Note

I'm traveling today so my article will be abbreviated.

Market Recap for Wednesday, January 23, 2019

It was a fairly volatile session on Wednesday as U.S. indices opened higher, but quickly fell fairly deep into negative territory before rallying in the afternoon. Only the small cap Russell 2000 (-0.22%) failed to close in positive fashion. The Dow Jones was the clear leader throughout the session, gaining 0.70%, as a few notable components saw strong reactions after earnings were released. International Business Machines (IBM, +8.46%), United Technologies (UTX, +5.20%) and Proctor & Gamble (PG, +4.77%) jumped after reporting solid results. UTX did finish at its 50 day SMA and well off its intraday high as they warned that revenues for FY19 would be weaker than expected.

One problem with yesterday's strength, however, was that leadership came from consumer staples (XLP, +1.19%) and utilities (XLU, +1.01%).

Pre-Market Action

Commerce Secretary Wilbur Ross said the U.S. was still "miles and miles away" from a trade deal with China, dampening U.S. futures this morning. Futures were pointing to a higher open prior to this statement. The 10 year treasury yield is lower by 4 basis points and is currently just beneath 2.72%, despite a much better than expected reading on initial jobless claims.

Markets were mostly higher overnight in Asia, while European trading is mixed after the ECB left rates unchanged.

Dow Jones futures are down 30 points with 30 minutes left to today's opening bell.

Current Outlook

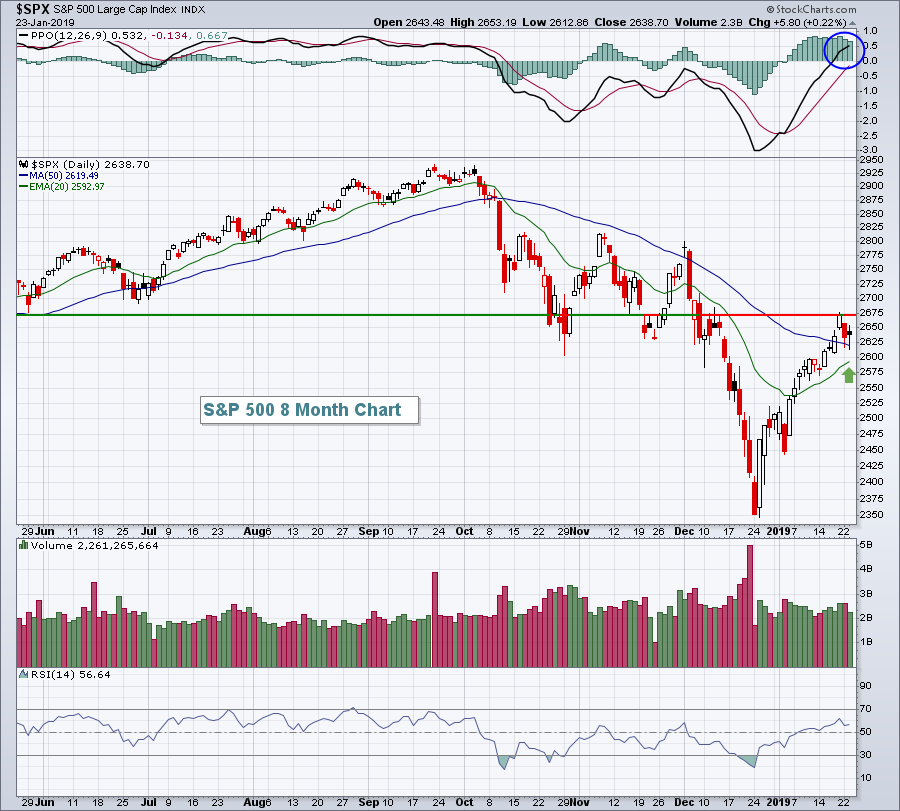

The S&P 500 is currently trapped between its rising 20 day EMA and declining 20 week EMA. The following chart shows that buyers returned as this benchmark index approached its 20 day EMA - short-term bullish behavior:

The daily PPO has crossed above the centerline, highlighting the current bullish short-term price momentum. Thus far, the rising 20 day EMA is holding as price support as I would expect with such a bullish chart pattern. Just keep in mind that the overriding longer-term pattern is bearish. Another break above the recent price high would begin to tilt the technical picture more towards bullish, in my view.

The daily PPO has crossed above the centerline, highlighting the current bullish short-term price momentum. Thus far, the rising 20 day EMA is holding as price support as I would expect with such a bullish chart pattern. Just keep in mind that the overriding longer-term pattern is bearish. Another break above the recent price high would begin to tilt the technical picture more towards bullish, in my view.

Sector/Industry Watch

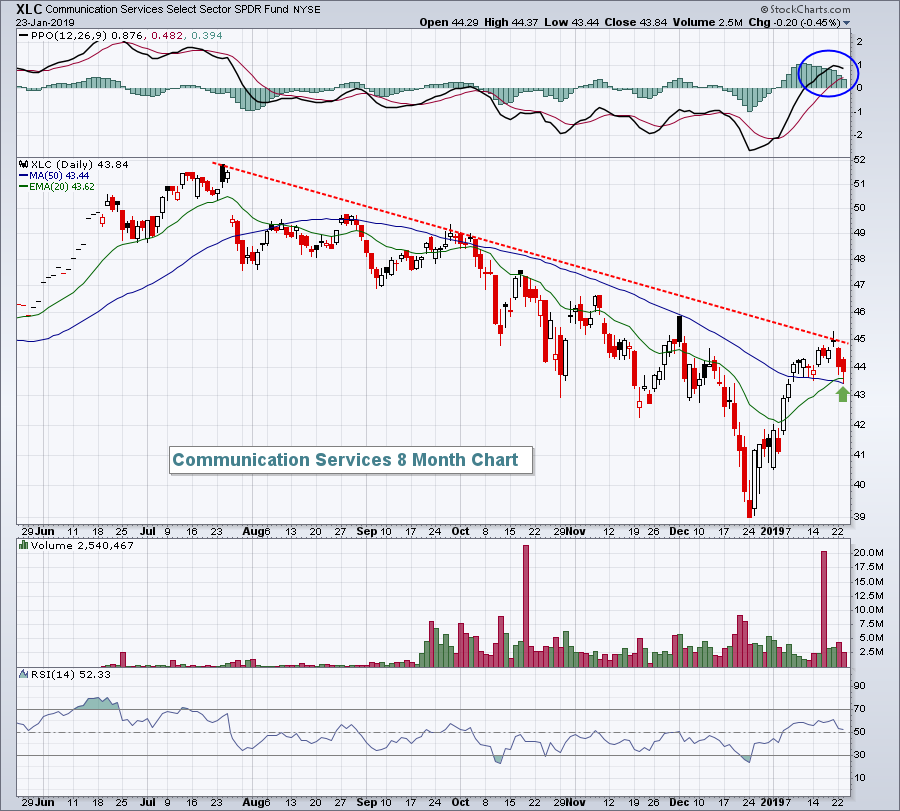

Yesterday, the communication services sector (XLC, -0.45%) threatened to become the first aggressive sector to close back beneath that key 20 day EMA. By the close, however, the group had strengthened and easily held serve:

The failure at trendline resistance and the daily PPO rolling over is ominous, but for now, the XLC held support where it needed to. Another trip down to yesterday's low would likely be met with more selling. Be careful here.

The failure at trendline resistance and the daily PPO rolling over is ominous, but for now, the XLC held support where it needed to. Another trip down to yesterday's low would likely be met with more selling. Be careful here.

Historical Tendencies

I'll be back with more historical data next week.

Key Earnings Reports

(actual vs. estimate):

AAL: 1.04 vs 1.05

AEP: .72 vs .72

BMY: .94 vs .85

FCX: .11 vs .21

GWW: 3.96 vs 3.60

HBAN: .29 vs .31

LUV: 1.17 vs 1.06

MKC: 1.67 vs 1.70

RCI: .86 vs .81

STM: .46 vs .44

TAL: .24 vs .10

TXT: 1.15 vs .98

UNP: 2.12 vs 2.06

(reports after close, estimate provided):

DFS: 2.09

ETFC: 1.05

INTC: 1.22

ISRG: 2.99

NSC: 2.30

RMD: .95

SBUX: .65

WDC: 1.51

Key Economic Reports

Initial jobless claims released at 8:30am EST: 199,000 (estimate) vs. 218,000 (actual)

January PMI composite flash to be released at 9:45am EST: 54.2 (estimate)

December leading indicators to be released at 10:00am EST: -0.1% (estimate)

Happy trading!

Tom