Market Recap for Wednesday, June 27, 2018

Trade war fears are dominating the headlines, but U.S. Dollar Index ($USD) strength is quietly making the biggest news of all. The rising greenback is potentially good news as it signals that the U.S. economy is humming along, and is perhaps stronger than foreign economies. It also suggests that the relative strength enjoyed by small caps throughout Q2 2018 is likely to extend into Q3....and possibly longer. A rising dollar does create headwinds for multinationals, however, and that's why we've seen such weak relative performance from the Dow Jones and S&P 500. While all major U.S. indices fell on Wednesday, the Dow Jones and S&P 500 actually outperformed small caps. The Russell 2000 and NASDAQ led the decline, dropping 1.68% and 1.54%, respectively, while the Dow Jones and S&P 500 suffered lesser losses - 0.68% and 0.86%, respectively. Still, the dollar issue is worth considering as the following chart shows:

The falling dollar in 2017 enabled the S&P 500 to soundly outperform the small cap Russell 2000, but the roles have reversed in 2018, thanks to a rising dollar. A further break above 95 in the USD would likely spur small caps to additional relative strength in the second half of 2018.

The falling dollar in 2017 enabled the S&P 500 to soundly outperform the small cap Russell 2000, but the roles have reversed in 2018, thanks to a rising dollar. A further break above 95 in the USD would likely spur small caps to additional relative strength in the second half of 2018.

Energy (XLE, +1.34%) continued to benefit from surging crude oil prices ($WTIC), which neared $73 per barrel on Wednesday, closing at their highest level since late-2014. Utilities (XLU, +0.48%), a defensive sector, was the only other sector to finish in positive territory. Weakness was felt everywhere else, especially in technology (XLK, -1.36%), consumer discretionary (XLY, -1.29%) and financials (XLF, -1.24%). Banks ($DJUSBK) dropped just beneath very critical intermediate-term price support at 455 and also closed beneath their rising 50 week SMA for the first time in nearly two years:

Throughout this uptrend, the DJUSBK has not seen a weekly RSI close beneath 40 (we're at 42), a weekly PPO close beneath 0 (we're currently at -0.115) or a close beneath the 50 week SMA (we're currently at 450.96, beneath 459.63 - 50 day SMA).

Throughout this uptrend, the DJUSBK has not seen a weekly RSI close beneath 40 (we're at 42), a weekly PPO close beneath 0 (we're currently at -0.115) or a close beneath the 50 week SMA (we're currently at 450.96, beneath 459.63 - 50 day SMA).

Perhaps the biggest issue the market is facing right now, however, is the rising Volatility Index ($VIX). The VIX closed on Wednesday at 17.91, the highest close since the second week of April. A rapidly rising VIX is synonymous with a quickly deteriorating stock market. Huge declines can be seen over just a few days when the VIX spikes so we're in a period of serious technical turmoil right now. What we want to see from a bullish perspective is a huge drop in the VIX from intraday highs to signal that the worst is behind us in terms of fear. Over the past 2 1/2 months, the VIX has topped in the 18-20 range. An intraday move above that range and a close beneath it would be a very bullish short-term development.

Pre-Market Action

Dow Jones futures have been moving back and forth between positive and negative territory this morning as recent selling and increasing fear continues to spook traders. At last check, and with a little more than an hour to go to the opening bell, Dow Jones futures are lower by 44 points.

Walgreens Boots Alliance (WBA) - the newest Dow Jones component - reported a "trifecta" this morning. They (1) reported both revenues and EPS that beat Wall Street forecasts, (2) authorized a $10 billion share repurchase program, and (3) increased their quarterly dividend 10% - from $.40 to $.44. But in the seller's market we have currently, all of that adds up to a loss of 1% in pre-market trading.

Current Outlook

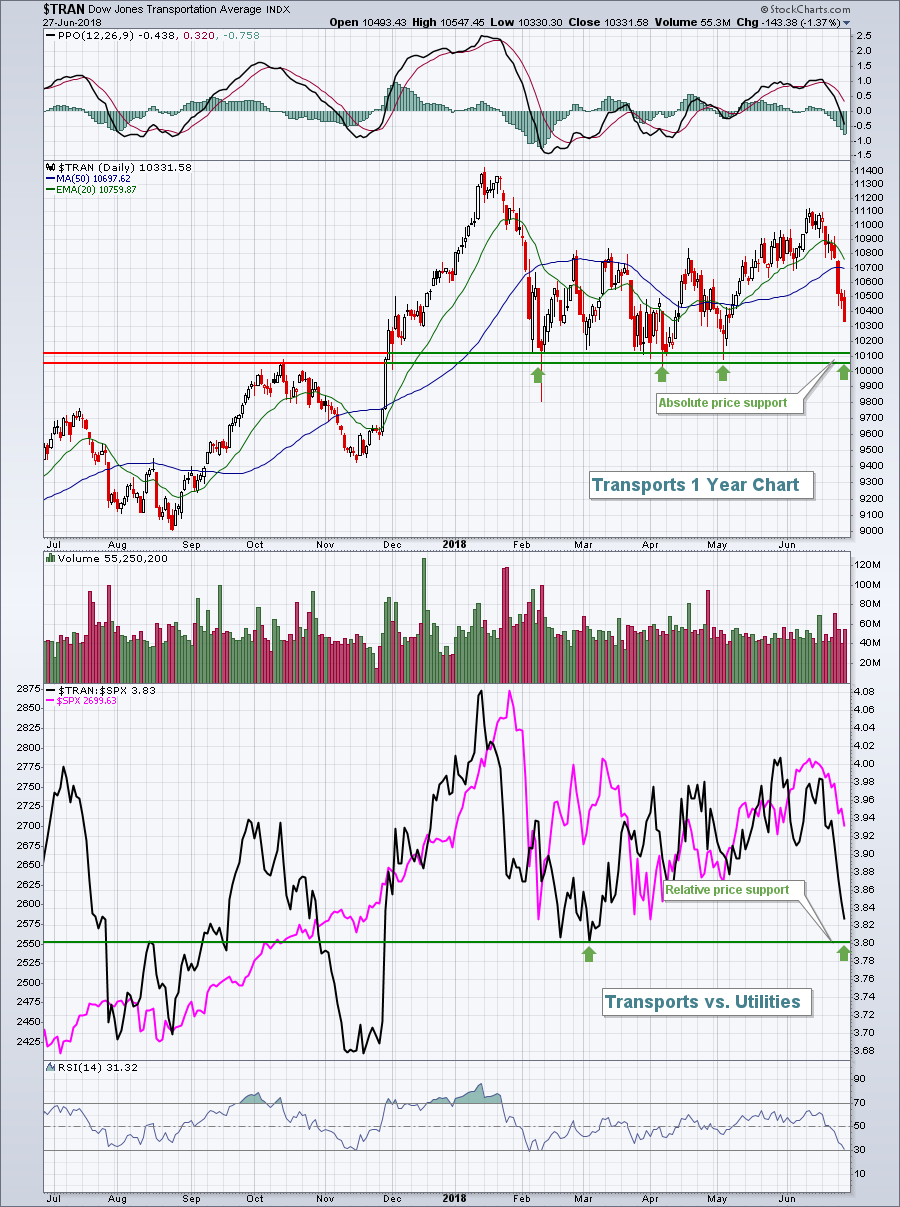

I'll be looking for renewed leadership in transportation stocks ($TRAN). They've lost approximately 7% in the past 7 trading sessions and are rapidly approaching major price support. Tranports have also weakened considerably vs. their utility ($UTIL) counterparts. The downward trend in this ratio ($TRAN:$UTIL) is also nearing relative support, so transports should be a key as we look for clues of the market's short-term direction:

The pink line above measures the S&P 500 performance. When transports lead utilities, we typically see an advancing S&P 500. When the opposite occurs, the S&P 500 tends to suffer. That's why transports holding onto both absolute and relative price support is important in the very near-term.

Sector/Industry Watch

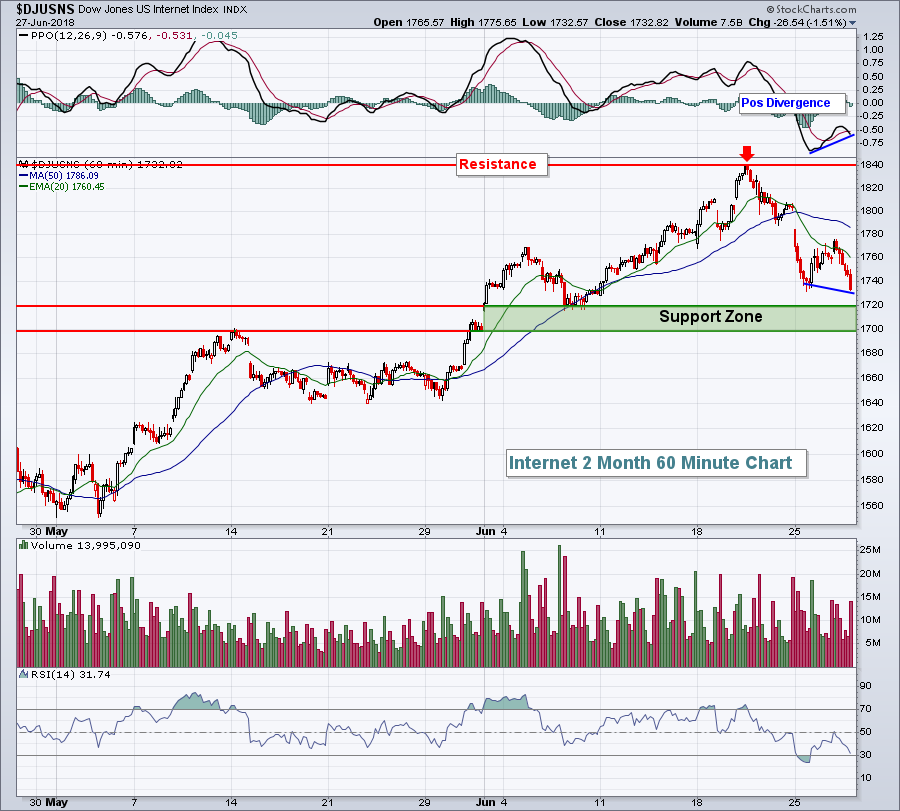

Internet stocks ($DJUSNS) have fallen roughly 6% over the past 5 trading sessions, but there's the potential of good news near-term. First, we're now in the latter days of June and seasonally stocks tend to do well as a calendar month approaches its end. Second, there's a 60 minute positive divergence in play on the DJUSNS, as well as both semiconductors ($DJUSSC) and software ($DJUSSW). Here's the DJUSNS chart:

Headline news has been driving U.S. equity prices lower, but I believe it's a short-term opportunity. Small to mid-size internet names like Carbonite (CARB) and GoDaddy (GDDY) have been swept up in the recent selling, but still have strong technical charts and high SCTR scores. Reversing candles could present nice opportunities in some of these names.

Headline news has been driving U.S. equity prices lower, but I believe it's a short-term opportunity. Small to mid-size internet names like Carbonite (CARB) and GoDaddy (GDDY) have been swept up in the recent selling, but still have strong technical charts and high SCTR scores. Reversing candles could present nice opportunities in some of these names.

Historical Tendencies

The rising dollar typically provides tailwinds for small cap stocks. I expect the dollar to continues its rise during the second half of 2018 and small caps to outperform as a result. Historically, this doesn't line up as the Russell 2000 struggles during the summer months. Here are the annualized returns on the small cap Russell 2000 (since 1987) by summer month:

July: -6.24%

August: -7.50%

September: -1.65%

Key Earnings Reports

(actual vs. estimate):

ACN: 1.79 vs 1.71

MKC: 1.02 vs .93

WBA: 1.53 vs 1.47

(reports after close, estimate provided):

NKE: .64

Key Economic Reports

Final Q1 GDP to be released at 8:30am EST: +2.2% (estimate)

Initial jobless claims to be released at 8:30am EST: 220,000 (estimate)

Happy trading!

Tom