Market Recap for Tuesday, June 26, 2018

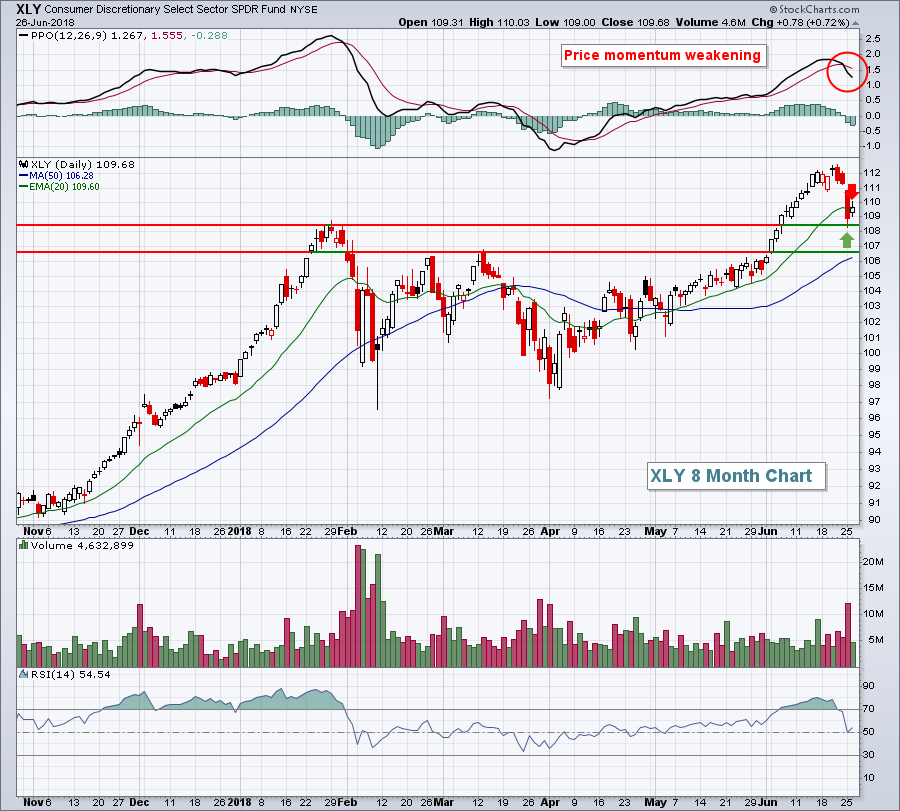

Tepid gains on Wall Street allowed trade fears to subside for a day, but technical indications suggest this is likely just a temporary breather. The Dow Jones gained 30 points on the session, while the small cap Russell 2000 and tech-laden NASDAQ produced better relative gains of 0.66% and 0.39%, respectively. Energy (XLE, +1.26%), consumer discretionary (XLY, +0.72%) and technology (XLK, +0.40%) rebounded after rough sessions on Monday. The XLY has been the strongest sector ETF of late and its ability (or inability) to move back above its rising 20 day EMA could provide the clue traders are looking for in the near-term:

The XLY did manage to close above its 20 day EMA yesterday, but barely. Failure today could result in a couple price support levels coming into play. First, there's price support near 108.50 established on the breakout above the January high. Then there's a gap and price support level closer to 106.50 that could be tested.

The XLY did manage to close above its 20 day EMA yesterday, but barely. Failure today could result in a couple price support levels coming into play. First, there's price support near 108.50 established on the breakout above the January high. Then there's a gap and price support level closer to 106.50 that could be tested.

Crude oil ($WTIC) surged yesterday, encouraging traders to scoop up energy shares. After weakness into mid-June printed a positive divergence, the WTIC has rallied strongly, up another 3.60% on Tuesday. Here's the chart, which appears to be unfolding as a possible cup with volume accelerating into the right side of the cup:

Crude oil is rising again this morning in pre-market action.

Crude oil is rising again this morning in pre-market action.

Health care providers ($DJUSHP) were among the losers on Tuesday, falling 1.64%. This group recently approached major overhead resistance at 1950 and seem to be pulling back on lesser volume to create future trading opportunities.

Pre-Market Action

ConAgra Brands (CAG) has agreed to acquire Pinnacle Foods (PF) for $8.1 billion in a cash and stock deal. The acquisition had been speculated in recent sessions with PF rising by about 5% in the past three to four days.

Dow Jones futures were down significantly earlier this morning, but a softer tone toward China by President Trump reversed those futures. At last check, and with a bit more than an hour to go to the opening bell, Dow Jones futures have turned positive, rising 33 points.

Current Outlook

The S&P 500 was turned back yesterday at its declining 20 hour EMA. In order to see strengthening price action, we'll first need to see the S&P 500 clear this key moving average. To the downside, it appears we could be on our way to test a gap support zone from 2690-2700:

The red circles above highlight the PPO weakness at each of the recent bottoms. Because the PPO has moved a bit lower this time and yesterday failed at key resistance, the odds are improving that we'll move into that gap support zone, possibly triggering a positive divergence on this hourly chart. That could mark a significant short-term bottom. The breakdown at 2740 now marks key price resistance so let's consider the short-term trading range to be 2690-2740. A break out of this range is what we should use to determine the likely intermediate-term direction of U.S. equities.

The red circles above highlight the PPO weakness at each of the recent bottoms. Because the PPO has moved a bit lower this time and yesterday failed at key resistance, the odds are improving that we'll move into that gap support zone, possibly triggering a positive divergence on this hourly chart. That could mark a significant short-term bottom. The breakdown at 2740 now marks key price resistance so let's consider the short-term trading range to be 2690-2740. A break out of this range is what we should use to determine the likely intermediate-term direction of U.S. equities.

Sector/Industry Watch

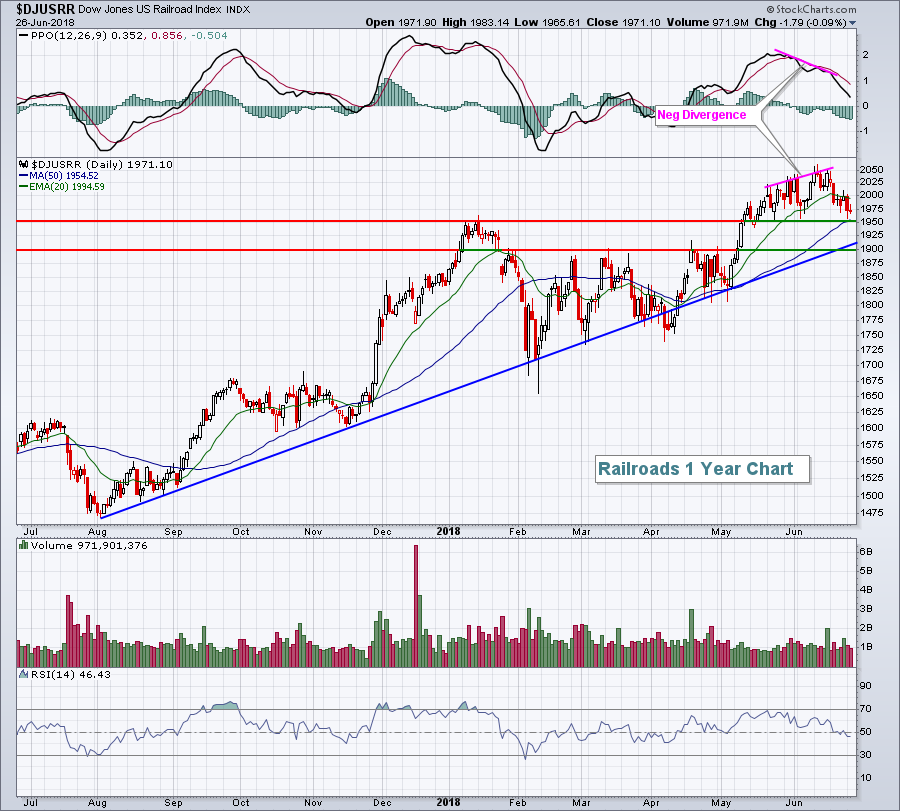

The Dow Jones U.S. Railroads Index ($DJUSRR) has succumbed to profit taking the past two weeks, but is rapidly approaching support levels that make the group a solid reward to risk alternative on the long side:

1950 is the initial price support level and we've approached that the past two trading sessions. Another support level resides near 1900 and trendline support moves through the middle of these two price support levels.

1950 is the initial price support level and we've approached that the past two trading sessions. Another support level resides near 1900 and trendline support moves through the middle of these two price support levels.

Historical Tendencies

The bearish historical period from June 18th through June 26th has ended.....thankfully. While futures are weak this morning, historical tendencies begin to turn bullish tomorrow. The June 28th through July 17th period has produced annualized returns of +24.14% on the S&P 500 since 1950. That's 15 percentage points above the average 9% annual returns over that same period.

The NASDAQ's historical tendencies are a bit more choppy from now until July 17th, but we do start a brief four day bullish historical period tomorrow that has produced annualized returns of 66.67% since 1971.

Key Earnings Reports

(actual vs. estimate):

GIS: .79 vs .73

PAYX: .61 (estimate - still awaiting results)

Key Economic Reports

May durable goods to be released at 8:30am EST: -0.6% (estimate)

May durable goods ex-transports to be released at 8:30am EST: +0.5% (estimate)

May wholesale inventories to be released at 8:30am EST: +0.3% (estimate)

May pending home sales to be released at 10:00am EST: +0.6% (estimate)

Happy trading!

Tom