Market Recap for Tuesday, November 22, 2016

You can't keep the bulls down right now, it's that simple. Yesterday, leadership turned to consumer discretionary (XLY, +1.19%) and materials (XLB, +0.61%) as small caps led a surge that took all of our major indices to all-time highs across the board. Both the XLY and XLB hit new highs as well. The latter benefited from hesitation in the U.S. dollar ($USD) as recent strength in the USD had squashed gold mining ($DJUSPM) and mining ($DJUSMG), which have fallen 6.44% and 1.87%, respectively, over the past month. But steel ($DJUSST) has risen 29.54% over the same period to lift the sector. I wrote in October about the historical strength of the DJUSST during the fourth quarter, and especially during November. Check out the historical tendencies section below for a reminder of this seasonal strength. The good news? December is historically strong as well, so the move higher may not be over just yet.

Here's a look at the XLB and XLY breakouts yesterday:

The red dotted lines highlight prior closing price resistance and clearly both the XLY and XLB exceeded those closing highs on Tuesday. The key to the sustainability of bull markets is (1) the rotation of money into aggressive areas and (2) wide participation. Seeing two more sectors breaking to fresh highs is very bullish as it puts more and more stocks on a buy signal. It's difficult for the bears to regain any control when most stocks are on buy signals and there's little expected volatility.

The red dotted lines highlight prior closing price resistance and clearly both the XLY and XLB exceeded those closing highs on Tuesday. The key to the sustainability of bull markets is (1) the rotation of money into aggressive areas and (2) wide participation. Seeing two more sectors breaking to fresh highs is very bullish as it puts more and more stocks on a buy signal. It's difficult for the bears to regain any control when most stocks are on buy signals and there's little expected volatility.

The Russell 2000 was particularly strong on Tuesday, gaining 0.92%, or more than double all of the other major U.S. indices. Small caps continue to be favored and this is their time of the year to shine historically. December's historical outperformance is quite evident.

Pre-Market Action

We've seen very slight profit taking around the globe overnight in Asia and this morning in Europe. The 10 year treasury yield ($TNX) is rising again - up to 2.35% this morning in early trade. Crude oil prices ($WTIC) are down roughly 1% this morning after finishing on Tuesday just above $48 per barrel.

U.S. futures are flat to slightly down as we prepare for the Thanksgiving Day holiday. U.S. markets will be closed on Thursday and open only until 1pm on Friday.

Current Outlook

This bull market rally continues unabated and there's a sense we'll never see a pullback. But we will. Profit taking is a necessary evil during uptrends. I'll use the S&P 500 as my example for what I'd consider to be a normal pullback within a sustained bull market. The most important level is long-term support. The S&P 500 has just broken out to a fresh high, closing above 2200 for the first time in its history yesterday. Let's take a look at the long-term weekly chart:

We're coming off a backtest of a trendline breakout, which also was close to a 50 week SMA test off the recent negative divergence. In my opinion, the negative divergence is no longer an influence here and the MACD is rising and accelerating once gain. Therefore, look to the rising 20 week EMA as the key support for this benchmark index. Currently, that's 2144 and is less than 3% from the current S&P 500 price. I don't believe we'll see a pullback greater than that.

We're coming off a backtest of a trendline breakout, which also was close to a 50 week SMA test off the recent negative divergence. In my opinion, the negative divergence is no longer an influence here and the MACD is rising and accelerating once gain. Therefore, look to the rising 20 week EMA as the key support for this benchmark index. Currently, that's 2144 and is less than 3% from the current S&P 500 price. I don't believe we'll see a pullback greater than that.

Sector/Industry Watch

The Dow Jones U.S. Apparel Retailers Index ($DJUSRA) broke out of a very bullish inverse head & shoulders pattern, suggesting a move over 1000 in time. Check out this weekly chart of the group:

Technically, strength here appears to be accelerating and the breakout is bullish, but one word of caution. December and January are below average months historically, so I'd be careful if neckline support is lost. In other words, just make sure you keep your stops in place. The overall market is solid. Therefore, I'm expecting more strength here but stay on your toes given the seasonal underperformance.

Technically, strength here appears to be accelerating and the breakout is bullish, but one word of caution. December and January are below average months historically, so I'd be careful if neckline support is lost. In other words, just make sure you keep your stops in place. The overall market is solid. Therefore, I'm expecting more strength here but stay on your toes given the seasonal underperformance.

Historical Tendencies

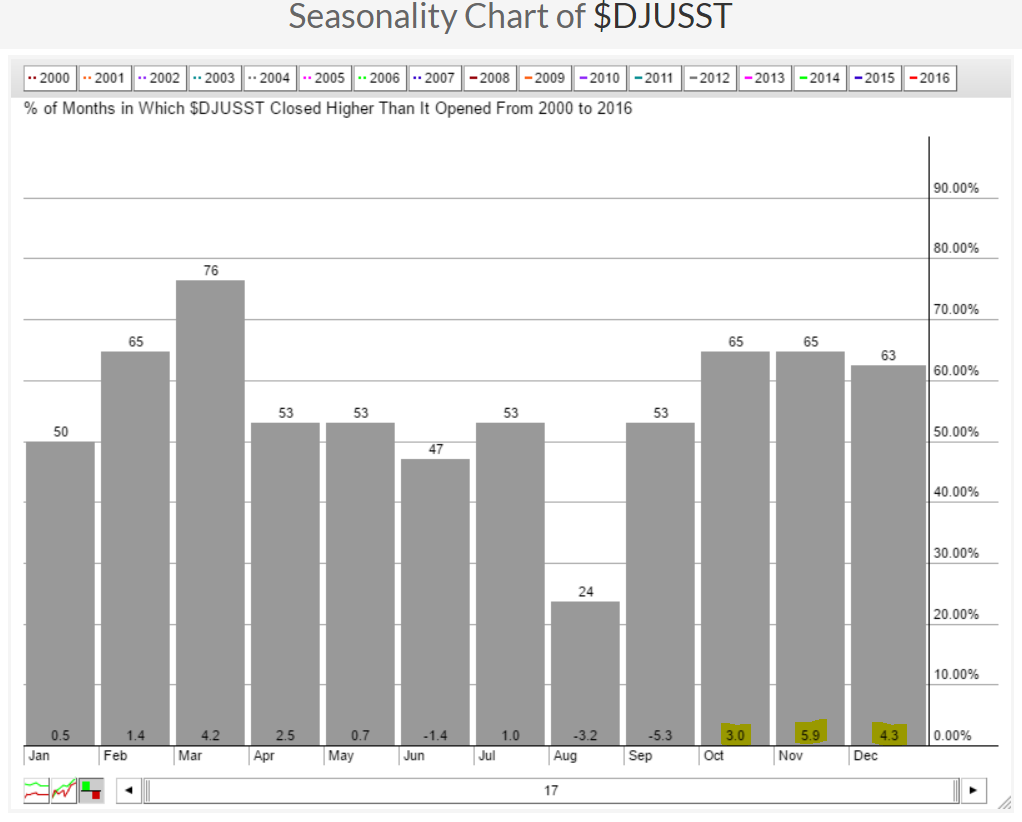

The Dow Jones U.S. Steel Index has produced excellent fourth quarter returns over the past 17 years and November has been the strongest month, averaging 5.9% returns in just that month alone. Below is a reminder of that strength:

December averages gaining 4.3% on the steel index so the parabolic gain in November may continue for awhile. The rising 20 day EMA should provide excellent support on any pullback.

December averages gaining 4.3% on the steel index so the parabolic gain in November may continue for awhile. The rising 20 day EMA should provide excellent support on any pullback.

Key Earnings Reports

(actual vs. estimate):

DE: .90 vs .36

(reports after close, estimate provided):

CTRP: (.08)

Key Economic Reports

October durable goods released at 8:30am EST: +4.8% (actual) vs. +1.5% (estimate)

October durable goods ex-transports released at 8:30am EST: +1.0% (actual) vs. +0.2% (estimate)

Initial jobless claims released at 8:30am EST: 251,000 (actual) vs. 250,000 (estimate)

September FHFA house price index to be released at 9:00am EST: +0.7% (estimate)

November PMI manufacturing index to be released at 9:45am EST: 53.5 (estimate)

October new home sales to be released at 10:00am EST: 590,000 (estimate)

November consumer sentiment to be released at 10:00am EST: 91.6 (estimate)

Happy trading!

Tom