Market Recap for Wednesday, April 6, 2016

Healthcare (XLV) and energy (XLE) had huge days on Wednesday as our major indices rose throughout the day and finished on its high. Strength was seen across nearly every sector with only the defensive utilities down slightly. The best performing aggressive sector - technology (XLK) - rose .98% and ranked the XLK fourth in sector performance on the session. The hesitation of money to rotate toward aggressive areas of the market remains a key factor in my current cautious approach to trading. I discuss this in greater detail in the Current Outlook section below.

Despite the huge 2.69% gain in the XLV, there remain significant challenges ahead for the group, particularly on the longer-term weekly chart. Check it out:

The XLV closed at 70.31, but there are two obvious reasons that healthcare could struggle in the 70-71 area. First, there's a down channel in play off the July 2015 highs. Remember those weekly negative divergences that warned us of trouble ahead? Here was my June 2015 article that discussed the potential troubles that healthcare faced at the time.

The XLV closed at 70.31, but there are two obvious reasons that healthcare could struggle in the 70-71 area. First, there's a down channel in play off the July 2015 highs. Remember those weekly negative divergences that warned us of trouble ahead? Here was my June 2015 article that discussed the potential troubles that healthcare faced at the time.

Also, the selling really began in 2016 from the current level. The entire stock market was extremely weak in January and the XLV was no exception. Now we've rallied back to that level. Finally, the 50 week SMA currently resides at 70.42. It seems unlikely we'll simply go blasting through, but we'll see.

Energy's strength resulted from the bounce in crude oil prices ($WTIC) as the price of crude rose 3.20% and for a second consecutive session, ending the two week decline from $42 per barrel to $36.

Pre-Market Action

Initial jobless claims came in slightly better than expected and there were three solid earnings reports out this morning as you can see below in Key Earnings Reports. Still, that's done little to change the direction of U.S. futures, which are down this morning.

Asian markets finished mixed with China's Shanghai ($SSEC) down 1.4%. In Europe this morning, the major indices are down fractionally after the German DAX recovered off 9500 price support. Watch that level closely. Failure to hold it would not only represent the likelihood of further technical selling in Europe, but it could also trigger more intense selling here in the U.S.

Current Outlook

The buying of treasuries is defensive in nature and sends treasury yields lower. Generally, when an imbalance of money is directed toward the bond market, it's because traders are anticipating economic weakness ahead. Hence, the lower rates in an attempt to stimulate economic growth. That same weak outlook tends to hit the stock market in negative fashion and the S&P 500 falters. Therefore, it makes sense that treasury yields and the S&P 500 move in unison.

Below is a chart showing the performance of both the 10 year treasury yield ($TNX) and the S&P 500 over the last 10 months:

As you look at the above chart, both the TNX and SPX appear to move together during the majority of uptrends and downtrends. The red vertical lines show two periods - July 2015 and currently - where there's been a significant variation. We saw what happened in July/August. The bond market had it right and the S&P 500 played catch up, tumbling in August, a few weeks after the TNX had done the same thing.

As you look at the above chart, both the TNX and SPX appear to move together during the majority of uptrends and downtrends. The red vertical lines show two periods - July 2015 and currently - where there's been a significant variation. We saw what happened in July/August. The bond market had it right and the S&P 500 played catch up, tumbling in August, a few weeks after the TNX had done the same thing.

The recent drop in the TNX from 2.00% to 1.75% while equities ignore this warning sign has me justifiably worried. As I always say, there are NO guarantees with the stock market, but my risk sensors are on high alert. This downturn in the TNX is supported by the similar selloff of banks ($DJUBK), and the drop in relative ratios that measure defense vs. offense - like the XLY:XLP (discretionary vs. staples), TRAN:UTIL (transports vs. utilities) and RUT:SPX (Russell 2000 vs. S&P 500). These are all signals that question the sustainability of the current advance in U.S. equities.

If you remain on the long side, I would simply suggest you keep your stops in place. Just in case.

Sector/Industry Watch

Consumer staples (XLP) has been one of the strongest sectors in 2016 and over the past year has trailed only utilities - by a fractional margin. It's easily outperformed its consumer discretionary (XLY) counterpart. A big reason for the strength here has been distillers and vintners ($DJUSVN), which have gained 23.79% over the past 12 months. Constellation Brands (STZ) has seemingly reported better-than-expected earnings results quarter after quarter, driving prices higher in this space. On Wednesday, the DJUSVN made another big breakout as STZ reported exceptional quarterly results. Check it out:

Momentum remains strong and Wednesday's breakout signals the likelihood of higher prices in coming days and weeks.

Momentum remains strong and Wednesday's breakout signals the likelihood of higher prices in coming days and weeks.

Historical Tendencies

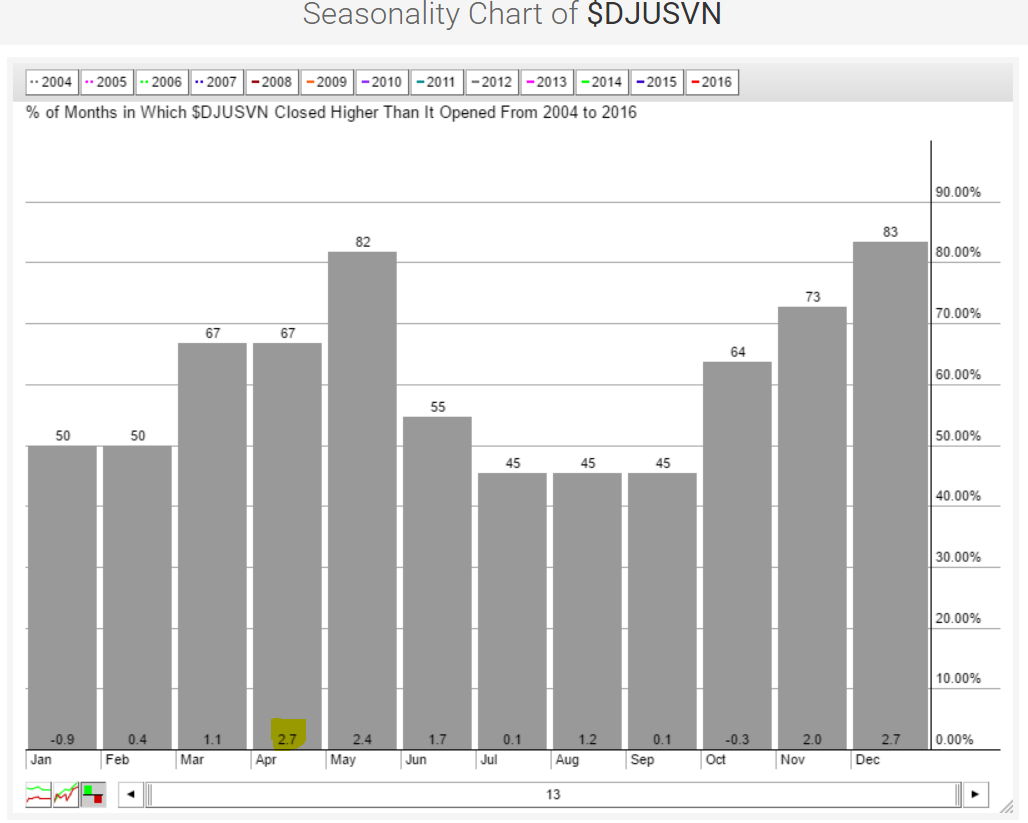

Due to the breakout in the DJUSVN, as highlighted above, it makes sense to look to see if there are seasonal patterns that favor the bulls as well. Take a look at the performance of the DJUSVN over the twelve calendar months:

Interestingly, the breakout is occurring in April, which is tied with December for the best calendar month performance for the group over the last 13 years.

Interestingly, the breakout is occurring in April, which is tied with December for the best calendar month performance for the group over the last 13 years.

Key Earnings Reports

(actual vs. estimate):

CAG: .68 vs .58

KMX: .74 vs .70

RAD: .07 vs .06

Key Economic Reports

Initial jobless claims released at 8:30am EST: 267,000 (actual) vs. 272,000 (estimate)

Happy trading!

Tom