps in that regard. I do believe the Fed should be data-dependent (more so than this time) and I do not believe they should be following the lead of the BoJ and ECB.

Those central banks have contributed to prolonging their instability and the destruction of price discovery, as they've removed a degree of risks in the minds of money managers, which is a risk itself. I suggest that this implies (as talked about that the other day) confidence in sort of a "smooth" monetary policy allowing heavier equity allocations without an intellectual discussion of unintended consequences. The Fed should tune-out politics, lest the consequences of well-intended moves and ideas not end well.

For investors, the good news is that, absent euphoria, you evolve rather than crash the market, and that's conceivably within context of a longer favorable cycle. Of course, the problem with the future of today's challenges is that there are variable outcomes. Even there, the Fed Chairman's comment that trade is now "simmering" supports my view that we've been in that uncertain state of affairs (with trade) long enough, that companies have moved on as far as planning (to a degree), and that mitigates the impact of the delay with getting a formal agreement between the U.S. and China.

Thursday could well see negative early action, with a rebound thereafter as likely - but all this should still yield to heaviness as August's evolves. Did the President set-up the Fed to be the fall-guy if things don't work out? Maybe, but we were and are in for a meaningful market correction regardless. Plus, the expensive big-cap stocks constitute a dangerously-crowded trade.

Convoluted policy perspectives - have been fairly obvious for the Federal Reserve; with tugging and pushing from current and former Fed officials and of course the White House pressures, which they say are ignored (actually, it is more realistic to say that they are taken into account, but primarily because rates can really be nudged higher without the impact on debt service becoming a lot more visible). Maybe it's like a cardio treadmill; the pace continues if you do; but get off of it and there's a palpable letdown, at least initially.

However, it's not only monetary policy debates that are convoluted. Lots of areas of concern to markets are either in turmoil, or the proposed solutions that would enhance the future are themselves a series of convoluted proposals.

That includes the trade dealing with China (and the President's tweets this morning, which *probably* are part of the negotiating approach); implications for currency movements (besides the fundamental changes) resulting from a hard Brexit, and even the nowhere-near-resolved geopolitical issues, that range from comparatively non-impactful deliberations about Venezuela, to a hostile Iran (now contemplating naval exercises with the Russians, as if it's a way to offset growing U.S. & U.K. Persian Gulf fleet reinforcements) and a not-so-secret underhanded dealing with untrustworthy Saudi Arabia (both it and Iran are also intractable opponents at this point, but that may change).

Of these, what happens with China is most pertinent to the market, as early shakeouts on Trump's tweets evidences, and, as you know, I felt matters lots more than a nominal "pushing on a string" move by the Fed tomorrow. From an overall standpoint, the market doesn't like uncertainty, and none of this is likely to be meaningfully resolved regardless of knee-jerk responses that are sold-into should they even go in a perceived favorable way.

This morning, I looked with envy at the huge bridge rotated into position in China and pondered *why* it has to be China that innovated construction to a "why didn't I think of that" new advanced level. Whether high-speed rail or MagLev or EV, they have taken technologies developed in Germany or the U.S. (typically, but occasionally other countries) and refined them to get the capability of constructing and activating capabilities and use faster than the originators of modern infrastructure concepts.

Since the U.S. is behind, but is the leader of basic technologies; we should learn from this and implement far faster than how we are slowly-but-surely updating our own transportation and other systems. We have built bridges and then rotated, but not on that scale, and we need to do it better. In Central Florida, the I-4 corridor has been under massive reconstruction for a couple years and the progress is slow, the construction techniques terribly traditional and the number of accidents and detours resulting from it incredible.

The I-4 case alone shows constructing fly-over interchanges and then "rotating" them into place should be the norm, not the rare exception. Yes, it takes less man-hours, but China has unlimited labor and yet they do it in an advanced way. There is no excuse for Americans to suffer so contractors can drag it out for what seems like interminably long projects. Just look at Laguardia Airport. Not only is it being constructed far below the renderings presented for approval (from facilities to materials) but they didn't even sensibly set-up an expeditious way to exit the airport to catch a taxi or Uber or, heaven-forbid, include a link to the City's subway system. Rarely now do you see a foreign major airport without such a link. The worst albatross of them all, Berlin's so incredibly-delayed Brandenburg Airport, had the rail link and station built before the terminal, which will finally open next year (they say). (And yes, it will become a major European hub and property prices in Berlin will rise.)

It's not our usual subject, but I felt like touching on some of this tonight as we await the decisions from Shanghai and the Fed.I'll add that it can be done right here in the United States. In Orlando, the new International Terminal and the huge multi-modal hub for vehicles, buses and local and high-speed trains has already been built, before utilization, and without putting passengers through a gauntlet like the contractors do with the highways or airports, typically. (The trains get a boost because they're both city and private; city for the Sunrail locals; and Virgin Trains, partially funded by Virgin U.K, running from Miami / Fort Lauderdale up to Orlando and then to Universal and Disney. It's a partnership that was arranged despite presumptions that high-speed does not work in the USA. It does, just in certain markets, like the Northeast corridor, which shamefully doesn't have it yet. Then there's the much less "modern" NYC airport links, with what they have - the path to Newark or Airtrain to JFK is really outdated.)

Speaking of trains - the risk to this market is of "derailing," and that's what everyone is trying to avoid, but I suspect the best they can hope for, after the requisite knee-jerk responses, is a series of corrections for the big-caps and, ideally stabilization or even gains in some of the already-corrected smaller cap stocks. Whether it's Apple, Harley-Davidson, Ingersoll-Rand or even i-Robot, you have lots of companies rotating some of their manufacturing or supply-chain dependence out of China and into other countries, not just with the known other Asian countries (like Vietnam and India), but also Mexico, Central America, Brazil and elsewhere. Many believe this diversification is absolutely a must. Will the Chinese see this and now come through?

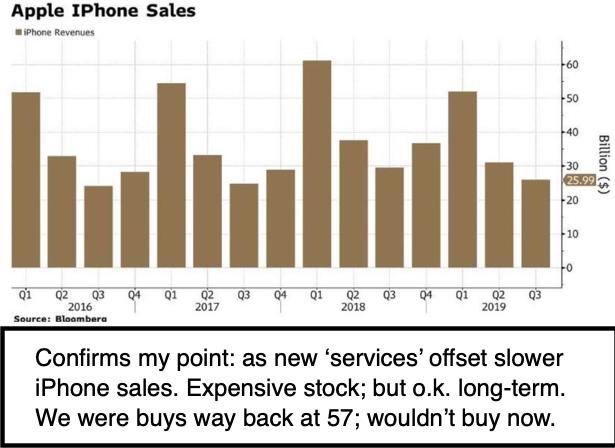

In the "Daily Action" section below, I'll touch on after-close earnings reports. I do want to mention the confusion (and it's still not clarified) by reports that Apple will or will not shift production of the expensive Mac Pro to China. It is too simplistic to discuss the inability of profitably making a computer here in the U.S. when they are basically talking of an expensive assembly using the same components whether it's put together here or over in China. Dell and IBM assembled computers here for years, and Apple has with some as well, so it's a bit ridiculous to talk about. It's actually the iPhone that requires lots of labor and an enormous workforce that would be hard to replicate here.

We're going to have real problems if we don't address technical training and compensating better in this country, as it really does involve capabilities, not just "labor." When the recently-bolstered $15/hr jobs get automated away in time, what will large numbers of unskilled/semiskilled workers do for jobs? Bringing manufacturing back to the US like this was the 1950s became just a pipe dream in recent years, whereas it was doable when I called for it so often 20-30-40 years ago; even before Trump took-up the challenge too. It's not just about wages - it's about skill and efficiency as technology can move us to a robust manufacturing process, but only if we focus on it politically.

Despite our country's divisions (sometimes running in political circles), goals the President states regarding jobs makes sense, but there is not a magical solution for it, and so far insufficient policies to implement needed capacity to make more things here. But this can change. My single word: education. Also, perhaps realizing free trade is fine, and localized manufacturing is a good (if not essential) goal to have and necessary to avoid pitfalls of major powers focusing only on services as they abandoned manufacturing. Ask the U.K. (now in the throes of Brexit and not dissimilar challenges too). I've warned of this risk of abandoning building-in-America for decades.

To the point, it may be lip service, but I would rather Tim Cook publicly state his intention to keep producing the Mac Pro here than to say nothing at all. If nothing else, we have got to get away from a dangerous reliance on China.

In-sum: It's not the turbo-boost of a Fed cut (at these levels) that will really make a difference, nor is it the Fed that's held back the economy. It's been a sluggish domestic environment, uncertainty at the corporate planning level, and the consumer debt that has continued to climb amidst a soft economy.

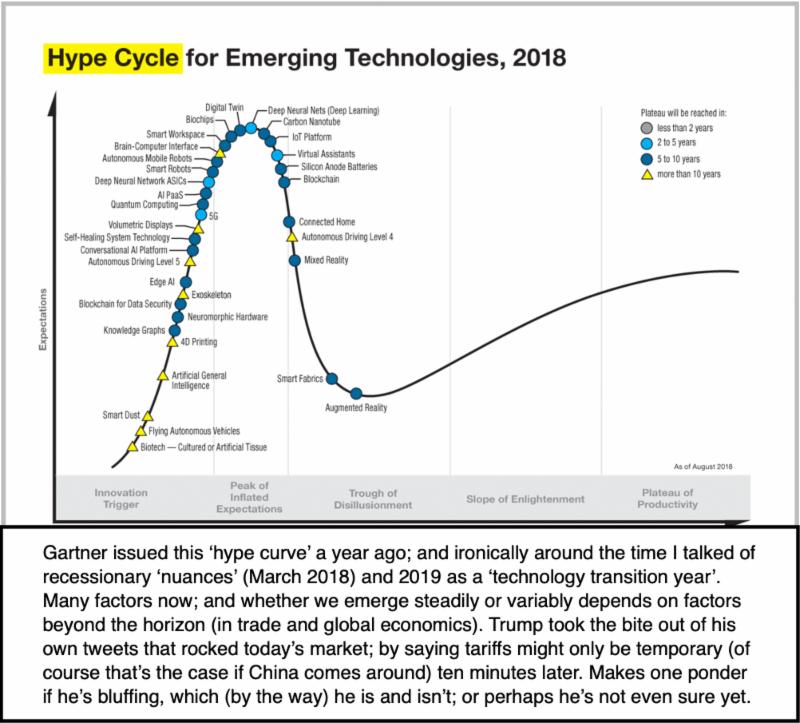

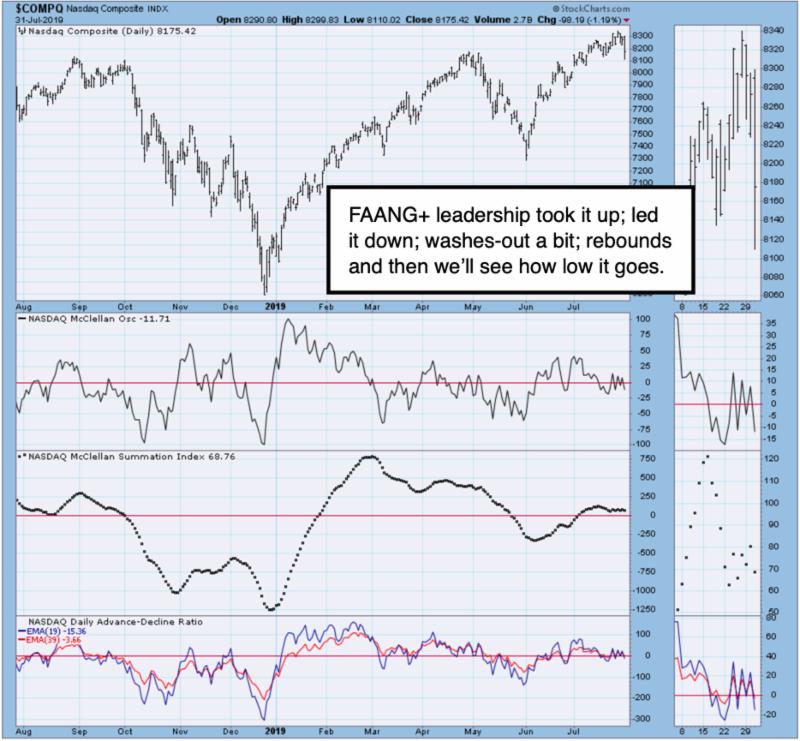

The market beat-up the stocks patiently waiting for the technology-transition year to be migrated through, while the mainstream industrial stocks haven't done much. Leadership has concentrated in a small handful that you all know well (FANG+). Since infrastructure and heavy construction (which a modern infrastructure program would utilize, not to mention export markets that contracted during the trade stand-off with China) haven't adequately yet reflected future growth, they can help stabilize the market when on defense, if there's no geopolitical accident (war with Iran comes to mind) and if there is a deal with China. Again, convoluted issues that we all understand, but, for now, remain unsettled in many ways.

Whether it's Autos, Media, robotics, autonomous controls, infrastructure or even healthcare (with speculative biotech always shifting around) or certain resource areas, there are lots of sectors with potential, but it takes a deal with China for now, because CapEx is the concern that puts a floor, but is a ceiling if there is no palliative agreement between the economic powers.

Bottom-line: The world has structural issues that can impact global growth (an expanding issue in China which should push a deal forward, if the U.S. doesn't come to a view that letting China contract or withdraw a bit might be in our interest... I suspect not, as it would only be temporary, and we'd lose the ability to temper their Brick & Road initiatives later on; not to omit the tendency to move away from the Dollar, closer to Russia, and so on). I believe it is preferable to make a deal and hope the U.S. actually wants it.

Nominal GDP being paid down to a level that allows domestic growth is yet another discussion, but it matters. The Fed wants to right-size yield curves, because the hiking into a yield-cut inversion last year was a mistake, as we'd noted at the time. The Fed needs to add velocity so the consumer can stay alive (though it's excessive and, somehow, people don't focus enough on the rates they are paying or simply the excessive use of consumer credit - but it too is another subject).

We have the multiple expansion in the S&P now, and we need earnings to follow-on with *actual growth* next year. That really would enhance forward guidance and justify a higher market next year ahead of elections. That, by-the-by, is the opposite of Goldman's view (sort of) because they talk of a higher price environment in the face of guidance or estimate cuts for next year. It's a bit of a charade, because a lot will start to depend on political trends, not just China or the Fed, as we migrate into the election year. Normally it would not, but alternatives are not symbiotic to a higher S&P.

Equity markets adhered to generally outlined expectations. Wild cards (like China) remain in-flux, while reverberations still flow.

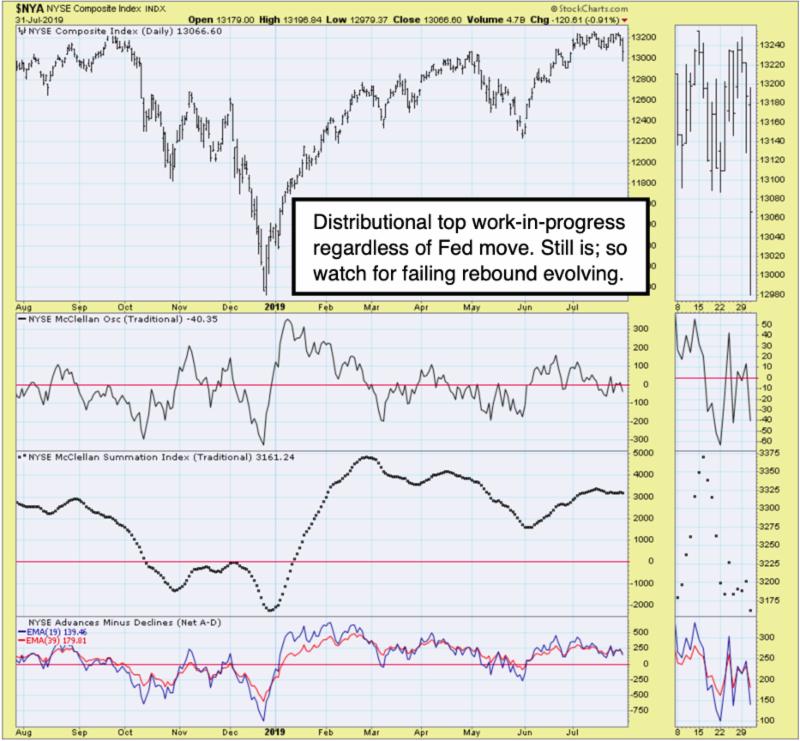

Discretion remains the better part of valor, following forecast thrusts above S&P 3000; there are expected to be limited or unsustainable S&P forays higher, given preceding rallies, as you know, were viewed as likely to occur through June into early-mid-July, while the backdrop became sort of neutralized.

Enjoy the evening,

Gene

Gene Inger