Market Recap for Monday, April 9, 2018

Once again, Monday was the tale of two markets. The first half of the day was quite bullish, but it was all for naught as sellers stampeded the bulls in the afternoon session. Our major indices finished with across-the-board gains so if you only tuned in at the close, you'd have been quite happy. But the entirety of the trading session was not nearly so bullish as the Dow Jones finished nearly 400 points off its intraday high. The S&P 500 traded within 2 points of its 20 day EMA before dropping 1.5% over just the final two hours:

The red arrows mark the recent failures at the declining 20 day EMA. While breaking above this moving average wouldn't necessarily end the two month correction, it would at least be a nice start. And continuing failures at this moving average will lead to major price support tests identified on the chart above at 2581 and 2532.

The red arrows mark the recent failures at the declining 20 day EMA. While breaking above this moving average wouldn't necessarily end the two month correction, it would at least be a nice start. And continuing failures at this moving average will lead to major price support tests identified on the chart above at 2581 and 2532.

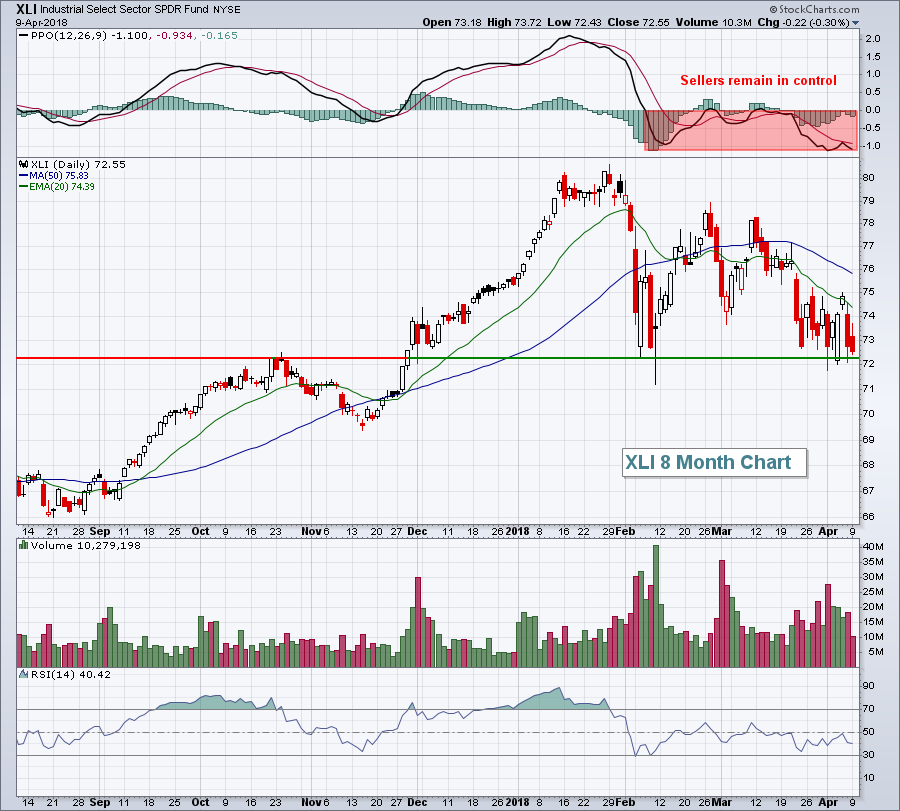

Industrials (XLI, -0.30%) claimed the honor of worst performing sector yesterday and actually closed at its lowest level since the 2018 swoon began. There's plenty of support, however, for the XLI to make a recovery. Check it out:

The 71-72 level represents solid short-term price support and I expect that to hold. Obviously, if it doesn't, it will embolden the bears and we could see swift selling resume. I expect to see the bulls make a stand at recent lows.

The 71-72 level represents solid short-term price support and I expect that to hold. Obviously, if it doesn't, it will embolden the bears and we could see swift selling resume. I expect to see the bulls make a stand at recent lows.

Consumer stocks also suffered on Monday as both consumer discretionary (XLY, -0.24%) and consumer staples (XLP, -0.06%) joined the industrials in negative territory.

Pre-Market Action

Despite an inflationary March PPI report, U.S. stock futures are on the rise and the 10 year treasury yield ($TNX) is barely higher, up just 2 basis points to 2.80%. Crude oil prices ($WTIC) are surging 2% to $64.68 per barrel. The energy ETF (XLE) has been threatening key price resistance at 69, so will this morning's crude oil surge be the catalyst the XLE needs to finally clear that 69 hurdle?

China President Xi Jinping discussed plans for China to open up its trade policies a bit, specifically indicating lower tariffs for autos. Not coincidentally, many auto stocks are up solidly in pre-market action.

Given that the Volatility Index ($VIX) remains in the 20s for now, it'll be very interesting to see if trade fears shift to inflationary fears. Dow Jones futures are up nearly 300 points, but as we've seen so many times over the past 2-3 months, early bullish action doesn't necessarily translate into late bullish action. The news out of China is quite encouraging, but let's see how we close today.

Current Outlook

Transports ($TRAN) are in a fairly well-defined trading range between 10000 price support and 10800 price resistance. Currently, and after Monday's weak finish, the TRAN is very close to its price support level and needs to see a recovery:

Airlines appear to be the weakest link among the transports, but if there's some good news, it's that all of the areas of transports - railroads, truckers and airlines - are holding their February lows. Many technicians look to transports for confirming strength and/or weakness, so we want to play close attention to the price support levels marked above.

Airlines appear to be the weakest link among the transports, but if there's some good news, it's that all of the areas of transports - railroads, truckers and airlines - are holding their February lows. Many technicians look to transports for confirming strength and/or weakness, so we want to play close attention to the price support levels marked above.

Sector/Industry Watch

Those invested in tires ($DJUSTR) have probably grown a little "worn" waiting for the "rubber to meet the road" (ok enough puns for now). Performance in this area has been no laughing matter. February and March produced big losses, but there is a silver lining as a strong positive divergence has emerged. I expect this industry to rally over the next few weeks, potentially gaining 6-7% or so by month's end. Here's why:

While I do look for a nice short-term rally here to perhaps 100-101, there's plenty of technical work to do before I'd become bullish this group longer-term. For now, I'd expect to see that positive divergence play out by testing its declining 50 day SMA and resetting the PPO at its centerline (blue arrows). Once that occurs, I'd re-evaluate.

While I do look for a nice short-term rally here to perhaps 100-101, there's plenty of technical work to do before I'd become bullish this group longer-term. For now, I'd expect to see that positive divergence play out by testing its declining 50 day SMA and resetting the PPO at its centerline (blue arrows). Once that occurs, I'd re-evaluate.

Historical Tendencies

The Dow Jones U.S. Tires Index ($DJUSTR) has history on its side for the next few weeks as April has produced an average monthly return of 6.0% over the past 19 years. After a brutal March in which the DJUSTR lost close to 8%, the positive divergence reflected above in the Sector/Industry Watch section suggests history could be proven correct once again.

Key Earnings Reports

None

Key Economic Reports

March PPI released at 8:30am EST: +0.3% (actual) vs. +0.1% (estimate)

March Core PPI released at 8:30am EST: +0.3% (actual) vs. +0.2% (estimate)

February wholesale inventories to be released at 10:00am EST: +1.1% (estimate)

Happy trading!

Tom