Industrial Suppliers Have Had A Rough Week

Market Recap for Tuesday, April 18, 2017

The Dow Jones U.S. Industrial Suppliers Index ($DJUSDS) tumbled more than 6% on Tuesday as the group absorbed its second earnings shock in the past week. W.W. Grainger (GWW) came up short of its earnings expectations, then lowered guidance and traders punished the stock as GWW fell more than 11%. This drop followed a negative divergence in February and a steady decline leading up to its earnings report. Apparently, many folks were getting out ahead of the poor results. GWW joined Fastenal (FAST) with disappointing results that have weighed heavily on the DJUSDS as you can see below:

Industrial suppliers have fallen more than 11% over the past week and it's directly attributable to FAST and GWW, two of its larger components. I have to admit it's a bit of a warning sign about potential economic strength ahead when industrial suppliers are acting so bearishly with earnings and guidance a major problem.

Defensive stocks were again the leaders on Tuesday as consumer staples (XLP, +0.45%) and utilities (XLU, +0.23%) were the only two sectors that finished with gains. Biotechs (see more on this group below in the Sector/Industry Watch section) and pharmas both had miserable days on Tuesday as healthcare (XLV, -1.09%) lagged the other sectors.

Pre-Market Action

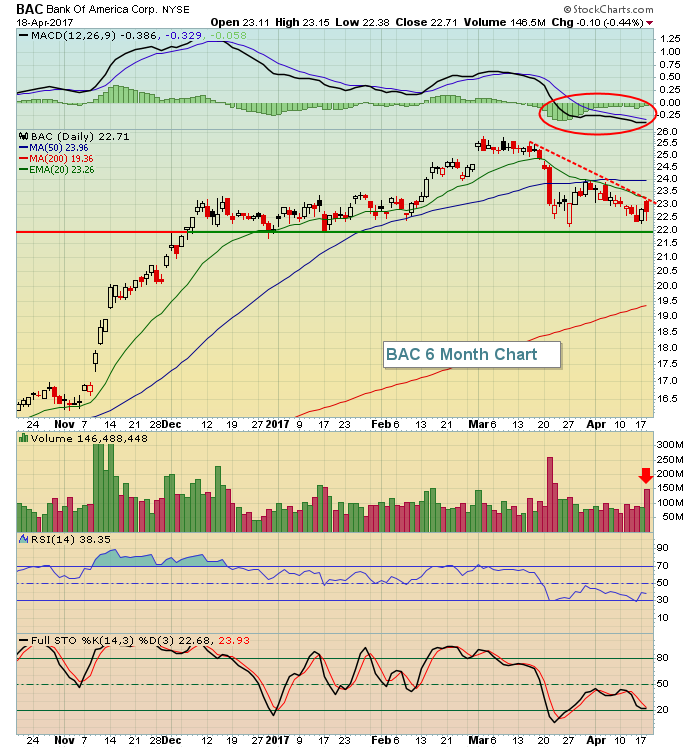

Earnings season is beginning to kick in and thus far I'm concerned. Results haven't been particularly bad, but the reactions to the reports have been technically disappointing. The banks immediately come to mind. Bank of America (BAC) reported stellar results on Tuesday in pre-market action and here was the reaction:

BAC needs to clear that downtrend line and its now declining 20 day EMA. Until then, I want to see 22.00 price support hold. BAC has been one of the best performing banks throughout the past six month rally and the last thing the group needs is to see one of its best performing components break down.

Currently, Dow Jones futures are pointing to a slightly higher open (22 points).

Current Outlook

The S&P 500 is struggling to break its downtrend lines since the March 1st top. In the very near-term, there's trendline resistance close to 2345 with the past week's intraday highs topping out close to 2350. That's the first level that needs to be cleared to improve the technical picture. But the bigger trendline in my view is the one established off the March 1st high. That intersects closer to 2370 currently:

To the downside, watch the March 27th low. That needs to hold or the 20 week EMA, currently at 2310 and not pictured above, becomes very significant support on the longer-term weekly chart.

Sector/Industry Watch

Biotechnology stocks ($DJUSBT) are hanging onto price support by a thread and this is the most aggressive part of the healthcare sector. We're seeing many signs of weakness and/or relative weakness in aggressive areas of the market and the loss of support here would simply add one more potentially bearish signal. Check out the support:

That green dotted line marks important short-term price support. While that support hasn't been broken yet, there are plenty of other negative developments. The DJUSBT has shown signs of slowing price momentum (MACD below centerline support) and has also seen its uptrend line break followed by a death cross (20 day moving average falling below 50 day moving average). If price support is lost, short-term caution is suggested.

Historical Tendencies

We're in the second half of April, which typically is much kinder to small cap stocks. Since 1987, the Russell 2000 has produced an annualized return of +35.87% from April 16th through 30th, while the first half of the month has produced an annualized return of -4.79%.

Key Earnings Reports

(actual vs. estimate):

ABT: .48 vs .43

AMTD: .40 vs .41

ASML: 1.12 vs .99

BLK: 5.25 vs 4.94

HBAN: .21 vs .22

MS: 1.00 vs .90

USB: .82 vs .80

(reports after close, estimate provided):

AXP: 1.28

CP: 1.90

CSX: .43

EBAY: .40

KMI: .18

QCOM: 1.05

SLG: 1.57

Key Economic Reports

None

Happy trading!

Tom